Understanding Insurance Riders and Why They Matter

Want to customize your insurance coverage and get more bang for your buck? This listicle explores six essential types of insurance riders. Discover how these optional add-ons can enhance your base policy, providing crucial benefits like waiving premiums during disability, boosting payouts for accidental death, or covering long-term care expenses. Understanding the different types of insurance riders empowers you to create a policy that truly meets your needs, offering greater financial security and peace of mind. Learn about the waiver of premium rider, accidental death benefit rider, guaranteed insurability rider, long-term care rider, critical illness rider, and return of premium rider.

1. Waiver of Premium Rider

A Waiver of Premium rider is a valuable addition to various types of insurance riders, offering crucial financial protection during challenging times. This rider acts as a safety net, eliminating the obligation to pay premiums if the policyholder becomes disabled due to a serious illness or injury and is unable to work. This ensures the insurance coverage remains active, safeguarding the policyholder's financial interests even when they face income disruption. This can be especially crucial for life insurance policies, preventing a lapse in coverage during a period when the death benefit might be most needed.

This type of insurance rider typically includes features like automatic premium payments during the disability period, eliminating the financial burden on the policyholder. There's usually a waiting period (typically 3-6 months) after the onset of the disability before the rider's benefits kick in. The rider generally remains in effect until the policyholder reaches a specified age, often 60 or 65. It's important to note that most riders require periodic proof of continued disability to maintain the benefit. Furthermore, the rider will include specific definitions of "disability" that must be met to qualify for premium waivers.

Pros:

- Maintains insurance coverage: Ensures your policy stays active even when you can't afford premiums.

- Prevents policy lapse: Safeguards against losing coverage during financial hardship.

- Affordable protection: Offers substantial benefits relative to its cost.

- Peace of mind: Provides assurance that your coverage will endure despite unforeseen circumstances.

- Essential for primary earners: Offers crucial protection for families dependent on a single income.

Cons:

- Increased base premium: Adding this rider slightly increases the overall policy cost.

- Strict disability definitions: Qualifying for the waiver might require meeting specific criteria.

- Waiting period: The period before benefits begin can create a temporary financial strain.

- Not all disabilities covered: Some conditions might not be included in the rider's definition of disability.

- Age limitations: Coverage under the rider typically ends at a certain age.

Examples:

- Imagine a 45-year-old primary income earner suffering a severe back injury that prevents them from working for two years. A waiver of premium rider would ensure their life insurance policy remains in force without requiring premium payments, protecting their family's financial future.

- Northwestern Mutual, a well-known provider of this type of rider, covers total disability and continues the policy without further premium payments after a 6-month waiting period.

Tips for Utilizing a Waiver of Premium Rider:

- Early inclusion: Add this rider when you're younger and premiums are lower.

- Careful review: Thoroughly understand the definition of "disability" within the rider.

- Comparison shopping: Compare waiting periods and coverage across different insurance providers.

- Risk assessment: Consider your occupation and potential disability risks.

- Priority for primary earners: This rider is especially vital if you're the primary source of income for your family.

When and Why to Use a Waiver of Premium Rider:

This rider is highly recommended for individuals who:

- Are the primary income earners in their families.

- Work in high-risk occupations.

- Want to ensure their insurance coverage remains active regardless of unforeseen circumstances.

- Seek peace of mind regarding their financial protection.

This type of rider is essential for many because it bridges the gap between maintaining crucial insurance coverage and the inability to pay premiums due to disability. It’s a small investment that can yield significant returns in terms of financial security and peace of mind. Companies like Prudential Insurance Company, MetLife, Northwestern Mutual, and New York Life Insurance Company have popularized this vital rider, recognizing its importance in comprehensive insurance planning. Learn more about Waiver of Premium Rider This resource might offer additional insights, although it's focused on renters insurance, which demonstrates how the concept of adding riders for enhanced protection applies across various insurance types.

