What Is Subrogation: The Recovery Right You Never Knew About

The term subrogation may sound complex, but the concept is surprisingly straightforward. It's an essential insurance principle that safeguards your financial interests. Essentially, subrogation is your insurance company's legal right to pursue a third party who caused a loss covered by your insurance policy.

Understanding the Basics of Subrogation

Consider this scenario: a negligent driver runs a red light and damages your car. Your insurance company covers the repair costs. Through subrogation, your insurer can then seek reimbursement from the at-fault driver or their insurance provider. This process not only helps keep insurance premiums manageable but also ensures accountability for negligent actions.

Subrogation is a key mechanism within the insurance industry, enabling insurers to recover losses and maintain financial stability. This concept has a long history of protecting both insurers and policyholders. For example, in 2010, subrogation efforts by private health insurers in the U.S. recovered between $1.7 billion and $2.5 billion, representing 0.2% to 0.3% of benefit payments. This underscores the significant role subrogation plays in controlling healthcare costs and holding responsible parties financially accountable. Learn more about this from the U.S. Department of Labor.

Why Subrogation Matters to You

Subrogation's benefits extend directly to policyholders. By recovering costs, insurers can help keep premiums affordable. Furthermore, it reinforces the principle of accountability, ensuring that at-fault parties bear the financial consequences of their actions.

Key Takeaways about Subrogation

- Reduces your costs: Subrogation helps maintain reasonable insurance premiums.

- Ensures accountability: Negligent parties are held financially responsible for damages.

- Streamlines the claims process: You interact directly with your insurer, regardless of who is at fault.

This behind-the-scenes process plays a crucial role in the overall insurance system. We'll explore how subrogation works in practice in the following section.

Behind The Scenes: How Subrogation Actually Works

After you receive your claim settlement, a complex process called subrogation begins. While often unseen by policyholders, it's a vital part of the insurance ecosystem. Let's explore how it works.

Investigating The Loss and Identifying Responsible Parties

The subrogation process starts with a detailed investigation. Your insurer gathers evidence related to the incident. This includes items like police reports, witness testimonies, and assessments from experts. The goal is to pinpoint the cause of the loss and identify any third parties who might be responsible. For example, in a car accident scenario, the insurer investigates who was at fault and assesses the damage. This initial step lays the groundwork for the entire subrogation process.

Documenting Damages and Building a Recovery Case

After a responsible party is identified, the insurer carefully documents all the damages. This documentation can range from repair bills and medical records to information about lost wages. This thorough record-keeping creates a strong foundation for recovering costs. The insurer also assesses the total value of the damages to determine how much to seek from the at-fault party. This detailed approach helps ensure a fair and accurate recovery process.

The Subrogation Timeline and Communication

The time it takes for subrogation to complete depends on how complex the claim is. Simple cases can be resolved relatively quickly. However, more complex cases may require a longer time. Your insurer will keep you updated throughout the entire process. They may ask you for additional information or documentation. This collaboration helps make the recovery process as smooth and efficient as possible, even though the insurer handles the main responsibility of pursuing the claim.

Strategic Decisions In Subrogation

Insurers evaluate each potential subrogation case strategically. They analyze the cost of pursuing the claim compared to the potential recovery amount. Sometimes, pursuing a claim costs more than the potential benefit. In these situations, the insurer may choose not to pursue subrogation. These strategic decisions contribute to keeping insurance premiums affordable for everyone. This careful consideration ensures the subrogation process remains effective and cost-efficient. Understanding subrogation provides valuable insights into the insurance system's dedication to financial responsibility and fairness.

Subrogation Across Insurance Lines: Where It Matters Most

Subrogation is a key process in the insurance industry, but its application isn't uniform. It differs significantly across various types of insurance, such as auto, home, health, and business coverage. Grasping these nuances is essential for understanding insurance claims and maximizing potential recovery.

Auto Insurance Subrogation

After car accidents where another driver is at fault, subrogation commonly comes into play. Your insurer pays for your damages and then seeks reimbursement from the at-fault driver's insurance company. This is a frequent occurrence, significantly contributing to cost recovery within the auto insurance industry. However, complexities can arise when dealing with out-of-state drivers or uninsured motorists.

