What Is Gap Insurance? The Protection Most Drivers Miss

Gap insurance, also known as Guaranteed Asset Protection insurance, offers specialized coverage to protect you from financial hardship if your vehicle is totaled or stolen. This protection is particularly important when the actual cash value (ACV) of your car is less than the outstanding balance on your auto loan or lease.

For example, imagine your car is worth $20,000, but you still owe $25,000 on your loan. Standard auto insurance will typically cover only the $20,000 ACV. This leaves you with a $5,000 difference, often referred to as "the gap," that you would be responsible for paying. Gap insurance steps in to cover this $5,000 gap, preventing a significant financial burden.

How Gap Insurance Works

Gap insurance coverage hinges on the difference between your car's market value and what you owe on your financing. This difference can be especially noticeable with new cars, which often depreciate quickly. Longer loan terms and smaller down payments can further contribute to a higher loan balance compared to the car’s decreasing value, widening this gap.

This means you could owe more on your loan than the car is worth for an extended period, making gap insurance a valuable consideration.

The Growing Importance of Gap Insurance

The need for gap insurance is increasingly apparent in today's automotive market. Factors like rising vehicle costs, common financing practices, and greater awareness of gap insurance benefits have contributed to its growing popularity.

The global guaranteed auto protection market was valued at approximately $3.97 billion in 2024. Projections indicate this market will reach $6.48 billion by 2029, representing a 10.3% compound annual growth rate. This impressive growth underscores the increasing recognition of gap insurance's role in mitigating financial risk associated with vehicle financing. Learn more about gap insurance market trends.

Key Scenarios Where Gap Insurance Is Crucial

Certain situations make gap insurance especially advisable. These include:

- Leasing a Vehicle: Lessees are often responsible for the difference between the vehicle’s residual value and the outstanding lease balance if the vehicle is totaled. Gap insurance helps cover this potential cost.

- Financing with a Small Down Payment: A smaller down payment leads to a larger loan amount, increasing the likelihood of a gap between the loan balance and the car’s actual value.

- Financing with a Long Loan Term: Loan terms of 72 or 84 months extend the time you might owe more than the car's worth.

- Owning a Rapidly Depreciating Vehicle: Some car models lose value faster than others. Gap insurance can provide valuable protection in these cases.

By understanding how gap insurance works and its potential benefits, you can make a well-informed decision about whether this type of coverage suits your individual financial situation and driving circumstances.

