Decoding Auto Insurance: Beyond the Basics

Auto insurance. It's a necessity, but how many of us truly understand it? Beyond the minimum required by your state, what does auto insurance actually offer? It's not simply about checking a box for legal compliance. It's about protecting your financial well-being from unforeseen circumstances. Understanding auto insurance means knowing how it protects you and your assets.

Key Coverage Components

A complete insurance policy can feel complex. However, certain components are essential. Liability coverage is crucial, protecting you financially if you cause an accident. This covers the other party's medical bills and property damage, preventing potentially crippling lawsuits.

Uninsured/underinsured motorist coverage protects you if you're hit by someone without adequate insurance. This is a more frequent occurrence than many realize.

Finally, comprehensive and collision coverage protect your vehicle from damage. This includes damage from accidents, theft, and even weather-related incidents.

Understanding Your Premium

Many factors affect your insurance premium, some less obvious than others. Your driving record, including accidents and traffic violations, is a major factor. However, your location, age, the type of vehicle you drive, and even your credit score can influence your rates.

Insurers use complex formulas to assess risk. Understanding these factors can help you make informed choices about your coverage. This includes choosing your deductible, the amount you pay out-of-pocket before your insurance takes over. A higher deductible lowers your premium but requires more funds available if you have an accident.

The global vehicle insurance market is growing rapidly. Valued at approximately USD 973.33 billion in 2025, it's projected to reach USD 1,796.61 billion by 2034. You can learn more about this growing market through resources like Precedence Research. This growth highlights the increasing importance of auto insurance worldwide.

Further information can be found through articles like Demystifying auto insurance. This kind of information empowers you to choose the right coverage, ensuring you have the necessary protection without overspending.

Coverage Types That Actually Matter for Your Situation

Choosing the right auto insurance can feel overwhelming. It's not just about meeting legal requirements; it's about protecting your financial well-being. This means understanding which coverage types truly offer protection and which might be less important based on your individual needs. A clear understanding of your auto insurance options starts with knowing what's available.

Essential Coverage: Protecting Yourself and Others

Liability coverage is the foundation of any auto insurance policy. It protects you financially if you're at fault in an accident, covering the other party's medical expenses and property damage. This is crucial protection against potential lawsuits. For example, if you cause an accident resulting in substantial medical bills for another driver, liability coverage prevents you from paying those costs directly.

Uninsured/underinsured motorist coverage is equally vital. This protects you if you're hit by a driver without sufficient insurance—a surprisingly common occurrence. This coverage helps pay for your medical bills and car repairs, ensuring you're not left with the expenses because of someone else's negligence.

Understanding key definitions can be helpful when navigating insurance options. You can learn more about how predictive modeling is impacting insurance.

Protecting Your Vehicle: Collision and Comprehensive

Collision coverage pays for repairs to your vehicle if it's damaged in an accident, regardless of fault. This includes damage from hitting an object, such as a tree or guardrail. Comprehensive coverage, on the other hand, covers damage to your car from events other than collisions. Think theft, vandalism, or weather-related incidents like hail or flooding. These coverages are especially valuable for newer cars or those with outstanding loans.