2. Accidental Death Benefit Rider

The Accidental Death Benefit (ADB) rider is a valuable addition to a life insurance policy that provides a supplemental payout to beneficiaries if the insured's death results from an accident. This rider enhances the base policy's coverage by offering a significantly larger death benefit—typically double or even triple the original face value—specifically in cases of accidental death. This extra layer of financial protection helps beneficiaries cope with the sudden loss of income and any unexpected expenses that may arise from such an event. The ADB rider is one type of insurance rider that addresses a specific need – providing a financial safety net for families facing the devastating consequences of an accidental death.

ADB riders generally define "accidents" as sudden, unexpected, and external events. They often include clauses specifying that death must occur within a certain timeframe following the accident, usually between 90 and 180 days. Importantly, ADB riders typically exclude coverage for deaths resulting from high-risk activities (like skydiving or base jumping), illegal activities, suicide, and certain pre-existing medical conditions. Furthermore, this type of rider is usually available only up to a certain age, often 65 or 70.

Features of an ADB Rider:

- Additional Death Benefit: Pays a lump sum in addition to the base policy's death benefit, often doubling it.

- Specific Definition of Accident: Covers deaths caused by sudden, unexpected, and external events.

- Time Limitations: Death must occur within a specific period after the accident.

- Exclusions: Doesn't cover deaths due to high-risk activities, illegal acts, or certain medical conditions.

- Age Limit: Coverage typically terminates at a specified age.

Pros:

- Increased Coverage at Low Cost: Offers substantial additional coverage for a relatively small premium increase.

- Addresses Specific Financial Needs: Provides a financial cushion for families dealing with the unexpected loss of income due to an accidental death.

- Simplicity: Easy to understand and add to an existing policy.

- Value for High-Risk Occupations: Particularly beneficial for individuals working in professions with higher accident risks.

- Peace of Mind: Offers reassurance to families concerned about the financial implications of an accidental death.

Cons:

- Limited Coverage: Does not cover deaths from natural causes or illness.

- Exclusions Apply: Contains numerous exclusions that can limit the scope of coverage.

- Potential Overlap: May duplicate existing accidental death and dismemberment (AD&D) coverage from employers or other policies.

- Age Restrictions: Terminates at a specified age, even though the risk of accidents can still exist.

- False Sense of Security: May create a false impression of comprehensive coverage, leading to underinsurance in other areas.

Examples:

- A 35-year-old construction worker with a $500,000 life insurance policy and an ADB rider could provide their beneficiaries with $1,000,000 in the event of a fatal work-related accident.

- Companies like State Farm, Farmers Insurance, and others offer various ADB riders with different coverage amounts and options.

Tips for Consumers:

- Assess Your Risk: Consider your occupation, lifestyle, and hobbies when evaluating the need for an ADB rider.

- Review Existing Coverage: Determine if you already have sufficient accidental death coverage through your employer or other policies.

- Scrutinize Exclusions: Carefully read the policy's exclusions to fully understand the limitations of coverage.

- Comprehensive Planning: Don't rely solely on an ADB rider for complete financial protection. Ensure you have adequate life insurance coverage and other necessary financial safeguards.

- Compare Costs and Benefits: Compare the cost of ADB riders from different insurers to find the best value.

The ADB rider deserves its place in a discussion of types of insurance riders due to its targeted approach to a specific risk – accidental death. While a standard life insurance policy covers death from any cause, the ADB rider acknowledges the heightened financial vulnerability associated with accidental deaths and provides an extra layer of financial support when it's needed most. This focus makes it a valuable tool for individuals seeking to strengthen their family's financial security in the face of unforeseen tragedy.

3. Guaranteed Insurability Rider

The Guaranteed Insurability Rider (GIR) is a valuable addition to a life insurance policy, offering the flexibility to increase coverage without further medical underwriting. It allows policyholders to purchase additional insurance at specified future dates, regardless of changes in their health. This rider essentially "locks in" your insurability at a younger, healthier age, protecting you against the possibility of becoming uninsurable due to illness or injury later in life. This feature provides peace of mind and ensures your coverage can adapt to evolving financial needs, such as marriage, the birth of a child, or the purchase of a home.

