What Is an Insurance Deductible? Breaking Down the Basics

An insurance deductible is simply the amount you pay out-of-pocket for covered services before your insurance company begins to pay. It's your initial financial contribution towards a covered loss. For example, if you have a $500 deductible and a $2,000 covered loss, you pay the first $500, and your insurance provider covers the remaining $1,500. This risk-sharing model between policyholders and insurers became increasingly common in the early 20th century, solidifying as standard practice by the 1950s. For more information on insurance trends, you can explore this article on global commercial insurance rates.

Types of Insurance Deductibles

Deductibles come in various forms, and understanding these differences is crucial for managing your insurance costs.

-

Flat-Dollar Deductible: This is a fixed dollar amount, such as $500 or $1,000, and is the most common and straightforward type. With a $1,000 flat deductible on car insurance, you would pay $1,000 towards repairs after an accident before your coverage begins.

-

Percentage-Based Deductible: This deductible is calculated as a percentage of your insured value. A 2% deductible on a $200,000 home insurance policy equals $4,000. This type is often used for homeowners insurance, especially for significant events.

Why Do Insurance Companies Use Deductibles?

Insurance companies use deductibles for several key reasons.

-

Discouraging Small Claims: Requiring policyholders to pay a portion of the cost discourages filing claims for minor incidents, helping keep premiums affordable for everyone.

-

Promoting Responsible Behavior: Knowing they have a deductible can encourage policyholders to take better care of their health and belongings, potentially leading to fewer claims.

-

Sharing Risk: Deductibles represent a shared financial responsibility between the insured and the insurer, allowing companies to offer more extensive coverage at manageable premium rates.

Common Deductible Misconceptions

Several misunderstandings surround insurance deductibles.

-

The Lower the Deductible, the Better: While a low deductible reduces your out-of-pocket expense when filing a claim, it often results in higher premiums. Balancing your deductible and premium is essential.

-

Deductibles Apply to Every Service: Some services, like preventive care under health insurance, may be exempt from the deductible. Review your policy details for specific information. This is especially relevant when considering long-term care, such as nursing home expenses, which may have specific tax implications.

Understanding your insurance deductible is crucial for managing your finances and making informed decisions about your coverage. By grasping these fundamental concepts, you can better navigate the insurance landscape and choose the best policy for your needs.