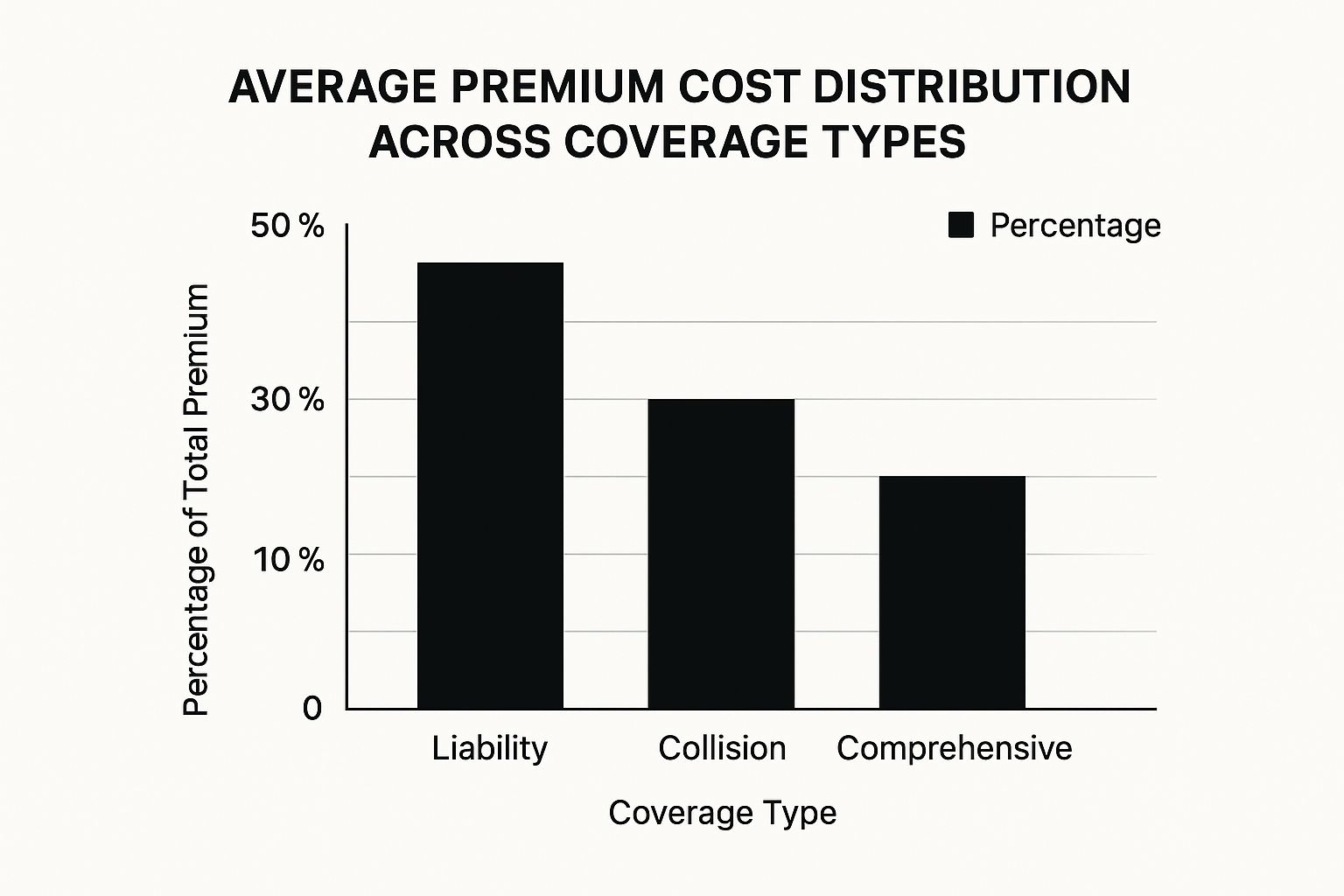

To illustrate how your premium is usually distributed across these core coverage types, take a look at the infographic below:

Liability coverage typically represents the largest portion of your premium, followed by collision and then comprehensive. This distribution reflects the importance of protecting yourself from liability claims, which can be far more expensive than vehicle repairs.

To further clarify the different coverage types, let's look at a comparison table:

Auto Insurance Coverage Types Comparison

This table compares different auto insurance coverage options, what they protect against, and who might need them.

| Coverage Type | What It Covers | Required or Optional | Who Should Consider |

|---|---|---|---|

| Liability | Medical expenses and property damage of others if you are at fault | Required in most states | All drivers |

| Uninsured/Underinsured Motorist | Your expenses if hit by an uninsured or underinsured driver | Often required | All drivers |

| Collision | Damage to your car from accidents, regardless of fault | Optional | Drivers with newer cars or loans |

| Comprehensive | Damage to your car from non-collision events (theft, vandalism, weather) | Optional | Drivers with newer cars or loans |

As you can see, liability and often uninsured/underinsured motorist coverage are typically required by law. Collision and comprehensive, while optional, offer valuable protection for your vehicle.

Customizing Your Coverage for Your Needs

The ideal auto insurance policy isn't one-size-fits-all. Factors such as your driving habits, the value of your vehicle, and your financial situation all contribute to determining the best coverage for you. This means understanding your individual needs and adjusting your policy accordingly is crucial for getting the most out of your auto insurance.

The Hidden Factors Driving Your Premium Costs

While your driving history and vehicle type clearly impact your auto insurance premiums, a complex algorithm works behind the scenes. This algorithm uses a variety of factors, some you can control and some you can't, to calculate your auto insurance costs. Understanding these less obvious factors can help you make smarter insurance decisions.

Beyond the Obvious: Unmasking the Algorithm

Insurers use your credit score to gauge your financial responsibility. A higher credit score often leads to lower premiums. Statistically, people with better credit tend to file fewer claims. Your location also matters significantly. Areas with higher rates of accidents, theft, or natural disasters generally have higher premiums.

Your age is another key factor. Younger and older drivers statistically present higher risks, which often results in higher premiums. Younger drivers are sometimes perceived as less experienced, while older drivers may have slower reaction times. These are generalizations, but they demonstrate how insurers use demographics in their risk assessments.

The Impact of Seemingly Small Changes

Even minor life changes can affect your premiums. Changing jobs, getting married, or moving to a new zip code can all alter your risk profile from the insurer's perspective. A shorter commute, for instance, could lower your premium. Bundling your auto insurance with other policies, like homeowners or renters insurance, can often result in discounts.