The GIR operates through predetermined "option dates," typically tied to significant life events or specific age milestones. When an option date arrives, the policyholder can choose to purchase additional coverage up to a predetermined limit without undergoing medical exams or answering health questions. The premium for this additional coverage is based on the policyholder's attained age at the time of purchase, but crucially, it's calculated using standard health rates. This means even if your health has declined since the initial policy purchase, you won't face higher premiums due to pre-existing conditions. This rider is usually available until a specific age, commonly between 40 and 50.

Features of a Guaranteed Insurability Rider:

- Option Dates: Specific times when you can purchase additional coverage.

- No Medical Underwriting: No medical exams or health questionnaires required.

- Predetermined Limits: Caps on the amount of additional coverage you can purchase at each option date.

- Age Limit: Typically available until a certain age (e.g., 40 or 50).

- Standard Health Rates: Premiums for additional coverage are based on attained age but at standard health rates.

Pros:

- Protection Against Future Uninsurability: Secure coverage even if health deteriorates.

- Adaptable Coverage: Increase coverage as financial responsibilities grow.

- Peace of Mind: Certainty in long-term insurance planning.

- Potential Cost Savings: Avoid higher premiums due to future health changes.

- Ideal for Young Adults: Particularly beneficial for those anticipating income growth and major life events.

Cons:

- Increased Base Premium: Adding a GIR increases the cost of your initial policy.

- Time Limitations: Option dates are "use it or lose it" opportunities.

- Age-Based Premiums: Additional coverage premiums increase with age.

- Purchase Limits: Caps on the amount of additional insurance purchasable.

- May Be Unnecessary: Potentially redundant if health remains good and insurance remains readily accessible.

Examples:

- A 25-year-old purchasing life insurance with a GIR can increase coverage at key milestones like marriage or the birth of a child, even if diagnosed with a chronic illness at 35.

- Companies like MassMutual and Northwestern Mutual offer variations of this rider, allowing policyholders to increase coverage without medical exams at specific intervals.

Tips for Utilizing a Guaranteed Insurability Rider:

- Consider Family History: If you have a family history of health issues, a GIR can be particularly beneficial.

- Project Future Needs: Carefully calculate potential future insurance needs when determining option amounts.

- Track Option Dates: Mark option dates on your calendar to avoid missing opportunities.

- Evaluate Your Risk Profile: Assess whether the rider cost is justified by your individual health risks.

- Compare Insurers: Compare option dates, purchase limits, and rider costs across different insurance companies.

The Guaranteed Insurability Rider deserves a place on this list because it provides crucial flexibility and protection against unforeseen health changes. It's a powerful tool for individuals, families, and business owners alike who want to ensure their life insurance coverage remains adequate as their needs evolve. Learn more about Guaranteed Insurability Rider to better understand its implications and benefits. This is particularly relevant for young singles, families planning for the future, and business owners seeking long-term financial security.

4. Long-Term Care Rider

A Long-Term Care (LTC) rider is a valuable addition to a life insurance policy, offering a way to address the potential financial burdens of extended care needs. It essentially transforms a standard life insurance policy into a hybrid, providing both a death benefit and living benefits that can be accessed if you require long-term care. This makes it a significant option among the different types of insurance riders available.

This rider allows you to accelerate a portion of your death benefit while you're still alive to pay for qualifying long-term care expenses. These expenses can include nursing home care, assisted living facilities, or even in-home care. Instead of purchasing a separate, standalone long-term care insurance policy, an LTC rider leverages your existing life insurance, providing a convenient and often more affordable solution.

How it Works:

The LTC rider typically becomes activated when you are unable to perform two or more Activities of Daily Living (ADLs), such as bathing, dressing, eating, or using the toilet. Cognitive impairment, such as Alzheimer's disease, can also trigger the benefits. Once activated, you can access a pre-determined portion of your death benefit each month to pay for your care.

Features and Benefits:

- Accelerated Death Benefit: Access a portion of your death benefit for qualified long-term care expenses.

- Triggering Events: Typically requires the inability to perform 2+ ADLs or cognitive impairment for activation.

- Benefit Limits: Usually includes a maximum monthly benefit and a total lifetime benefit limit.

- Impact on Death Benefit: The death benefit is reduced as LTC benefits are paid out.