Navigating Deductibles Across Different Insurance Types

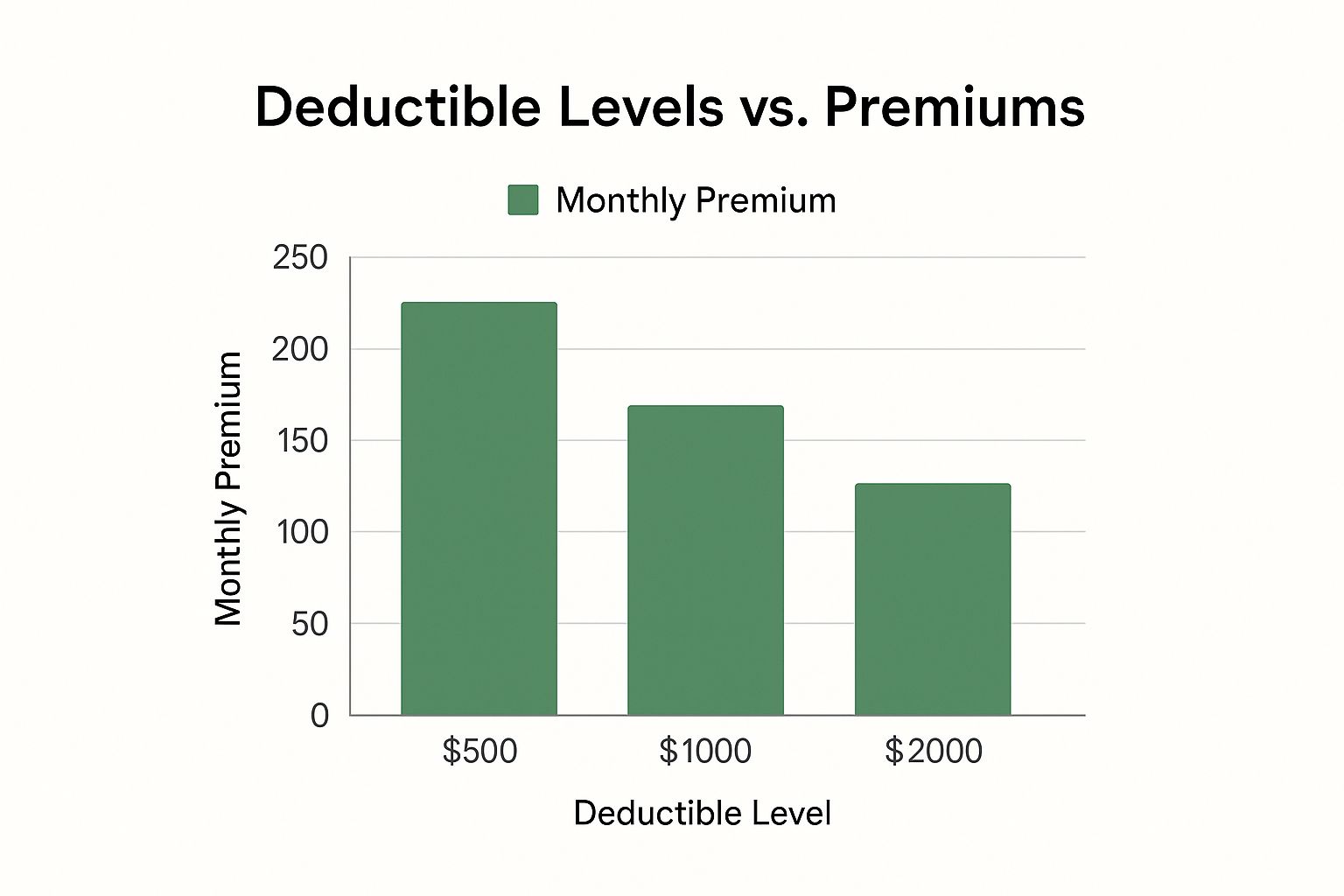

Understanding insurance deductibles is key, especially across different insurance types. Deductibles aren't universal; they vary significantly between auto, home, and health insurance. This means your approach to deductibles should be specific to each policy. The data chart above visualizes typical deductible ranges across these insurance types. Note the variations in typical ranges and how home insurance can incorporate percentage-based deductibles.

Auto Insurance Deductibles

Auto insurance typically involves two main deductibles: collision and comprehensive. Your collision deductible applies to damage from colliding with another vehicle or object. For instance, if you hit a pole causing $1,500 in damage with a $500 deductible, you pay $500, and your insurance covers the remaining $1,000.

Your comprehensive deductible covers non-collision damage, such as theft, vandalism, or weather damage. For more information on this topic, see this helpful resource: How to master the differences between comprehensive and collision coverage.

Home Insurance Deductibles

Homeowners insurance deductibles often differ from auto deductibles. You’ll find standard flat-dollar deductibles for events like fire or theft, but many policies use percentage-based deductibles for hurricanes or earthquakes. This means your deductible is a percentage of your home's insured value.

A 2% deductible on a $300,000 home would be $6,000. This significantly impacts your out-of-pocket expenses for major claims.

Health Insurance Deductibles

Health insurance adds more complexity to deductibles. Besides your annual deductible, the amount you pay before your insurance covers most services, you'll also encounter co-pays, co-insurance, and out-of-pocket maximums. These all impact your healthcare costs and interact with your deductible.

Even after meeting your deductible, you might still owe a percentage of your bills (co-insurance) until you reach your out-of-pocket maximum.

To help clarify these differences, let's look at a comparison table:

The following table, "Deductible Comparison Across Insurance Types", compares typical deductible ranges and structures across different insurance categories to help readers understand how deductibles vary by policy type.

| Insurance Type | Typical Deductible Range | Structure | Key Considerations |

|---|---|---|---|

| Auto | $250 – $1,000 | Flat-Dollar or Fixed | Collision vs. Comprehensive |

| Home | $500 – $2,000 or Percentage | Flat-Dollar or Percentage | Percentage-based for certain perils |

| Health | $1,000 – $5,000+ | Flat-Dollar | Co-pays, Co-insurance, Out-of-Pocket Maximums |

As the table highlights, deductible structures vary widely across insurance types. Auto insurance typically uses flat-dollar deductibles, while home insurance can use both flat-dollar and percentage-based amounts. Health insurance deductibles also tend to be higher and involve additional cost-sharing elements. Understanding these differences empowers you to choose the right coverage for your needs.