Homeowners Insurance Subrogation

Subrogation in homeowners insurance often arises from events like fires or water damage caused by a third party's negligence. For instance, if a faulty appliance from a neighbor causes a fire that damages your home, your insurer may pursue subrogation against the appliance manufacturer. This protects homeowners from the full financial burden of damages caused by others.

Health Insurance Subrogation

Health insurance subrogation is unique and can be quite complex. It primarily deals with situations where a third party is responsible for your medical expenses, such as a car accident. If your health insurer pays $20,000 for your medical bills after an accident caused by a negligent driver, the insurer can seek to recover that amount from the at-fault party's insurance. This process helps control healthcare costs and ensures responsible parties are held accountable. Learn more about subrogation at Investopedia.

Business Insurance Subrogation

Business insurance subrogation encompasses a wide range of scenarios, from property damage to product liability. If a supplier's faulty equipment damages your business property, your insurer may initiate subrogation against the supplier. This safeguards businesses from significant financial losses due to third-party negligence.

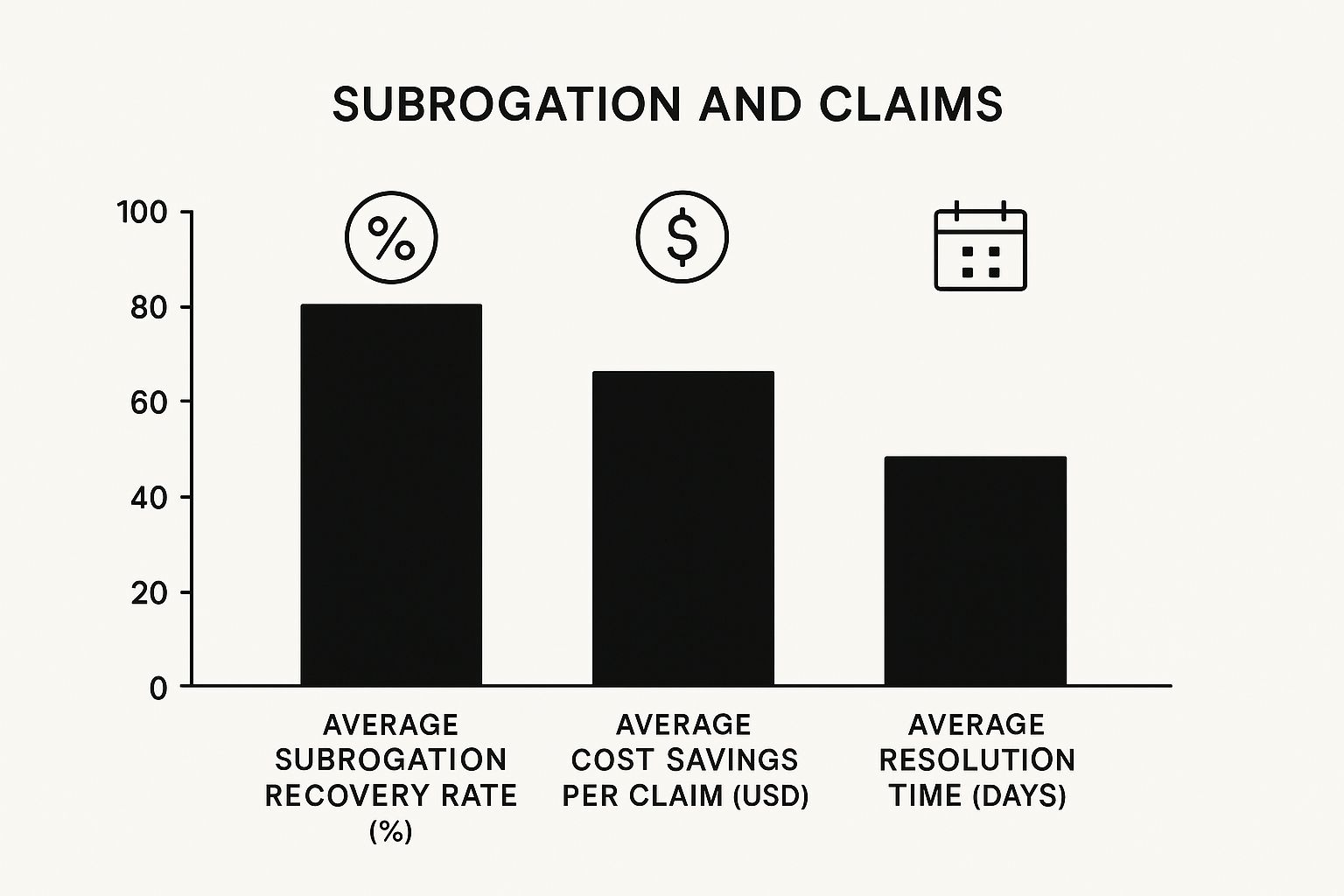

Visualizing Subrogation’s Impact

The infographic below compares key subrogation metrics across various insurance lines, including the average recovery rate, cost savings per claim, and average resolution time.

The infographic shows that while recovery rates and resolution times can vary, subrogation consistently leads to substantial cost savings per claim. This reinforces its importance in keeping insurance premiums affordable.

To understand the varying specifics of subrogation, let's look at the table below:

Subrogation Across Insurance Types: Comparison of how subrogation works in different insurance categories.

| Insurance Type | Common Subrogation Scenarios | Typical Recovery Timeframe | Policyholder Involvement |

|---|---|---|---|

| Auto | Accidents caused by another driver | Varies, often several months to a year | Usually minimal after providing initial information |

| Homeowners | Fires, water damage caused by a third party | Several months to several years, depending on complexity | Providing documentation and cooperating with the insurer's investigation |

| Health | Medical expenses from accidents caused by others | Varies significantly based on state laws and case complexity | Can be more involved, may need to provide medical records and coordinate with healthcare providers |