- Waiting Period: May include an elimination or waiting period before benefits begin.

- Affordability: Often more affordable than standalone LTC insurance.

Pros:

- Dual Protection: Offers coverage for both death and long-term care needs.

- Cost-Effective: Generally less expensive than separate long-term care insurance.

- Guaranteed Use of Benefits: Ensures the benefits will be utilized, either for care or as a death benefit.

- Simplified Underwriting: Typically has less stringent underwriting requirements than standalone LTC policies.

- Asset Protection: Helps protect your assets from being depleted by long-term care costs.

- Stable Premiums: More stable premiums compared to traditional LTC insurance.

Cons:

- Reduced Death Benefit: Utilizing LTC benefits reduces the final death benefit paid to beneficiaries.

- Coverage Limitations: May provide less comprehensive LTC coverage than standalone policies.

- Benefit Caps: Usually has daily or monthly benefit caps.

- Increased Premium: Can increase the premium of your base life insurance policy.

- Service Restrictions: May have limitations on covered facilities or services.

- Inflation Risk: Benefits may not keep pace with rising healthcare costs.

Examples:

- John Hancock offers LTC riders allowing policyholders to access up to 4% of their death benefit monthly for qualified long-term care expenses.

- Lincoln Financial's MoneyGuard® combines life insurance with long-term care benefits usable for various care settings.

- A 60-year-old with a $500,000 policy and an LTC rider could potentially access $10,000 monthly for care, lasting up to 50 months.

Tips for Choosing an LTC Rider:

- Compare Costs: Compare the rider's cost to the cost of a standalone LTC insurance policy.

- Understand Triggers: Know precisely what conditions trigger the benefits (which ADLs or cognitive impairments).

- Inflation Protection: Check if the policy offers inflation protection for LTC benefits.

- Benefit Adequacy: Review the maximum monthly benefit to ensure it's sufficient for care costs in your area.

- Family History: Consider your family history of longevity and long-term care needs.

- Tax Implications: Consult a financial advisor to understand the tax implications of the rider.

Popularized By: Lincoln Financial Group's MoneyGuard®, John Hancock, Nationwide, Pacific Life, Prudential

Why This Rider Deserves Its Place in the List:

The Long-Term Care rider is a crucial consideration when evaluating types of insurance riders. It offers a practical and often cost-effective way to address the growing concern of long-term care expenses, which can quickly deplete savings. By combining these benefits with a life insurance policy, individuals can achieve a comprehensive approach to financial planning that protects both their future and the well-being of their loved ones. Whether you're a family seeking long-term financial security, a single individual planning for the future, or a business owner looking for comprehensive coverage, understanding the benefits and limitations of an LTC rider is essential.

5. Critical Illness Rider

A Critical Illness rider is a valuable addition to a life insurance policy that provides a lump-sum cash payment upon the diagnosis of a covered critical illness. This type of insurance rider deserves its place on this list because it offers crucial financial support during a challenging time, bridging the gap between existing health insurance and the often overwhelming costs associated with serious illnesses. It's a powerful tool for families, couples, singles, and even business owners seeking to safeguard their financial stability in the face of unexpected health crises.

How it Works:

The Critical Illness rider functions as a supplement to your main life insurance policy. Upon diagnosis of a specific covered illness, such as cancer, heart attack, stroke, or organ failure, the rider pays out a predetermined lump sum benefit. Importantly, this payment is made regardless of the actual medical expenses incurred. This means you have the flexibility to use the funds for any purpose – from covering medical bills and deductibles to paying your mortgage, daily living expenses, or even exploring experimental treatments not covered by traditional insurance.

Features and Benefits:

- Lump-Sum Payment: Provides immediate financial support upon diagnosis.

- Specific Illness Coverage: Typically covers major illnesses like cancer, heart attack, stroke, and organ failure.

- Payment Independent of Costs: The benefit is paid regardless of actual medical expenses.

- Survival Period: Usually requires a survival period (e.g., 30 days) after diagnosis.

- Benefit Structure: Can be an accelerated benefit (reducing the death benefit) or an additional benefit.

- Age Limit: Often has a maximum age limit for coverage (e.g., 65-75).