The Deductible-Premium Balance: Finding Your Sweet Spot

Selecting the right insurance deductible is a crucial decision. It involves balancing upfront premium costs with potential out-of-pocket expenses when you file a claim. A lower deductible often means higher premiums, while a higher deductible typically leads to lower premiums. This inverse relationship is fundamental to how insurance pricing works.

Understanding the Trade-Off

The connection between your deductible and premium comes down to risk sharing. A lower deductible means your insurer carries more risk, resulting in higher premiums. Conversely, a higher deductible shifts more risk to you, allowing for lower premium payments. For instance, raising your auto insurance deductible from $500 to $1,000 will likely reduce your annual premium.

Factors Influencing Your Decision

Your ideal deductible depends on your financial situation and risk tolerance. Consider factors like your emergency savings, comfort level with risk, and the likelihood of needing to file a claim. If you have ample savings and are comfortable with more risk, a higher deductible might be a good option. However, if your savings are limited and you prefer minimizing out-of-pocket costs, a lower deductible is probably better, even with higher premiums. When comparing health insurance deductibles, understanding industry marketing trends can be valuable. For more information, see this guide on Healthcare Marketing Strategy.

Real-World Examples

Consider homeowner's insurance. A higher deductible might save you significantly on premiums, but you would need to cover more of the repair costs if, for example, a storm damages your roof. Similarly, a higher auto insurance deductible means lower monthly payments, but you'd pay more if you were in an accident. Deductibles also influence claim frequency. Raising deductibles by 10% can decrease claim frequency by 3-5% in developed markets. You can find more detailed statistics from Aon.

To help you understand potential savings, let's examine how different deductible levels impact annual premiums across various insurance types:

Premium Savings With Different Deductible Levels

This table shows how different deductible amounts affect annual premium costs across various insurance types, helping readers understand potential savings

| Insurance Type | Low Deductible/Premium | Medium Deductible/Premium | High Deductible/Premium | Potential Annual Savings |

|---|---|---|---|---|

| Auto | $1,200/$600 | $1,000/$500 | $500/$400 | $200 |

| Home | $2,000/$800 | $1,500/$700 | $1,000/$600 | $200 |

| Health | $5,000/$400 | $3,000/$350 | $1,000/$300 | $100 |

This is an example table and the values can vary greatly depending on individual circumstances and the insurance provider. It's important to get personalized quotes to understand your potential savings.

Finding the Right Balance

Choosing the right deductible-premium balance requires a strategic approach. Weigh potential savings against your capacity to handle unexpected costs. Also, understand how deductibles work across different insurance types—auto, home, and health—each with its own considerations. By carefully assessing your finances and understanding deductibles, you can choose one that offers suitable protection without overspending.

When Disaster Strikes: How Deductibles Impact Claims

Understanding insurance deductibles is important, but seeing how they work in real-world claim scenarios provides a clearer picture. This section walks you through the claims process, from initial damage assessment to the final insurance payout, highlighting your deductible's role.

Real-World Claim Scenarios: Putting Deductibles into Action

Let's use some examples to illustrate how deductibles work in practice:

-

Scenario 1: Hailstorm Damage: Imagine a hailstorm damages your roof. Repairs are estimated at $12,000, and your homeowner's insurance policy has a $1,000 deductible. You pay the $1,000 deductible, and your insurance company covers the remaining $11,000.

-

Scenario 2: Fender Bender: A minor car accident causes $2,500 in damage to your vehicle. Your collision deductible is $500. You're responsible for the $500 deductible, and your insurance pays the remaining $2,000.

-

Scenario 3: Emergency Appendectomy: An unexpected appendectomy results in a $15,000 medical bill. Your health insurance deductible is $2,000. You pay the $2,000 deductible, and your insurance covers the remaining $13,000. Remember that co-insurance and out-of-pocket maximums can still impact your final costs.