Several factors influence the motor insurance market. Increasing vehicle ownership, regulatory changes, urbanization, and rising traffic density all contribute to market growth. In 2024, this market was valued at approximately USD 877.75 billion and is projected to reach USD 1,390.63 billion by 2029. Learn more about motor insurance market trends. This growth reflects the dynamic nature of the auto insurance industry.

Navigating the Rating System for Better Rates

Understanding how insurers categorize drivers can help you secure the best rates. Maintaining a clean driving record is essential. Avoiding accidents and traffic violations significantly lowers your perceived risk. Taking a defensive driving course can sometimes reduce premiums and demonstrate your commitment to safe driving.

By understanding the hidden factors that influence your premiums, you can make informed decisions about your auto insurance coverage and take steps to manage your expenses wisely. This knowledge empowers you to take control of your auto insurance and find the best possible coverage for your needs.

Mastering The Claims Process To Maximize Your Payout

Filing an auto insurance claim can feel overwhelming. However, understanding the process can significantly impact your final payout. Knowing how claims adjusters work and what documentation strengthens your claim can make a substantial difference. This section breaks down the process, highlighting key steps and common pitfalls to avoid.

The Critical First Steps After An Accident

After an accident, your immediate actions can heavily influence your claim's outcome. First, prioritize safety. Check for injuries and call for medical assistance if needed. Document the scene thoroughly by taking photos and videos of the damage to all vehicles and the surrounding area.

Obtain contact information from witnesses and the other driver. This documentation will prove invaluable later. Importantly, avoid admitting fault at the scene, even if you think you're responsible. Let the insurance companies determine liability.

Navigating The Claims Process: What To Expect

Once you file your claim, an adjuster will be assigned to your case. This adjuster will investigate the accident and assess the damages. They'll review police reports, witness statements, and the documentation you provide. Understanding how adjusters evaluate claims is essential for a fair settlement.

Be prepared to provide supplemental documentation, such as medical bills and repair estimates. The auto insurance industry is a large and growing market. The global automobile insurance carriers market was valued at approximately USD 936.62 billion in 2024 and is projected to reach USD 1,611.72 billion by 2029.

This growth is fueled by factors including legal requirements, a rise in accidents, and increasing vehicle affordability. You can find more detailed statistics here. This expanding market underscores the crucial role of auto insurance in protecting individuals and their assets.

Negotiating Your Settlement: Tips And Strategies

The adjuster will eventually present a settlement offer. Don't feel obligated to accept the first offer. It's often just a starting point for negotiation. Understand your policy's coverage limits and the true value of your damages.

Consider factors such as pain and suffering, lost wages, and the diminished value of your vehicle. If you're unsure about the offer's fairness, consult with an attorney. For further guidance, you might find this resource helpful: How to master car insurance claims.

When To Push Back And How To Appeal

If you believe the insurance company's offer is inadequate, you absolutely have the right to push back. Provide additional documentation that supports your claim and clearly explain your reasoning. If negotiations reach an impasse, you have the right to appeal.

This may involve filing a formal complaint and potentially pursuing arbitration or litigation. Knowing your rights and options empowers you to advocate for a fair settlement. Mastering the claims process means being prepared, understanding the adjuster’s role, and negotiating effectively. By following these steps, you can confidently advocate for your rights.

Premium-Slashing Tactics The Industry Doesn't Advertise

Beyond the common "safe driver" discounts and bundling, many lesser-known strategies can significantly lower your auto insurance premiums. These tactics aren't widely advertised, and insurance agents rarely volunteer this information. This section reveals these insider strategies, empowering you to control your insurance costs.

Leverage Price Optimization and Timing to Your Advantage

Price optimization is a practice insurers use to charge higher premiums to customers less likely to shop for better rates. To combat this, be an informed consumer. Regularly compare quotes from multiple insurers, even if you're already insured. This shows you're price-sensitive, making you less vulnerable to price optimization.

Timing your policy purchase can also help. Purchasing insurance mid-week or at the end of the month might offer slightly lower rates, though this can vary. Insurers may adjust pricing based on sales targets and internal algorithms.

Negotiating and Structuring Your Coverage For Savings

Don't hesitate to negotiate with your insurer. Ask about potential discounts, such as those for anti-theft devices, good student status, or completing a defensive driving course. For more premium-reducing strategies, review our guide on How to master auto insurance savings.

Structure your coverage to avoid overlaps. If you have comprehensive health insurance, you might reduce your medical payments coverage on your auto policy. Analyze your existing coverage to avoid paying twice for the same protection.

Deductibles, Bundling, and Loyalty Myths Debunked

Choosing the right deductible is key. A higher deductible lowers your premium but increases your out-of-pocket expenses after an accident. Choose a deductible you can comfortably afford. Don't automatically choose the lowest deductible; a higher one can lead to significant long-term savings.