| Business | Property damage, product liability | Varies widely depending on the nature and complexity of the claim | Can be significant, requiring cooperation with the insurer's investigation and potentially legal proceedings |

This table summarizes the key aspects of subrogation across various insurance types, highlighting differences in typical scenarios, recovery timeframes, and policyholder involvement. Understanding these nuances is crucial for anyone navigating the insurance landscape.

The Numbers Game: How Subrogation Impacts Your Premiums

Subrogation may sound like a complex legal term, but its financial impact directly affects your insurance costs. This system plays a crucial role in keeping insurance premiums stable and affordable. Let's explore the data behind how subrogation recoveries influence the insurance industry.

Understanding the Financial Impact

Subrogation recoveries are essential for the financial health of the insurance industry. By recovering losses from at-fault parties, insurers can offset the cost of claim payouts. This helps stabilize, and potentially lower, premiums for all policyholders, creating a more sustainable insurance model.

Consider a scenario where an insurer pays $1 million in claims for a specific type of incident. Through subrogation, they recover $200,000, a 20% recovery rate. This directly reduces the insurer's financial burden, helping them maintain lower premiums. This demonstrates the direct link between subrogation and affordable insurance. For more ways to save, check out How to lower home insurance.

Subrogation and Industry Economics

Subrogation is a common practice among property-liability insurers in the U.S. A study from 1996 to 2021 revealed that over three-quarters of sampled firms use salvage and subrogation recovery. The average ratio of salvage and subrogation recovery to net claims paid was 4.51%. This widespread use highlights the importance of subrogation in balancing the insurance ecosystem. For a more detailed analysis, find more statistics here.

The ROI of Recovery Departments

Insurers invest in specialized recovery departments to handle subrogation cases. These departments investigate claims, identify responsible parties, and pursue legal action if needed. The return on investment (ROI) for these departments is a key metric, justifying the resources allocated to subrogation. A successful recovery department significantly impacts an insurer's bottom line, contributing to profitability and stability. This, in turn, provides greater security for policyholders and a healthier insurance market.