Common Deductible Questions Answered

This section addresses frequently asked questions about insurance deductibles and how they function during a claim.

-

Do You Physically Pay the Deductible to Someone? Typically, you pay your deductible directly to the repair shop, contractor, or healthcare provider. In some cases, you might pay the insurance company directly, who then pays the provider. This process varies depending on the situation and your insurer's procedures.

-

What if the Damage Costs Less Than Your Deductible? If the damage is less than your deductible, you cover the entire cost. For example, with a $1,000 deductible and $800 in repairs, your insurance wouldn't pay anything.

-

How Do Multiple Claims in One Year Work? This depends on the insurance type. Health insurance deductibles are usually met once per calendar year. Home or auto insurance deductibles typically apply per incident. Two separate car accidents in one year would likely mean paying your deductible twice.

Time is Money: Deductible Reset Periods

Knowing when your deductible resets is essential. Health insurance deductibles typically reset on January 1st. Property insurance deductibles, however, reset per incident. This difference means you could face multiple deductibles in a single year for property claims, particularly during a season with multiple events like hurricanes and tornadoes. Understanding this, as seen in discussions regarding Hurricane Milton’s impact and subsequent tornado damage, can save you money. Careful consideration of these factors can significantly affect your expenses.

Beyond the Basics: Special Deductible Structures Explained

While standard deductible structures are fairly common, insurance deductibles aren't always so simple. Specialized structures, sometimes hidden within the policy's fine print, can significantly impact your out-of-pocket expenses. Understanding these variations is essential for anyone wanting to grasp the full implications of an insurance deductible.

Disappearing and Split Deductibles

Some policies offer disappearing deductibles, rewarding clients who remain claim-free. For example, each year without a claim could reduce your deductible by a specific amount, potentially eliminating it entirely. This encourages responsible behavior and can result in long-term cost savings. Split deductibles apply different amounts to different claim types. You might have a lower deductible for fire damage and a higher one for water damage, reflecting the varying risks and associated costs of specific incidents.

Aggregate and Catastrophe Deductibles

Aggregate deductibles accumulate expenses across multiple incidents within a defined period. If your policy has a $2,000 aggregate deductible, you'll pay up to that amount for all covered losses combined during the year. Once you meet the aggregate, the insurance company covers subsequent claims fully. You might be interested in: How to master homeowners insurance policy. Catastrophe deductibles apply to major events like hurricanes, earthquakes, or floods. These deductibles are usually percentage-based and can be considerably higher than standard deductibles, often surprising homeowners. This is particularly important for those living in disaster-prone areas.

In the U.S., the average annual deductible for employer-sponsored health plans increased by 68% between 2006 and 2020, from $303 to $1,644. Globally, property insurance deductibles typically range from 1-5% of insured values. More detailed statistics can be found here.

Family vs. Individual Health Insurance Deductibles

Health insurance deductibles can work differently for families. Individual deductibles apply to each person covered under the policy. Each family member must meet their individual deductible before coverage begins. Family deductibles combine the medical expenses of all family members toward the total deductible. Once the family reaches that threshold, the insurer covers expenses for everyone. Understanding these nuances, especially for larger families, is crucial for healthcare budgeting.

These varied deductible structures highlight the importance of reviewing your policy details. It’s vital to understand how your insurance will respond in different circumstances. By understanding how deductibles work, especially the specialized structures discussed here, you'll be better equipped to make informed decisions about your coverage and avoid unexpected costs when filing a claim.

Choosing Your Ideal Deductible: A Strategic Approach

Selecting the right insurance deductible is a crucial financial decision. It's not simply about comparing numbers, but about understanding how your deductible choice impacts your overall financial well-being. This guide will help you navigate the process of choosing a deductible that aligns with your individual circumstances.

Evaluating Your Financial Resilience

Before settling on a deductible, it's important to assess your ability to handle unexpected costs. This involves considering several factors:

-

Emergency Funds: Your emergency fund serves as a financial safety net. Ideally, it should be sufficient to cover your chosen deductible. For example, if you only have $3,000 in savings, a $5,000 auto insurance deductible might create financial strain if you need to file a claim.