The Depreciation Dilemma: Why Your Car's Value Plummets

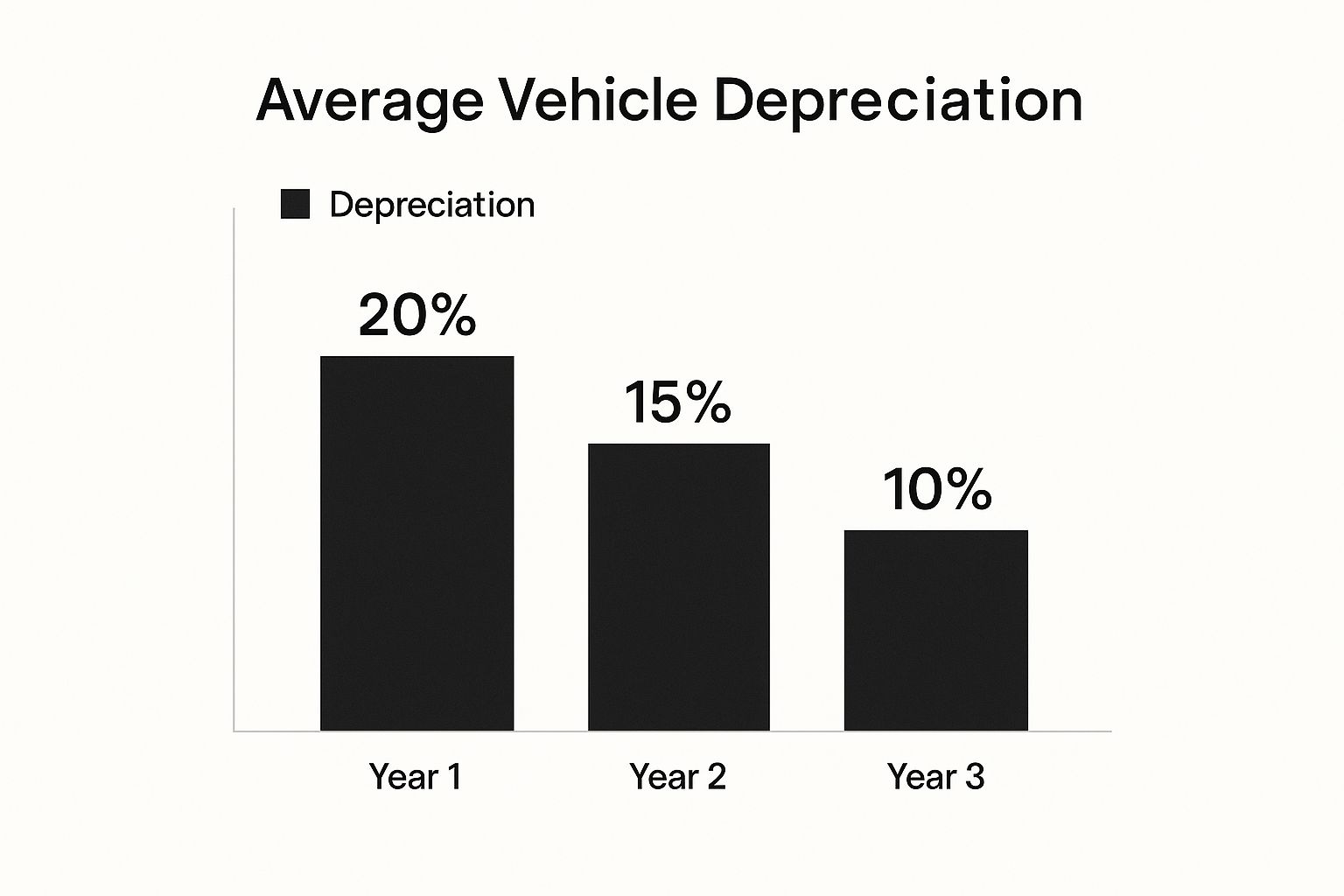

That new car smell fades quickly, and unfortunately, so does its value. Depreciation, the decrease in an asset's value over time, significantly impacts car owners. The moment you drive off the dealership lot, your car's value starts to decline, and this drop can be substantial, particularly within the first few years. The infographic below illustrates this typical depreciation curve.

As shown, a new car can lose 20% of its value in the first year, followed by another 15% in the second and 10% in the third. This rapid depreciation can create a significant gap between your car's worth and the outstanding balance on your auto loan. This difference is the “gap” that gap insurance is designed to address.

Understanding the Depreciation Curve

Several factors influence a car's depreciation rate. Key factors include the make and model, mileage, condition, and even current market demand. Popular, in-demand vehicles often hold their value better than less-desirable models.

How you finance your vehicle also significantly affects your vulnerability to depreciation. Longer loan terms (like 72 or 84 months) are increasingly prevalent, meaning you’re potentially “underwater” on your loan for an extended period. Combined with minimal down payments, these longer loan terms exacerbate the impact of depreciation, widening the gap between your loan balance and the car’s actual cash value.

Why Depreciation Matters for Gap Insurance

The depreciation dilemma is the core reason gap insurance exists. If your car is totaled or stolen, your standard auto insurance policy typically pays out only the actual cash value (ACV) of your car at the time of the loss. If your loan balance exceeds the ACV, you’re responsible for the difference.

Gap insurance covers this financial gap, preventing you from paying out of pocket for a car you no longer own. The gap insurance market is expected to see substantial growth, with projections of a CAGR of 4.8% to 10.3%. This growth reflects increasing awareness of this financial risk. Learn more about the gap insurance market growth.

Understanding depreciation is crucial for informed financial decisions, especially concerning a total loss. Knowing your car's depreciation rate helps assess your need for gap insurance and how this coverage can protect you from financial hardship.

The table below demonstrates how a vehicle's value depreciates faster than a typical loan balance, creating the "gap" that gap insurance covers.