Pros:

- Immediate financial support upon diagnosis

- Benefit can be used for any purpose

- Bridges the gap between health insurance and actual costs

- Offers financial flexibility during recovery

- Relatively affordable compared to standalone critical illness policies

- No receipts or proof of expenses required

Cons:

- Increases the base insurance premium

- Limited to specifically defined conditions

- May have waiting periods before coverage begins

- Often excludes pre-existing conditions

- May reduce the death benefit if structured as an acceleration

- Can have complex qualification criteria

Examples:

- A 45-year-old policyholder diagnosed with Stage 2 cancer receives a $50,000 lump sum to cover deductibles, experimental treatments, and lost income during treatment.

- AIG's Critical Illness rider covers up to 16 different conditions and provides payments up to $2 million for qualifying diagnoses.

- Mutual of Omaha's Critical Advantage rider provides payouts for conditions in four categories: cancer, heart/stroke, organ, and childhood.

Tips for Choosing a Critical Illness Rider:

- Review the specific definition of covered illnesses in the rider.

- Compare with standalone critical illness policies for comprehensiveness.

- Consider your family medical history when evaluating the value.

- Check if the benefit amount is adequate for potential income loss and expenses.

- Understand whether the rider accelerates or adds to the death benefit.

- Review any exclusions, particularly for pre-existing conditions.

Popularized By: AIG, Mutual of Omaha, Aflac, American Fidelity, Colonial Life

When and Why to Use a Critical Illness Rider:

Consider a Critical Illness rider if you are concerned about the financial implications of a serious illness and want to ensure you have access to funds to cover expenses beyond what your health insurance might provide. It's particularly valuable for those with families, mortgages, or other significant financial obligations. Learn more about Critical Illness Rider (Note: While this link is provided as requested, it doesn't seem to relate to Critical Illness Riders and should be updated by the requester with a relevant link). This type of insurance rider is an important consideration among the various types of insurance riders available.

6. Return of Premium Rider

The Return of Premium (ROP) rider is a valuable addition to certain insurance policies, offering a unique blend of protection and savings. It allows policyholders to receive a full or partial refund of their premiums paid if they outlive the policy term without filing a claim. This feature transforms a traditional insurance policy, which typically only pays out upon a covered event, into a combined insurance and savings instrument. Essentially, if the insured person doesn't need to use the policy's benefits, they get their money back. This rider is especially attractive for those who view insurance as an expense and appreciate the potential for a return on investment.

