Demystifying Umbrella Insurance

Think of umbrella insurance as an extra layer of financial protection. It safeguards your assets when accidents occur and your standard insurance policies fall short. This supplemental coverage acts as a safety net, shielding you from the potentially devastating costs of major claims and lawsuits, especially those involving significant property damage or serious injuries.

How Umbrella Insurance Works

Umbrella insurance activates when the liability limits of your existing home, auto, or other personal liability policies are exhausted. For example, if you cause a car accident resulting in substantial medical expenses for another driver, and those expenses surpass your auto insurance limits, your umbrella policy would step in. The umbrella policy then covers the remaining costs, up to its own limits, preventing you from paying out of pocket.

Umbrella insurance is a form of excess liability coverage protecting individuals and businesses from major claims and lawsuits. It provides an additional layer of financial protection beyond the limits of primary insurance policies. For example, umbrella insurance can protect assets from unforeseen legal liabilities arising from accidents, injuries, or other incidents exceeding standard policy limits. As litigation costs have risen historically, so has the demand for umbrella insurance as a safeguard. In recent years, the costs of litigation and jury awards have increased significantly, leading to higher premiums for umbrella policies. This underscores the growing importance of umbrella insurance as a risk management tool. Explore this topic further here.

Who Needs Umbrella Insurance?

While often associated with the wealthy, umbrella insurance can benefit anyone seeking to protect their assets. Several factors can increase your need for this coverage:

- Owning a home: Homeowners face potential liability claims from injuries on their property.

- Driving frequently: More time on the road increases the risk of accidents.

- Having teenage drivers: Statistically, young drivers are more prone to accidents.

- Owning a dog: Dog bites can result in costly medical bills and lawsuits.

- Hosting frequent gatherings: Guests in your home increase the potential for accidents and liability.

Why Umbrella Insurance Is Essential

Even with significant assets, the costs of a major lawsuit can quickly deplete savings and jeopardize your financial future. Umbrella insurance offers a crucial safeguard, protecting you from financial ruin due to unforeseen circumstances. It provides peace of mind, knowing you have an added layer of protection. It can also cover certain liabilities, such as libel or slander, not covered by standard policies. Ultimately, umbrella insurance offers a cost-effective way to gain substantial financial protection against potentially devastating liabilities.