Vehicle Depreciation vs. Loan Balance Over Time

| Time Period | Average Vehicle Value | Typical Loan Balance | The Gap |

|---|---|---|---|

| Year 1 | $24,000 | $25,000 | $1,000 |

| Year 2 | $20,400 | $22,000 | $1,600 |

| Year 3 | $18,360 | $18,000 | $360 |

| Year 4 | $16,524 | $13,000 | -$3,524 |

| Year 5 | $14,872 | $7,000 | -$7,872 |

Note: These figures are illustrative and can vary significantly depending on the specific vehicle, loan terms, and other factors.

This table highlights how, in the initial years, the loan balance often surpasses the vehicle's value. This difference, represented in "The Gap" column, shows the potential financial burden in case of a total loss. As the loan is paid down, the gap decreases, and eventually, the vehicle's value may exceed the loan balance.

Do You Actually Need Gap Insurance? Honest Answers

Gap insurance isn't a universal solution. It can be valuable in specific situations, but it's not always essential. Understanding your financial situation and vehicle details will help you decide if gap insurance is right for you. This includes evaluating your loan or lease terms, down payment, and your vehicle's depreciation rate.

When Gap Insurance Is a Must-Have

There are times when gap insurance is highly recommended. Leased vehicles often require gap coverage because of the potential difference between the residual value and the outstanding lease balance if the vehicle is totaled. Financing a car with a small down payment or a long loan term (like 72 or 84 months) also increases the risk of owing more than the car's worth.

A smaller down payment means a larger loan balance. Longer loan terms extend the time your loan balance could be higher than the vehicle's depreciated value. Some car models also depreciate faster than others, making gap insurance more critical.

When You Might Skip Gap Insurance

If you made a large down payment (20% or more) and have a shorter loan term, you might not need gap insurance. This is because you'll gain equity in your vehicle faster, reducing the time your loan balance might be greater than its value. Some drivers also skip gap insurance if they can afford to pay the potential difference if their car is totaled.

Those with significant savings might prefer to self-insure this risk. This requires careful financial planning and a comfortable level of risk tolerance. Ultimately, the decision comes down to your personal risk assessment and financial preparedness.

The Bigger Picture of Financial Protection

The idea of a "protection gap" isn't limited to car loans. The global insurance protection gap—the difference between economic losses from disasters and insured amounts—is widening. As of 2025 forecasts, the Asia-Pacific region accounts for almost half of all uninsured losses. Learn more about the global insurance protection gap. This includes things like inadequate homeowners insurance for hurricanes or earthquakes.

While this gap applies to all insurance types, the vehicle loan protection gap (the issue gap insurance addresses) is especially relevant to auto financing. In markets like the U.S., where car financing and leasing are common, this protection gap creates a significant financial risk. This risk highlights the importance of understanding what gap insurance is and how it can protect consumers from financial burdens if their car is totaled or stolen. Understanding what gap insurance is is a key part of responsible car ownership.

Gap Insurance vs. Other Coverage: What's Actually Different

Don't waste money on potentially overlapping car insurance coverage. This section clarifies how gap insurance interacts with your other auto insurance, highlighting key differences and helping you avoid redundant protection. Understanding how gap insurance differs from your standard comprehensive coverage is particularly important.

Comprehensive vs. Gap: Understanding the Purpose

Comprehensive insurance protects your vehicle from damage caused by incidents like theft, vandalism, or weather. However, the payout is limited to the actual cash value (ACV) of your car at the time of loss. This can be problematic if you owe more on your loan than the car is worth, leaving you responsible for the difference.

Gap insurance steps in to cover this "gap" between the ACV and your outstanding loan balance after a total loss or theft. It's designed as a supplement to comprehensive coverage, not a replacement, and is only relevant if your car is totaled or stolen.

Loan/Lease Payoff and New Car Replacement: Exploring the Nuances

Some policies offer new car replacement coverage or loan/lease payoff provisions, which may seem similar to gap insurance but have important distinctions. New car replacement usually allows you to buy a brand new vehicle of the same make and model if yours is totaled within a specific period, often the first year of ownership.