Bundling auto and home insurance is often promoted as a cost-saving measure, but it's not always the best deal. Compare bundled prices with separate policies from different companies. Sometimes, individual policies offer better overall value.

Finally, loyalty to one insurer can be costly. Insurers often offer better rates to new customers. Don't hesitate to switch if you find a better deal. Loyalty discounts exist, but they may not outweigh the potential savings from switching.

The following table summarizes some common auto insurance discounts and how to qualify for them:

Auto Insurance Discount Opportunities

| Discount Type | Potential Savings | Eligibility Requirements | How to Apply |

|---|---|---|---|

| Safe Driver | Up to 20% | No accidents or violations for a specified period | Maintain a clean driving record |

| Multi-Policy | Up to 15% | Bundle auto and home insurance with the same company | Contact your insurer about bundling options |

| Good Student | Up to 10% | Maintain a certain GPA in high school or college | Provide proof of good grades |

| Anti-Theft Device | Up to 5% | Install an approved anti-theft device in your vehicle | Provide documentation of the installed device |

| Defensive Driving Course | Varies | Complete an approved defensive driving course | Provide certificate of completion |

| Military | Varies | Active or veteran military status | Provide proof of military service |

| Senior Citizen | Varies | Typically age 55 or older | Inquire with your insurer about senior discounts |

This table offers a quick overview of ways to save on car insurance. Always contact your insurance provider for specific details on discounts and eligibility requirements.

Future-Proofing Your Coverage: Tech Transformations Ahead

The auto insurance industry is rapidly evolving, thanks to advancements in technology. These aren't just minor tweaks; they're fundamentally changing how auto insurance is calculated, provided, and experienced. Understanding these trends is essential for making smart decisions about your coverage now and in the future.

Telematics and Usage-Based Insurance: Rewarding Safe Driving

Telematics, the technology behind usage-based insurance (UBI), is changing how insurers assess risk and set premiums. UBI programs use devices or smartphone apps to track driving habits, offering personalized premiums based on individual behavior instead of broad demographics. This allows safe drivers to often significantly lower their insurance costs. This shift towards personalized pricing encourages safer driving and gives drivers more control over their insurance expenses.

For example, insurers can track things like speed, acceleration, braking, and mileage to create a personalized risk profile. Drivers who consistently demonstrate safe driving habits are rewarded with lower premiums, while those with riskier behaviors may face higher rates. This creates a direct connection between how you drive and how much you pay for car insurance. Explore tactics to save money on your car insurance while maintaining essential coverage by learning more about lower insurance premiums.

AI and Automation: Streamlining Claims and Fighting Fraud

Artificial intelligence (AI) is transforming many aspects of auto insurance, especially claims processing. AI-powered systems can automate tasks like damage assessment, estimate generation, and even claim approval. This automation speeds up processing, resulting in quicker payouts and a smoother experience for policyholders. Furthermore, AI algorithms can help detect and prevent fraudulent claims, protecting both insurers and honest policyholders. This leads to more accurate and efficient claims handling, saving everyone time and resources.

This improved efficiency isn't just about speed; it's about accuracy and fairness. By removing some human subjectivity from the process, AI helps ensure claims are handled consistently and fairly, leading to a more transparent and trustworthy system.

Connected and Autonomous Vehicles: Redefining Risk

The increasing popularity of connected and autonomous vehicles presents both obstacles and opportunities for auto insurance. As vehicles become more interconnected and self-driving capabilities improve, the traditional driver-centric insurance model may need to change. As autonomous features manage more driving tasks, figuring out who is liable in an accident gets more complicated. Insurers are exploring new coverage models, like product liability insurance for manufacturers of autonomous vehicles, to manage these new risks. The very definition of who is insured and what is covered could change drastically in the near future.

For instance, if a self-driving car malfunctions and causes an accident, the liability may shift from the driver to the manufacturer or software developer. These shifts in responsibility are forcing insurers to rethink risk assessment and coverage design. This is a constantly evolving area of auto insurance, and understanding how these changes might impact your future coverage is vital.

Blockchain and Data Privacy: Building Trust and Transparency

Blockchain technology, known for its secure and transparent nature, is finding its way into auto insurance. Blockchain can verify the authenticity of insurance documents, track vehicle history, and simplify the claims process. This added transparency can reduce fraud and foster more trust between insurers and policyholders. However, the increased use of data in auto insurance also raises valid privacy concerns. It's crucial for consumers to understand how their data is collected, used, and protected. Choosing insurers with strong data privacy policies is essential as personalization becomes more common in the industry. This growing focus on data privacy is pushing for increased transparency and consumer control over personal information.

Comments are closed.