Navigating Today's Insurance Landscape

Car insurance can often feel like a significant expense. Understanding the current auto insurance market is the first step towards potentially lowering your premiums. This begins with understanding how insurance companies determine their pricing. One key factor is location; regional differences can heavily influence your rates. This article will equip you with the knowledge to make informed decisions about reducing your car insurance costs.

Understanding Rate Fluctuations

Managing insurance costs effectively involves understanding how and why rates fluctuate. This knowledge can help you anticipate potential increases and identify the optimal times to compare policies from different providers. Understanding how insurers calculate your premium, considering factors like your driving record and vehicle type, empowers you to manage the aspects within your control. Staying informed about market trends can also reveal opportunities for savings. This means keeping up-to-date with insurance industry news and changes in pricing strategies.

One factor impacting premiums is the overall trend of rate increases. Auto insurance rates have been rising in recent years. For example, 2024 saw a 16.5% average rate increase, which followed a 12% increase in 2023. A slowdown is anticipated for 2025, with a projected average increase of 7.5%. However, premiums are still expected to reach a record high of $2,101 per year in the United States. You can learn more about these trends. These fluctuations, along with regional variations, are essential considerations when seeking to lower your premiums. Drivers in states like New Jersey, Washington, and California, for instance, are experiencing steeper increases and could potentially benefit from comparing rates across different insurance companies.

Regional Differences and Insurance Costs

Understanding regional pricing patterns is crucial for finding affordable car insurance coverage. Rates can differ significantly between states due to several factors, including population density, weather conditions, and state-specific regulations. Where you live plays a substantial role in determining your premium. By recognizing these regional differences, you can take a proactive approach to finding the best possible rates. This might involve adjusting your coverage levels or researching insurers known for offering competitive pricing in your specific location.

You might also be interested in learning How to identify the best home insurance policy for 2025. Ultimately, navigating the current insurance market requires a proactive and informed approach. By understanding the factors that influence rate changes, you can gain more control over your insurance costs and secure the most suitable coverage for your needs and budget.

Global Trends That Unlock Hidden Savings

The global insurance market is in constant flux, creating a dynamic environment ripe with opportunities for drivers to save on car insurance premiums. By understanding these international trends, you can discover new ways to reduce your insurance costs. For instance, global competition among insurance providers can significantly impact pricing strategies, giving consumers more leverage.

How International Competition Impacts Your Premiums

Competition in the global insurance market indirectly affects your local insurance rates. Insurers regularly adjust their pricing based on market conditions, including competitor offerings in different regions. This allows you to compare rates and find insurers with more competitive pricing models, ultimately lowering your premiums. The development of new technologies also plays a role, changing how premiums are calculated across different markets.

This leads to more accurate risk assessments and potentially more personalized pricing.

The size of the global motor vehicle insurance market is another important factor. Projected to reach $940.79 billion by 2025, this market demonstrates the substantial global demand for car insurance. More detailed information on this market can be found here. Driven by rising vehicle ownership and stricter insurance regulations, this growth fosters a competitive environment where insurers must constantly strive to attract and retain customers.

The Role of Emerging Technologies and Regulation

Emerging technologies, such as telematics and AI-powered risk assessment, are changing the way insurance premiums are determined. The adoption of these technologies is a global phenomenon, not limited to specific countries. As these technologies improve risk prediction, they can lead to more accurate and potentially lower premiums for safe drivers.

For example, usage-based insurance programs, which monitor driving habits, can offer substantial discounts for safe driving.

Regulatory changes in other countries can also influence domestic pricing strategies. Insurers often monitor international regulatory developments to anticipate future changes and adapt their pricing accordingly. Staying informed about international insurance regulations can provide insights into potential changes in your local market.

This awareness allows you to anticipate shifts in your area, giving you a potential advantage when comparing insurance policies. By understanding these global influences, you can identify ways to lower your car insurance premiums and secure the best possible rates.

Building Your Perfect Driver Profile

Your car insurance premium reflects how much of a risk insurers perceive you to be. So, how can you improve that perception and potentially lower your car insurance costs? Insurers evaluate drivers based on several key factors. Understanding these factors helps you take control and implement strategies for savings.

Driving Record and Insurance Premiums

Your driving record is a major factor in determining your insurance premium. A clean driving record, free of accidents and traffic violations, demonstrates responsible driving habits. This can lead to lower premiums because insurers view you as a lower risk. Conversely, accidents and tickets can significantly increase your rates.