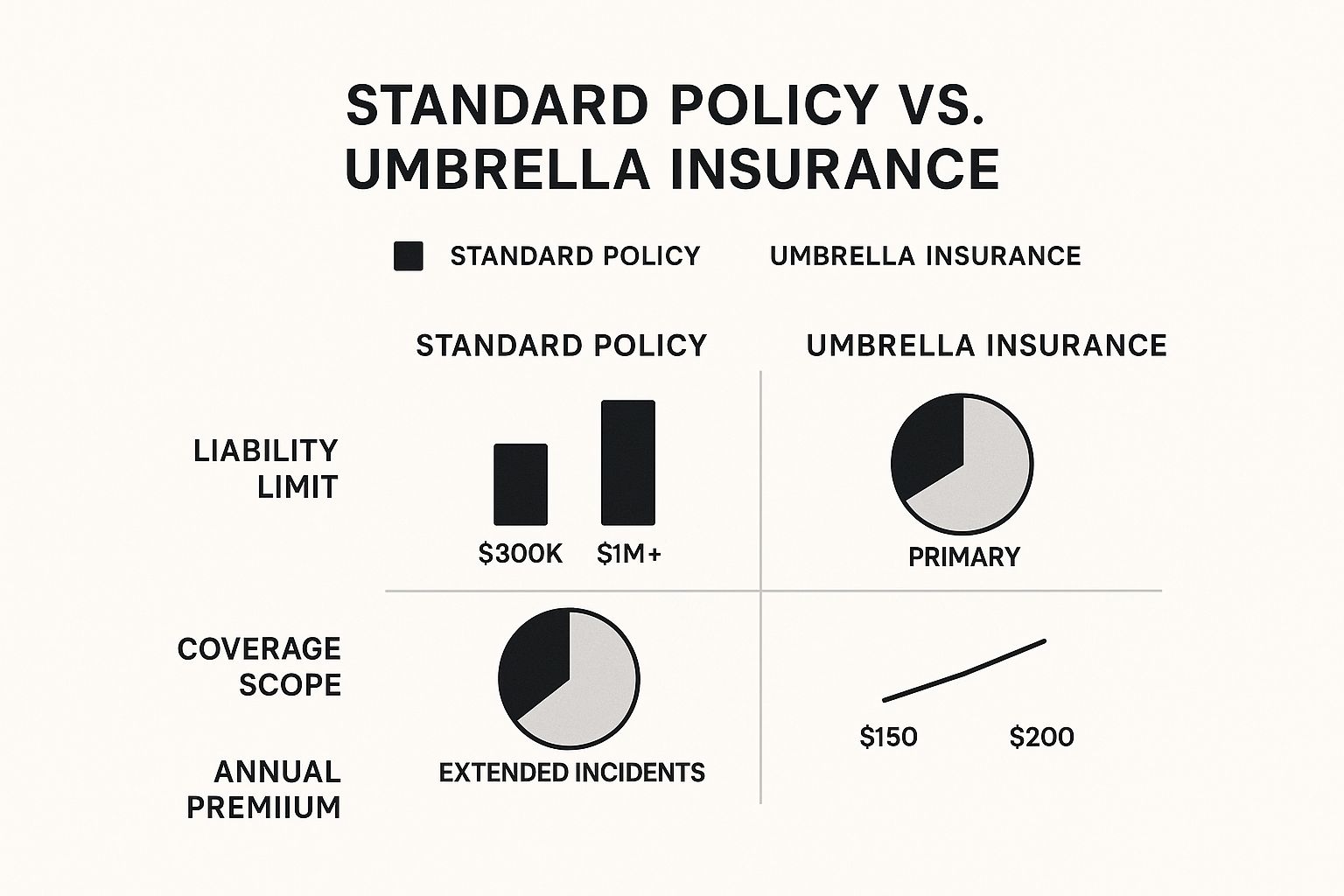

How Umbrella Coverage Actually Works

This infographic compares standard liability insurance with umbrella insurance, examining liability limits, coverage scope, and annual premiums. Notice how umbrella insurance provides significantly increased liability coverage and a broader scope of incidents, at a relatively small additional cost. This makes it a practical way to gain substantial financial protection.

This section explains how umbrella insurance works in practice. It supplements your existing liability coverage, such as auto or homeowners insurance. It activates when those policies reach their limits. Importantly, umbrella insurance extends your existing coverage—it doesn't replace it.

Coordinating With Existing Insurance

Umbrella insurance acts as a secondary layer of protection. For instance, if you have a $300,000 liability limit on your auto insurance policy and you cause an accident resulting in $500,000 in damages, your auto insurance will pay up to its $300,000 limit. Your umbrella policy would then step in, covering the remaining $200,000 and protecting you from significant personal financial loss.

Covered Liability Events

Umbrella insurance covers a broad range of liability events. This includes bodily injury or property damage that you cause to others. It can also cover claims not typically covered by standard policies, such as libel, slander, or defamation of character. However, there are usually exclusions, such as intentional acts of harm and damage to your own property.

Identifying Protection Gaps

Umbrella insurance helps fill critical gaps in standard insurance policies. For example, standard homeowner's insurance may not fully cover a lawsuit resulting from a dog bite. An umbrella policy provides additional protection in such cases, safeguarding your assets from unexpected legal expenses.

To illustrate this further, let's look at a comparison table:

Umbrella Insurance vs. Standard Liability Coverage

This table compares the key differences between standard liability insurance and umbrella policies.

| Feature | Standard Liability Coverage | Umbrella Insurance |

|---|---|---|

| Purpose | Covers common liability claims up to a specified limit | Provides additional liability coverage beyond the limits of underlying policies |

| Coverage Amount | Relatively lower limits | Significantly higher limits, typically in $1 million to $5 million increments |

| Cost | Included as part of underlying policies (e.g., auto, home) | Separate policy with an additional premium |

| Scope | Specific to the underlying policy (e.g., auto accidents, home incidents) | Broader scope, covering a wider range of liability claims, including libel and slander |

| Examples | Pays for damages up to your policy limit in a car accident | Covers the excess damages beyond your auto policy limit in a major accident; may also cover legal defense costs in a defamation lawsuit |

This table highlights how umbrella insurance complements, rather than replaces, standard liability policies. It provides a higher level of protection and a wider scope of coverage for a relatively modest cost.