Loan/lease payoff provisions, sometimes offered by lenders, cover the outstanding balance of your loan or lease after a total loss. However, these can come with higher interest rates and may not fully protect you from depreciation. They may also have more stringent requirements than gap insurance.

To help you compare, we've compiled a table outlining the key differences between these coverage types:

Understanding these nuances can help you make informed decisions about your auto insurance coverage.

| Coverage Type | What It Covers | What It Doesn't Cover | Typical Cost | Who Should Consider |

|---|---|---|---|---|

| Comprehensive | Damage to your car from events like theft, vandalism, weather | The "gap" between the car's ACV and your loan balance | Varies based on vehicle and driving history | All drivers |

| Gap Insurance | The difference between the ACV and your loan balance after a total loss or theft | Damage to your car; other expenses like down payments | Typically $30-$60 per year | Drivers who owe more on their loan than their car is worth |

| New Car Replacement | A brand new car of the same make and model if your car is totaled (often within the first year of ownership) | The "gap" if the new car is more expensive; coverage after the initial period | Usually more expensive than comprehensive | Drivers of new cars concerned about rapid depreciation |

| Loan/Lease Payoff | Outstanding loan or lease balance in case of a total loss | Other expenses like down payments or negative equity; gap coverage for leased vehicles | Varies depending on the lender and loan terms | Drivers financing or leasing a new car |

The table above provides a general overview. Specific costs and coverage details can vary significantly.

Making Informed Choices: Protecting Your Investment

Choosing the right combination of coverage is crucial. Consult with your insurance provider to determine the best options for your individual needs and financial situation. By understanding the differences between gap insurance and other coverage types, you can avoid paying for unnecessary protection and ensure you're adequately covered in the event of a total loss.

Where to Buy Gap Insurance: Insider Price-Saving Strategies

Finding the right gap insurance can seem daunting. Knowing where to shop, however, can make a big difference to your wallet. The cost of identical coverage can fluctuate significantly based on the provider. Dealerships, insurance companies, and standalone providers all offer gap insurance, but their pricing models vary widely. Let's explore how to navigate these choices and find the best possible value.

Dealerships: Convenience at a Premium

Dealerships make it easy to bundle gap insurance with your new car purchase. But this ease often comes with a higher price tag. Dealer-offered gap insurance is typically the priciest option, sometimes as much as 300% higher than policies from other sources. This inflated cost often stems from added fees and commissions factored into the financing. However, there's good news! Negotiation can be your best friend.

Don't hesitate to negotiate the cost of gap insurance at the dealership. Be willing to walk away if the price isn't right. This demonstrates your seriousness as a buyer and can unlock more favorable terms. Having researched average gap insurance costs from other providers can strengthen your negotiating position.

Insurance Companies: A Smart Starting Point

Your existing auto insurance company is often a great place to begin your search for gap insurance. They frequently provide competitive rates and can easily add gap coverage to your existing policy. This streamlined process avoids the added fees and commissions often encountered at dealerships. Requesting a quote from your insurance provider is vital when comparing prices.

Don't forget to ask about potential discounts or bundling opportunities that could lower your premiums. For instance, some insurers offer discounts when you combine gap insurance with other types of coverage.

Standalone Providers: Exploring Niche Options

Standalone providers specializing in gap insurance can occasionally offer competitive pricing. While these providers may be less familiar, they can be worth considering. Thorough research on these providers is essential to ensure their financial stability and reputation. For a complete understanding of how gap insurance integrates with your overall coverage, review the basics of Understanding Insurance Policy.

Timing Your Purchase: Early Bird Advantages

The timing of your gap insurance purchase also impacts the price. Buying gap insurance soon after acquiring your new vehicle lets you capitalize on introductory offers and sidestep potential price hikes. Dealerships may initially present promotional pricing that could later disappear. Moreover, securing early gap coverage protects you against depreciation from the outset.

Canceling Existing Coverage: Path to Potential Savings

If you have pricey dealership gap insurance, switching to a more budget-friendly option from an insurance company or a standalone provider is usually feasible. Understand any cancellation fees attached to your current policy before making the change. Often, the savings from a lower premium more than offset these fees.