-

Cash Flow Stability: Stable income and predictable expenses make it easier to absorb unexpected costs. If your income fluctuates, a lower deductible might provide greater financial security.

-

Risk Comfort Level: Consider your personal comfort level with financial risk. If you prefer to minimize out-of-pocket expenses, a lower deductible is generally recommended. If you're more comfortable assuming risk, a higher deductible can result in lower premiums.

Targeted Recommendations Based on Life Stages

The ideal deductible varies depending on your stage of life. Different life stages present unique financial considerations:

-

Young Renter: Limited savings often make lower deductibles a better choice, even with higher premiums. This helps protect against depleting already scarce financial resources.

-

Growing Family: Juggling multiple financial priorities often necessitates finding ways to save on premiums. A moderate deductible can offer a balance between cost and coverage.

-

Established Homeowner: With greater financial stability and more assets to protect, a higher deductible combined with a robust emergency fund can be a sensible strategy.

Reassessing Your Deductibles

Your ideal deductible is not fixed; it should evolve with your circumstances. Regularly review your deductibles, especially during periods of significant change:

-

Life Events: Major life events such as marriage, having children, buying a home, or a substantial change in income warrant a review of your deductible choices.

-

Annual Review: Use your annual insurance policy review as an opportunity to reassess your deductibles. Adjust them as needed based on your current financial situation and risk tolerance.

-

Changes in Insurance Landscape: New policy options or regulatory changes in the insurance industry can also create a need to review your deductibles.

By strategically choosing and regularly reviewing your insurance deductibles, you can optimize your coverage for both protection and affordability. Consider your individual needs and make informed decisions to ensure your insurance aligns with your evolving life.

Deductible Pitfalls: Mistakes Smart Consumers Avoid

Choosing the right insurance deductible is a balancing act. It involves finding the right compromise between affordable premiums and manageable out-of-pocket expenses when you need to make a claim. Even careful consumers can make common mistakes when selecting their deductibles. This section highlights those pitfalls and offers strategies to avoid them.

Overlooking Emergency Savings

One of the biggest mistakes is choosing a deductible without considering your emergency fund. Your deductible is the amount you'll pay before your insurance coverage begins. If your deductible is more than your available savings, you could face financial difficulty if an unexpected event occurs. For example, choosing a $2,000 deductible with only $1,000 in savings could leave you struggling to cover the remaining $1,000 when filing a claim. The solution? Align your deductible with your actual financial capacity.

Focusing Solely on Premium Savings

Lower premiums are tempting, but focusing only on saving money on premiums by choosing a high deductible can be a mistake. A high deductible means higher out-of-pocket expenses when you file a claim. This can offset any premium savings you've gained. For example, a $500,000 home might have a $5,000 deductible (2%), and commercial policies can sometimes exceed 5% in catastrophe-prone areas. Learn more about commercial insurance rates. While appealing initially, this high deductible could be financially devastating in the event of a major loss. The key is to balance potential premium savings with your ability to comfortably pay the deductible.

Applying the Same Deductible Across All Policies

Another common error is using the same deductible for all insurance policies. Your risk exposure and financial implications are different for various types of insurance, such as auto, home, and health insurance. A blanket deductible approach doesn't consider these important differences. You might be comfortable with a higher deductible for auto insurance but prefer a lower deductible for health insurance, reflecting different priorities and potential costs. You might be interested in: How to master health insurance deductibles. The best approach is to evaluate each policy separately, choosing a deductible based on the specific risks and potential financial impact.

Ignoring Policy Details and Definitions

Not fully understanding your policy’s definitions can also lead to unexpected costs. For example, the definition of a "hurricane" or "hurricane windstorm" can determine whether a standard deductible or a significantly higher hurricane deductible applies, especially with tornado damage outside hurricane-force wind areas. This lack of clarity can lead to unforeseen out-of-pocket expenses. Carefully review your policy's definitions and deductible clauses to avoid surprises when you file a claim.

By avoiding these common mistakes, consumers can make informed choices about insurance deductibles. This means understanding the relationship between premiums, deductibles, and emergency savings, tailoring deductibles to each type of policy, and thoroughly reviewing policy details. This strategic approach ensures your insurance provides effective protection without causing undue financial strain.

Comments are closed.