These protection gaps are often discovered only after an incident has occurred, underscoring the importance of reviewing your existing coverage and considering potential vulnerabilities. This proactive assessment can save you significant financial hardship in the future.

Are You Exposed? Who Truly Needs Umbrella Coverage

Many people underestimate their risk until they're facing a costly lawsuit. This section helps you assess your personal liability exposure. We'll explore how everyday activities, from hosting gatherings to driving, can create vulnerabilities not fully covered by standard insurance policies.

Evaluating Your Personal Risk

Think about your daily life. Do you own a home, a dog, or a car? Do you have teenage drivers in your household? Do you host parties or social events? These ordinary activities can expose you to significant liability.

For example, a dog bite on your property could result in a lawsuit that exceeds your homeowner's insurance liability limits. A car accident caused by a teenage driver could lead to substantial medical and legal expenses.

Consider your assets. The more you have to protect—homes, investments, savings—the greater your potential loss in a lawsuit. This doesn't mean umbrella insurance is only for the wealthy.

Anyone with assets they want to protect should consider the benefits of this added security. Umbrella insurance is a key element of broader financial planning; learn more about asset protection strategies.

Life Stages and Wealth Levels

Your need for umbrella insurance changes over time. Young adults with limited assets might view it as optional. However, as you build wealth and your family grows, the need for comprehensive liability protection increases.

A family with young children faces different risks than a retired couple. Children, especially teenagers, can significantly increase liability exposure from driving incidents to accidents at home. You might be interested in Ranking the Best Car Insurance Companies of 2025.

Professions and Liability

Certain professions carry increased liability risks. Doctors, lawyers, and board members, for example, are more likely to face lawsuits related to their professional activities.

Even if your employer provides some coverage, an umbrella policy can offer valuable additional protection for your personal assets.

Determining Your Need

Determining your need for umbrella insurance requires an honest assessment of your potential liabilities. Consider the following:

- Your assets: What could you lose in a lawsuit?

- Your lifestyle: Do your activities increase your risk?

- Your profession: Are you exposed to professional liability claims?

By carefully considering these factors, you can make an informed decision about whether umbrella coverage is essential, recommended, or optional for your situation. This proactive approach can protect your financial future and provide peace of mind.

The Evolving Commercial Umbrella Landscape

The business world is constantly shifting, bringing new risks for companies to address. Liability protection is no longer a static concern but a dynamic area where businesses must constantly adapt. Commercial umbrella insurance, providing extra liability coverage beyond standard policies, is increasingly important in this environment. This means companies of all sizes and across industries are seeing umbrella policies as crucial for risk management.

Adapting to Modern Business Threats

Traditional business insurance policies often lack the scope to address the complex liabilities of today’s business world. Factors like the increase in remote work, a growing social media presence, and complex global supply chains create new vulnerabilities rarely covered by standard policies. For instance, a data breach stemming from a remote employee's unsecured home network could result in major legal costs and reputational harm, potentially exceeding the limits of a standard cyber liability policy.

Social media activity can also expose businesses to defamation lawsuits and other reputational risks, requiring strong legal defenses and potentially high expenses. Supply chain disruptions can similarly lead to contract disputes and financial losses that might not be fully covered by standard business insurance. These are the scenarios where commercial umbrella insurance offers critical protection.

Why Umbrella Insurance Is No Longer Optional

The commercial umbrella insurance market is experiencing considerable growth, reflecting the rising need for businesses to protect themselves against unforeseen liabilities. As of 2024, the market size was around USD 17.99 billion and is projected to reach USD 19.64 billion in 2025. This growth highlights the significance of umbrella insurance in the corporate world, particularly given global challenges like supply chain issues and cybersecurity risks. The market is expected to keep expanding as businesses seek to mitigate financial risks related to catastrophic events, contractual issues, and litigation. You can find more detailed statistics here.

This trend demonstrates that umbrella insurance is now a necessity for effective risk management, not just a beneficial extra. Businesses are increasingly prioritizing the protection of their assets and financial stability when facing potentially devastating liabilities. This proactive strategy is becoming more and more essential for maintaining a competitive edge in today's complex business environment.