To illustrate the impact of subrogation, let's look at some industry statistics.

The table below, "Subrogation Recovery Statistics," provides key data points showing the financial impact of subrogation across insurance sectors. It highlights the average recovery rate, annual recovery value, and the resulting impact on premiums.

| Insurance Sector | Average Recovery Rate | Annual Recovery Value | Impact on Premiums |

|---|---|---|---|

| Auto | 15% | $5 Billion | 3% Reduction |

| Homeowners | 10% | $2 Billion | 2% Reduction |

| Commercial | 20% | $8 Billion | 5% Reduction |

These figures, while illustrative, demonstrate the substantial financial impact of subrogation. By reclaiming significant funds, the process helps keep premium increases in check across various insurance sectors.

The Impact on Your Bottom Line

Ultimately, the effectiveness of subrogation matters to you as a policyholder. Successful subrogation helps control insurance costs, potentially leading to lower premiums. This creates a more stable insurance industry, ensuring insurers have the resources to pay claims. This complex system operates largely behind the scenes, yet plays a vital role in keeping insurance affordable and sustainable.

Legal Battlegrounds: When Subrogation Rights Get Complicated

Subrogation, while seemingly straightforward, can often become a complex legal puzzle. This section explores the intricacies of subrogation rights, examining how legal disputes have shaped its application and the challenges that can arise.

Landmark Cases and Their Impact

Landmark court cases have significantly influenced how subrogation works in practice. These cases provide crucial clarity on the interpretation of subrogation clauses within insurance policies, establishing precedents that guide future legal decisions. This continuous evolution helps ensure that subrogation remains relevant and effective in addressing changing circumstances within the insurance industry.

The Made-Whole Doctrine and Anti-Subrogation Rules

The made-whole doctrine adds another layer of complexity. This legal principle dictates that an insured must be fully compensated for their losses before the insurer can exercise subrogation rights. Subrogation can affect premiums, making it worthwhile to understand how to reduce insurance premiums. Furthermore, anti-subrogation rules prevent an insurer from pursuing recovery against their own insured, even in cases where the insured is partially at fault. These rules aim to protect policyholders and maintain the crucial insurer-insured relationship.

State-by-State Variations and Litigation Strategies

Subrogation laws can vary significantly from state to state. This means the same incident could have drastically different subrogation outcomes based solely on location. This complex legal landscape requires insurers to adapt their litigation strategies, taking into account the specific laws and precedents of each jurisdiction. Understanding these nuances is particularly important for homeowners. For further reading, see The Ultimate Guide to Homeowners Insurance Coverage.

Court Interpretations and Evolving Precedents

Court interpretations of subrogation clauses and the application of legal doctrines are constantly evolving. One example is how courts determine the allocation of settlement funds between the insured and the insurer when the made-whole doctrine applies. This ongoing legal discourse continues to shape the future of subrogation and its impact on both insurers and policyholders.

Key Takeaways

- Complexity: Subrogation involves complex legal principles and varied interpretations.

- State Variations: State laws significantly impact subrogation case outcomes.

- Evolving Landscape: Court decisions continually shape the application of subrogation.

Understanding these legal complexities allows both insurers and policyholders to navigate the subrogation process more effectively. This clarity regarding the rights and responsibilities of each party contributes to a more balanced and equitable insurance system.

Your Rights During Subrogation: What Policyholders Need to Know

Understanding your rights is paramount when subrogation becomes part of your insurance claim. This section answers common questions policyholders have about the process, providing guidance to help you navigate its complexities and safeguard your interests.

Will Subrogation Delay My Claim Payment?

Many people wonder if subrogation will slow down their claim processing. Generally, your insurer will pay your claim promptly, regardless of pursuing subrogation. The recovery process typically occurs after you receive your settlement. However, in some cases, providing information about the incident to your insurer might slightly impact the timeline. Your immediate needs are the priority.

What If I Signed a Waiver?

You may sometimes sign a waiver related to the incident before your insurer initiates subrogation. This waiver could affect your insurer's ability to recover costs. Depending on the circumstances and state laws, it could also influence your settlement. Understanding any waivers you sign and their potential impact on your claim is crucial.