Maintaining a positive driving history is one of the most effective ways to keep your insurance costs low. It shows insurers you are a responsible driver, reducing your perceived risk.

- Maintain a clean driving record: Avoid speeding tickets and accidents.

- Consider defensive driving courses: Some insurers offer discounts for completing approved defensive driving courses.

- Address any inaccuracies: Review your driving record for errors and dispute them with the relevant authorities if necessary.

Credit Score's Impact on Car Insurance

In many states, your credit score plays a role in determining your car insurance rates. Insurers use credit-based insurance scores to assess risk. A higher credit score generally translates to lower insurance premiums. Studies have shown a correlation between credit scores and the likelihood of filing a claim.

Improving your credit profile not only benefits your overall financial health but can also positively impact your insurance rates.

- Improve your credit score: Pay bills on time and manage debt effectively. You can find resources and tools online to help you improve your credit score.

- Check your credit report regularly: Identify and correct any errors that could negatively affect your score. AnnualCreditReport.com allows you to access your credit reports from the three major credit bureaus.

- Understand your state's regulations: Some states restrict the use of credit scores in setting insurance premiums. Research your state's specific insurance laws.

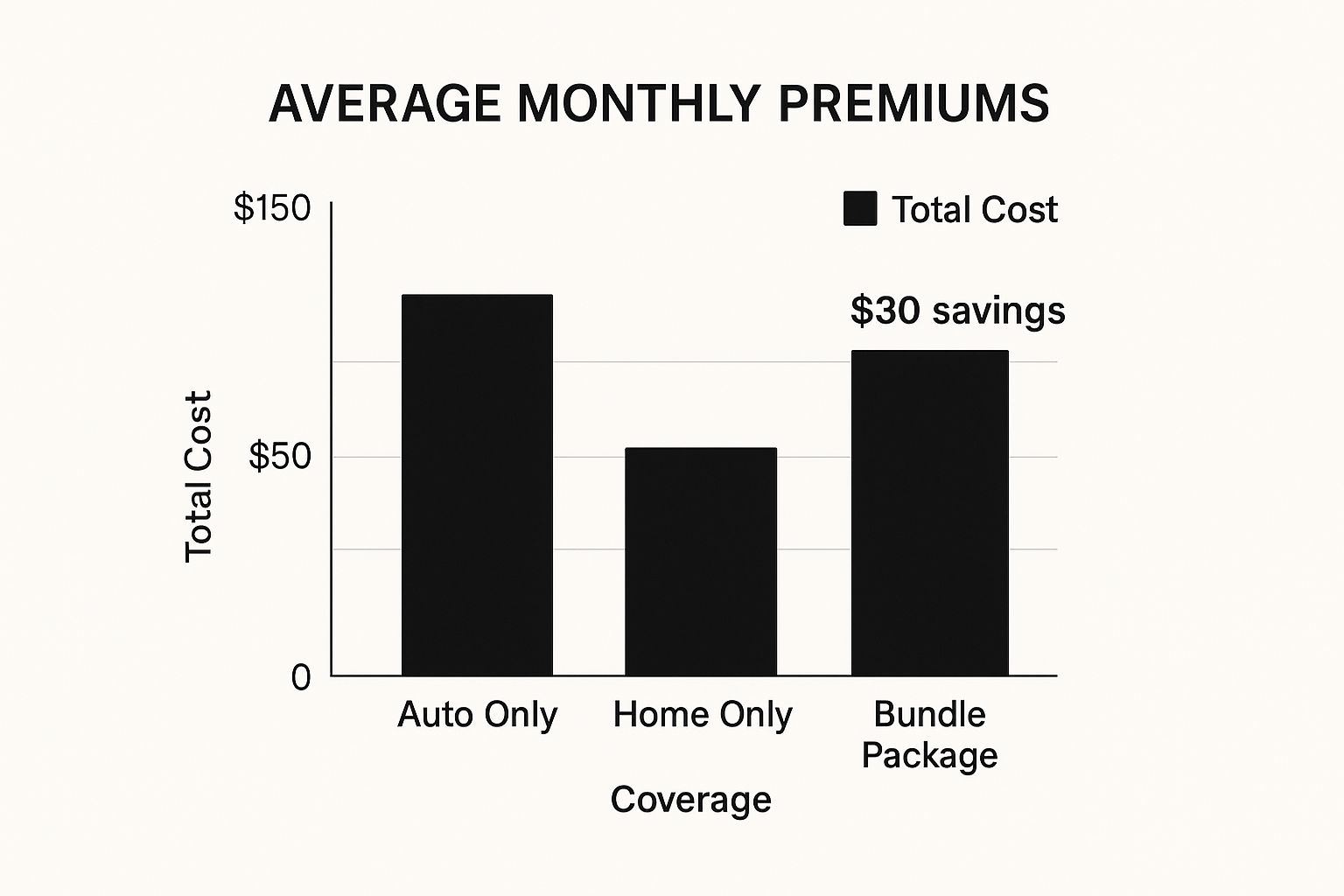

This infographic visualizes average monthly premiums for Auto Only, Home Only, and a Bundle Package. Bundling your auto and home insurance can often lead to significant cost savings compared to purchasing these policies separately.