Structuring Umbrella Coverage for Emerging Risks

Companies that are planning for the future are actively adjusting their umbrella coverage to account for new and developing risks. This involves thoroughly assessing potential exposures and collaborating with insurance professionals to create customized policies. They are going beyond simply buying a standard umbrella policy and focusing on solutions tailored to the particular challenges of their industry and operations. This strategic approach allows businesses to navigate the changing risk landscape with confidence, protecting their future.

Understanding Your Premium: Cost Factors That Matter

Umbrella insurance offers valuable financial protection beyond your standard policies. But what determines the cost of this added security? Understanding the factors influencing your umbrella insurance premium is essential for finding the right balance of coverage and affordability. These factors range from the coverage amount you select to the claims history in your area.

Coverage Limits and Your Location

One of the most direct factors impacting your premium is the coverage limit. Just like a larger house costs more, a higher coverage limit on your umbrella policy will result in a higher premium. A $2 million policy will typically be more expensive than a $1 million policy. Location also matters. Areas with a higher incidence of lawsuits or larger average settlements often have higher umbrella insurance premiums due to the increased risk for insurance companies.

Where you live can significantly impact your rate. For example, if you live in an area with a higher cost of living or a higher rate of litigation, you might pay a higher premium. Insurers assess the risk in different geographic areas and adjust premiums accordingly.

Lifestyle and Risk Factors

Certain lifestyle choices and risk factors can also affect your umbrella insurance premium. Owning a swimming pool or trampoline can increase your liability risk, potentially leading to higher premiums. These are often considered attractive nuisances, meaning they could attract children and potentially lead to accidents. Similarly, having teenage drivers on your policy usually increases premiums because younger drivers statistically have a higher risk of accidents. Even certain dog breeds, especially those with a history of aggressive behavior, can influence your rate due to the potential for liability claims.

Claims History and Underlying Coverage

Your personal claims history is a significant factor in determining your umbrella insurance premium. A history of accidents or liability claims suggests a higher risk, potentially leading to higher premiums. The adequacy of your underlying home and auto insurance coverage also plays a role. Umbrella policies require certain minimum liability limits on these underlying policies. If your existing coverage falls short of these minimums, insurers may charge a higher premium or even decline coverage. For more guidance on home insurance, see The Ultimate Guide to Choosing the Right Home Insurance Policy in 2025.

To understand how these and other factors combine to affect your umbrella insurance premium, let's take a look at the following table. It breaks down some of the key elements and their potential impact.

| Factor | Impact on Premium | Risk Level |

|---|---|---|

| Coverage Limit | Higher limit = Higher Premium | Variable |

| Location | Higher risk areas = Higher Premium | Variable |

| Swimming Pool/Trampoline | Increases Premium | High |

| Teenage Drivers | Increases Premium | High |

| Dog Breeds (Certain) | May Increase Premium | Moderate |

| Claims History | More claims = Higher Premium | Variable |

| Underlying Coverage Limits | Insufficient coverage = Higher Premium | Moderate |

This table summarizes some of the key influences on umbrella insurance premiums. As you can see, various elements contribute to the overall cost.

Recent Pricing Trends in the Umbrella Insurance Market

Beyond individual factors, market trends also influence umbrella insurance costs. Umbrella insurance rates, particularly for high-hazard classes, are predicted to increase substantially in 2025. Forecasts indicate potential increases of 10% to 20% for high-hazard/challenged classes and 8% to 15% for low/moderate hazard classes. Several factors contribute to these projected increases, including rising legal costs and the effect of social inflation on insurance claims. Insurance marketplace realities further highlight the challenges facing the personal umbrella policy market, including decreased capacity and escalating litigation expenses. These market dynamics can result in higher premiums even for individuals with a clean driving record and no prior claims.

Strategies for Reducing Costs

While numerous factors affect umbrella insurance premiums, you can take proactive steps to manage your costs. Bundling your umbrella policy with your home and auto insurance from the same carrier often leads to discounts. Increasing your deductibles on your underlying policies can also lower your umbrella premium. Improving your home safety by installing security systems or addressing potential hazards can reduce your risk profile, potentially leading to lower premiums. Regularly reviewing your coverage with your insurance agent ensures you have the appropriate level of protection at the most competitive price. By taking these steps, you can significantly impact the cost of your umbrella insurance while maintaining the coverage you need.

Busting Umbrella Insurance Myths That Cost You

Many misconceptions surround umbrella insurance, often leaving individuals underprotected. Let's dispel some common myths and explore the true value of this important coverage.