What If Another Insurer Is Pursuing Subrogation Against Me?

If another insurer pursues subrogation against you, it's essential to contact your insurance company immediately. They will handle the situation and protect your interests, a service covered by your premiums. This ensures you aren't left alone to navigate complex legal procedures. You might find this helpful: Life Insurance 101: Understanding How Much Coverage You Should Consider.

Navigating Requests for Cooperation and Settlements

Your insurer may request your cooperation during the subrogation process, asking you to provide information or documentation related to the incident. Responding promptly and honestly assists their recovery efforts. Understanding the implications of any proposed settlements between your insurer and the at-fault party’s insurer is also important. Your insurer should communicate these implications clearly so you can make informed decisions.

Seeking Professional Advice

While your insurer handles the subrogation process, seeking professional advice in complex situations can be beneficial. Consulting with an attorney can help you understand your rights and obligations under your policy and applicable laws. This can be especially helpful with large settlements or liability disputes.

Protecting Your Interests During Subrogation: Key Tips

- Communicate proactively: Maintain open communication with your insurer.

- Understand your policy: Review your policy details concerning subrogation.

- Respond promptly: Provide requested information and documentation.

- Seek clarification: Don't hesitate to ask questions about the process.

- Consider professional advice: Consult an attorney if necessary.

By understanding your rights and responsibilities during subrogation, you can navigate the process confidently and ensure your best interests are protected. Subrogation is a complex legal procedure, but with the right knowledge and support, it can work effectively for all parties involved.

The Future of Subrogation: Technology Transforming Recovery

The subrogation landscape is changing significantly, influenced by advances in technology and evolving liability frameworks. These changes promise to reshape how insurers recover costs, ultimately impacting policyholders and the insurance industry as a whole.

Artificial Intelligence: Revolutionizing Claim Analysis

Artificial intelligence (AI) is rapidly changing how insurers analyze claims. AI algorithms can swiftly sift through massive amounts of data, identifying patterns and potential subrogation opportunities much faster than traditional methods. This speed and efficiency translate into quicker recovery times and reduced costs, ultimately benefiting policyholders through more stable premiums. For example, AI can identify complex relationships between parties involved in accidents, potentially uncovering hidden liability and maximizing recovery potential.

Blockchain: Enhancing Documentation Integrity

Blockchain technology offers exciting possibilities for improving the integrity of documentation in subrogation cases. By creating a secure and tamper-proof record of evidence, blockchain can minimize disputes regarding information validity. This secure record-keeping system streamlines the subrogation process, reducing delays and associated costs. It also creates a more transparent process for everyone involved. Understanding how legal rights apply to your assets is crucial. For example, it's important to know how to protect your retirement savings.

Automated Systems: Accelerating Recovery Timelines

Automated systems are becoming increasingly integrated into subrogation processes. These systems handle routine tasks, freeing up human resources to focus on more complex aspects of recovery. This accelerated workflow leads to faster resolution of subrogation cases, benefiting both insurers and policyholders. Automated systems can manage communication, track documents, and even generate initial liability assessments, significantly increasing overall efficiency.

Emerging Risks and New Challenges

Emerging risk areas like autonomous vehicles, cybersecurity incidents, and climate change create new subrogation challenges. The complex liability questions surrounding these areas require insurers to develop innovative recovery strategies. For instance, determining liability in accidents involving self-driving cars could involve manufacturers, software developers, or even the vehicle owner. These complexities demand sophisticated approaches to subrogation. Climate change-related events like wildfires and floods also present unique challenges, often involving multiple parties and difficult-to-assess damages. These emerging risks are reshaping the subrogation landscape and demanding ongoing adaptation from insurers.

The Impact on Policyholders

These technological and legal changes in subrogation ultimately impact policyholders. Faster recovery times, increased efficiency, and greater transparency can lead to more stable insurance premiums and a more responsive claims process. This improved system directly benefits consumers through increased financial protection and peace of mind.

Comments are closed.