Buyer’s Checklist: Key Steps for the Savvy Consumer

To ensure you secure the most affordable gap insurance, consider these steps:

- Compare Quotes: Gather quotes from multiple sources—dealerships, insurance companies, and standalone providers.

- Negotiate with Dealers: Don't settle for the initial price offered at the dealership. Negotiate to get a better deal.

- Ask About Discounts: Inquire about possible discounts with your insurance company.

- Review Coverage Details: Understand the specifics of each policy before making a purchase.

- Check Cancellation Policies: Be aware of the terms and conditions for canceling your coverage.

You might also find this helpful: How to master the ultimate guide to choosing the right home insurance policy in 2025. By investing time in research and comparison, you can confidently choose the right gap insurance for your needs and budget.

Filing a Gap Claim: Critical Steps to Get Your Full Payout

Dealing with insurance claims after your car is totaled or stolen can be incredibly stressful. Adding a gap insurance claim to the mix can make it even more complicated. This section provides a clear guide to navigating the gap insurance claim process and receiving the full payout you deserve. Understanding the process, the required documentation, and potential problems can save you time, money, and a lot of frustration.

First Steps After a Loss: Immediate Actions

After your vehicle is totaled or stolen, the steps you take immediately afterward are critical for a smooth claim process. The first thing you should do is contact your primary auto insurer to report the incident. This starts your standard insurance claim. You’ll need the claim number provided by your primary insurer when you file your gap insurance claim. It's also essential to contact your gap insurance provider about the loss, ideally within 24-72 hours.

Next, gather all the necessary documents. This typically includes your auto insurance policy, your gap insurance policy, your vehicle financing agreement, and the police report (if one was filed). Having these documents organized beforehand will streamline the process. For insurance agents looking to utilize SMS marketing, this resource offers valuable insights: SMS Marketing for Insurance Agents.

Coordinating with Insurers: A Two-Part Process

Filing a gap insurance claim requires coordination with both your primary auto insurer and your gap insurance provider. Your primary insurer will determine the actual cash value (ACV) of your vehicle at the time of the loss. They will then issue a settlement based on your coverage. Your gap insurer will cover the difference between the ACV and the outstanding balance on your loan or lease. Keep in mind you may need to provide documentation to both insurers, so keep copies of everything.

This two-part process can sometimes be complex, so staying organized is key. Create a specific file or folder to keep all claim-related documents and correspondence. This will help you track deadlines and ensure you have the necessary information readily available.

Common Pitfalls to Avoid: Navigating the Challenges

Several common errors can delay or even result in a denied gap insurance claim. Missing notification deadlines, failing to submit requested documentation, and inconsistencies between the information given to both insurers can cause complications. Overlooking maintenance records, which some gap insurers require as proof of proper vehicle maintenance, is another potential issue.

For instance, some gap insurance policies exclude coverage for modifications made to the vehicle without the correct paperwork. Furthermore, failing to cooperate fully with both insurers can put your claim at risk. Understanding these potential problems will help you avoid them. If you’re looking to reduce your home insurance costs, check out this helpful resource: How to Lower Home Insurance.

Maximizing Your Settlement and Resolving Disputes: Expert Tips

To maximize your settlement, ensure your primary auto insurance policy accurately reflects your vehicle's condition and mileage. This ensures a fair ACV calculation. If you disagree with the ACV, don't hesitate to negotiate with your insurer or seek an independent appraisal. Documenting all communication with both your auto and gap insurer is crucial. This provides a record of your interactions, which can be helpful if any disputes arise.

If your gap insurance claim is denied, don't give up. Carefully review your policy to understand the reasons for the denial. Contact your gap insurer to discuss the denial and submit any additional information supporting your claim. If necessary, consider seeking legal advice. Being proactive and persistent can significantly increase your chances of a positive outcome. A recent court case highlighted the importance of understanding the rules and regulations surrounding add-on products like gap insurance. While this particular case involved dealer practices, it emphasizes the need for consumers to be well-informed and understand their rights. This means thoroughly reviewing all documents and asking questions if anything is unclear.

Comments are closed.