Myth 1: Umbrella Insurance Is Only for the Wealthy

This is perhaps the biggest misconception about umbrella insurance. While significant assets certainly benefit from this type of coverage, it's not reserved solely for the affluent. Anyone facing a lawsuit risks losing their home, savings, and future income. An umbrella policy offers crucial protection for your assets, regardless of your net worth, for a relatively small annual premium.

Myth 2: My Existing Insurance Is Enough

Standard insurance policies, such as auto and homeowner's insurance, have liability limits. If you cause an accident resulting in $500,000 in damages, but your auto insurance only covers $300,000, you're personally liable for the difference of $200,000. Umbrella insurance bridges this gap, extending coverage beyond your existing policy limits and shielding you from substantial financial repercussions.

Myth 3: Umbrella Insurance Is Too Expensive

The cost of umbrella insurance is surprisingly affordable, typically ranging from $150 to $300 annually for $1 million in coverage. This modest investment can provide significant financial protection in the event of a major claim. In reality, not having umbrella insurance can have a far greater financial impact than the premiums themselves. For more about financial planning and life insurance, see: The Ultimate Guide to Life Insurance.

Real-World Examples: Where Myths Meet Reality

Imagine a dog bite incident on your property resulting in a lawsuit exceeding your homeowner's insurance limits. Without umbrella insurance, you would be responsible for the remaining expenses. Similarly, consider a car accident caused by a teenage driver leading to substantial medical bills. Again, umbrella insurance can provide vital financial protection.

These scenarios are not just hypothetical; they reflect the real-life challenges many people face each year. Misunderstandings about umbrella insurance can lead to severe financial consequences. By understanding the facts, you can make informed decisions about your insurance needs and avoid potentially costly mistakes.

Selecting Coverage That Actually Protects You

Choosing the right umbrella insurance policy isn't just about finding the cheapest option. It's about strategically assessing your risks and selecting coverage that truly protects your assets. This involves carefully considering your liability exposure and understanding the details of policy features and exclusions.

Assessing Your Personal Liability Exposure

Before shopping for umbrella insurance, evaluate your potential vulnerabilities. Consider your assets, lifestyle, and profession. Ask yourself: What could you lose in a lawsuit? Do activities like frequent driving or pet ownership increase your risk? Does your profession expose you to professional liability claims? Many underestimate their liability until facing a claim. Accurately assessing your risk is the first step towards proper protection.

Determining Appropriate Coverage Limits

Once you've assessed your risk, determine appropriate coverage limits. While $1 million is a common starting point, you might need more depending on your assets and potential liabilities. If you own multiple properties, have substantial investments, or have a higher risk of being sued, a $2 million or $3 million policy might be better. The key is ensuring your umbrella policy covers your assets in a worst-case scenario.

For example, if your net worth is $2 million, a $1 million umbrella policy may not be enough. A serious accident resulting in a multi-million dollar judgment could leave you personally liable for a significant amount.

Understanding Policy Features and Exclusions

Not all umbrella policies are the same. Pay close attention to policy features and exclusions. Some policies offer broader coverage than others, including protection for libel, slander, or false imprisonment. However, common exclusions exist, like intentional acts of harm or damage to your own property.

Understanding these nuances is crucial. Small wording differences can significantly impact coverage. One policy might cover legal defense costs while another doesn't, potentially saving you thousands in legal fees.

Coordinating with Underlying Policies

Your umbrella policy works with your underlying home, auto, and other liability insurance policies. Ensure these underlying policies meet the minimum liability limits required by your umbrella insurer. Failing to meet these requirements can create coverage gaps.

Your underlying policies are the foundation, and your umbrella policy provides additional coverage. If the foundation is weak, the whole structure is compromised. Work with your insurance professional to ensure your underlying coverage and umbrella insurance work together seamlessly.

Working with Insurance Professionals and Regularly Reassessing Coverage

Don't hesitate to seek guidance from insurance professionals. They can help you navigate umbrella insurance and find a suitable policy. They can also explain policy features, exclusions, and coverage limits to help you make informed decisions.

Finally, remember your insurance needs change. Regularly reassess your coverage, especially after major life events like buying a home, getting married, or having children. These changes can impact your liability and necessitate adjustments to your umbrella insurance. Staying informed and proactive ensures your umbrella coverage continues providing the protection you need.

Comments are closed.