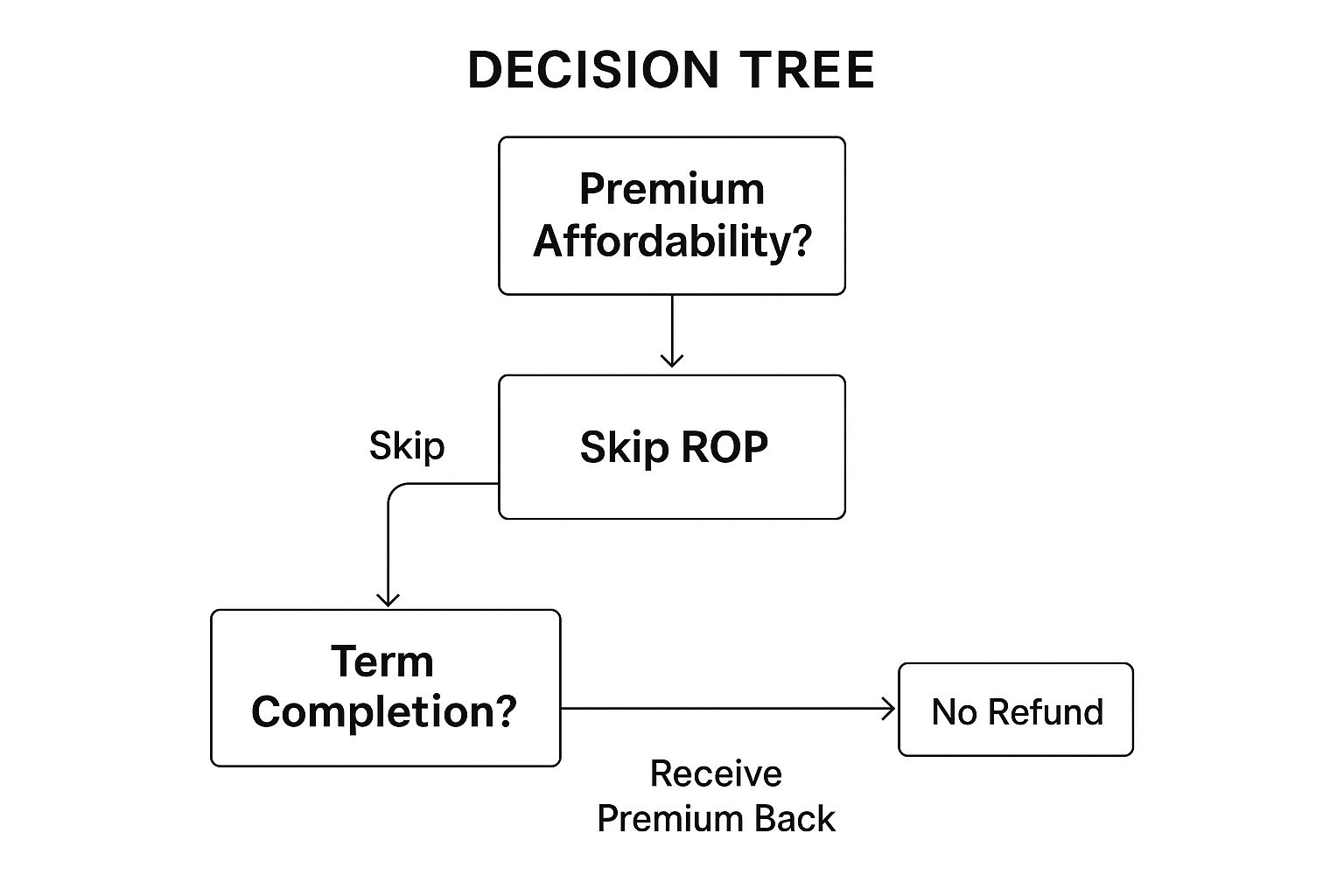

The infographic above presents a simplified decision tree to help determine if a Return of Premium rider is right for you. It starts by asking if you are comfortable with higher premiums. If yes, it then prompts you to consider if you prioritize getting your premiums back over potential investment growth. If the answer is still yes, then an ROP rider might be a good fit. However, if you prefer lower premiums or maximizing investment returns, then an ROP rider is likely not the best option.

This rider deserves its place on the list of insurance riders because it addresses a key concern for many individuals: the perceived "loss" of premiums if a claim is never filed. It provides a tangible return on investment, making insurance more appealing to those hesitant about the traditional model. ROP riders are typically available with term life insurance and some disability insurance policies. Key features include the return of either 100% of base premiums or a graduated percentage based on the policy's duration, usually requiring the completion of the full policy term. It's crucial to understand that some ROP riders only return the base premium paid, excluding the cost of the rider itself or any other add-ons. Some policies, however, may offer partial returns if the policy is surrendered early.

Pros:

- Creates a 'money-back' feature, making insurance feel less like an expense.

- Provides a potential return of investment if the insurance isn't needed.

- Can function as a forced savings mechanism.

- Creates higher perceived value for risk-averse consumers.

- Can help with retirement planning if timed appropriately.

- Makes income protection more attractive to younger policyholders.

Cons:

- Significantly increases premium costs (often 2-3 times higher).

- Returns money without interest or investment growth.

- Often requires completion of the full policy term to receive full benefits.

- May have reduced cash value if surrendered early.

- Opportunity cost of higher premiums versus investing the difference.

- May trigger taxable events in some situations.

Examples:

- A 30-year-old purchases a 30-year term life policy with an ROP rider for $150/month instead of $60/month without the rider, receiving $54,000 back at age 60 if they survive the term.

- Illinois Mutual's DI105 disability insurance with ROP rider returns 80% of premiums if no claims are made during the policy period.

- Assurity's LifeScape ROP Term Life returns 100% of premiums at the end of 20 or 30-year terms.

Tips:

- Calculate the opportunity cost by comparing premium differences invested at a reasonable return rate.

- Consider your life stage and whether the premium return will align with your financial needs.

- Understand exactly which premiums are returned (base premiums only or including rider costs).

- Review tax implications of premium returns with a tax professional.

- Evaluate the company's financial strength since benefits are paid decades in the future.

- Compare partial return schedules if you might need to cancel before the term ends.

Popularized By: Assurity Life Insurance Company, American National, Illinois Mutual, Pacific Life, Prudential

When and Why to Use This Approach:

The Return of Premium rider is ideal for individuals who:

- Are risk-averse and value the guaranteed return of premiums.

- Seek a forced savings mechanism combined with insurance coverage.

- Are comfortable paying higher premiums for the peace of mind of a potential return.

- Prioritize the return of premiums over potential investment growth.

This rider is less suitable for individuals who:

- Prioritize maximizing investment returns.

- Are comfortable with the traditional insurance model.

- Are price-sensitive and seek the lowest possible premiums.

By carefully weighing the pros and cons and considering your individual financial circumstances, you can determine if the Return of Premium rider is the right choice for your insurance needs.

6 Insurance Rider Types Comparison

| Rider Type | Implementation Complexity 🔄 | Resource Requirements 💡 | Expected Outcomes 📊 | Ideal Use Cases 💡 | Key Advantages ⭐ |

|---|---|---|---|---|---|

| Waiver of Premium Rider | Medium 🔄🔄 | Moderate | Maintains coverage during disability | Primary income earners facing disability risk | Keeps policy active during financial hardship |

| Accidental Death Benefit | Low 🔄 | Low | Additional payout on accidental death | High-risk occupations and those needing extra accident cover | Affordable extra death benefit with simple terms |

| Guaranteed Insurability | Medium 🔄🔄 | Moderate | Ability to increase coverage without new underwriting | Young policyholders expecting health changes | Locks insurability; coverage grows with life stages |

| Long-Term Care Rider | High 🔄🔄🔄 | High | Access to death benefit for long-term care expenses | Those concerned about long-term care costs and aging | Dual protection for death and care needs; more affordable than standalone LTC insurance |

| Critical Illness Rider | Medium 🔄🔄 | Moderate | Lump sum on diagnosis of serious illnesses | Individuals with family history of critical illnesses | Immediate financial support for major health events |

| Return of Premium Rider | Medium 🔄🔄 | Moderate to High | Refund of premiums if no claims made | Risk-averse individuals wanting forced savings | Returns premium payments, reducing net insurance cost |

Choosing the Right Insurance Riders: Your Next Steps

Understanding the various types of insurance riders is crucial for tailoring your insurance policies to your specific needs. From the waiver of premium rider, offering financial relief during disability, to the critical illness rider providing a lump-sum payment after a serious diagnosis, each rider plays a unique role in enhancing your coverage. We've explored riders like accidental death benefit, guaranteed insurability, long-term care, and return of premium, each designed to address specific circumstances and bolster your financial security.

The most important takeaway is that insurance isn't one-size-fits-all. By carefully selecting the right combination of types of insurance riders, you can create a comprehensive safety net that aligns with your life stage, financial goals, and potential risks. To further enhance your understanding and help you choose the right riders for your specific needs, you can explore this comprehensive guide on the different types of insurance riders from America First Financial. Whether you're a student seeking affordable coverage, a family prioritizing long-term security, a business owner protecting your assets, or a frequent traveler requiring international coverage, understanding these options empowers you to make informed decisions.

Your next step is to review your existing policies and identify any potential gaps in coverage. Consider your individual circumstances, future plans, and potential risks. Don't hesitate to reach out to your insurance provider to discuss the available types of insurance riders and how they can be incorporated into your policy. Mastering these concepts allows you to not just have insurance, but to have the right insurance, offering you and your loved ones true peace of mind. Take control of your financial future today – a secure tomorrow starts with the choices you make now.

Comments are closed.