Vehicle Characteristics and Insurance Costs

The type of vehicle you drive can also influence your insurance premium. Factors like the vehicle's safety features, age, and repair costs are taken into consideration. Vehicles equipped with advanced safety features often qualify for discounts.

By strategically choosing your vehicle and focusing on models with robust safety features, you can further manage your insurance premiums. This combines cost-saving measures with increased safety on the road.

To illustrate the impact of vehicle characteristics on insurance premiums, let's look at the following table:

Insurance Premium Impact by Vehicle Characteristic

This table compares how different vehicle characteristics affect insurance premium costs across typical insurance providers.

| Vehicle Characteristic | Average Premium Impact | Potential Savings |

|---|---|---|

| Safety Features (Anti-theft, airbags, etc.) | -5% to -25% | Shop around for insurers that offer these discounts |

| Newer Vehicle (Less than 5 years old) | +10% to +40% | Consider a slightly older model |

| High-Performance Vehicle | +20% to +50% | Opt for a standard model |

| Vehicle's Repair Costs | Varies significantly | Research repair costs before purchasing a vehicle |

As you can see, safety features can significantly reduce premiums. Conversely, newer and high-performance vehicles tend to come with higher premiums. By being mindful of these factors when choosing a car, you can significantly impact your insurance costs.

Coverage Customization That Slashes Costs

Many drivers pay for car insurance coverage they simply don't need. This section explores how customizing your coverage can lower your car insurance premiums while maintaining essential protection. It's all about striking the right balance.

Understanding Your Coverage Options

A crucial first step in lowering your car insurance costs is to understand your coverage options. Insurance policies often include various types of coverage, some of which may be unnecessary given your specific situation. Carefully review your policy details to identify any areas of over-insurance.

For example, if you own an older car with a low market value, maintaining both comprehensive and collision coverage might not be the most cost-effective strategy. Look closely at your policy's language for clauses that indicate overlapping or unnecessary coverage. This careful review will help you tailor your policy to your actual needs.

Deductibles: Finding the Sweet Spot

Your deductible, the amount you pay out-of-pocket before your insurance coverage begins, significantly impacts your premium. A higher deductible generally translates to a lower premium. However, you must be able to comfortably afford your deductible in the event of a claim.

A higher deductible is essentially self-insuring for a greater portion of the risk. This reduces the insurance company's liability and, in turn, lowers your premium. Finding the right deductible involves balancing your financial capacity with your desired level of risk.

Customizing Coverage Limits

Coverage limits are the maximum amount your insurance will pay for a covered claim. Similar to deductibles, adjusting your coverage limits can significantly affect your premiums. Adequate coverage is vital, but excessively high limits can unnecessarily inflate your costs.

Consider your risk exposure. Set limits that realistically reflect your potential needs. Someone driving primarily in low-traffic areas might require lower bodily injury liability limits compared to someone navigating congested city streets. Sometimes, improving your overall financial profile can also lead to savings. For more insights, check out How to Reduce Tax Liability.

Strategic Timing and Policy Adjustments

The timing of your policy updates can also affect your costs. Take a look at our guide on How to master car insurance cost savings. Regularly review your policy, especially after significant life events like buying a new car or moving. These changes provide opportunities to adjust coverage and potentially save. It's also a good idea to compare quotes from different insurers periodically to ensure you're getting the best rate.

To help you make informed decisions about your car insurance coverage, we've compiled the following cost-benefit analysis. It breaks down the costs and benefits of different coverage options.

| Coverage Type | Monthly Cost Impact | Protection Value | Recommended For |

|---|---|---|---|

| Liability Only | Low | Covers damage/injury to others | Budget-conscious drivers with older vehicles |

| Liability + Collision | Medium | Adds coverage for your vehicle damage (regardless of fault) | Drivers wanting more protection for their own vehicle |

| Comprehensive | High | Covers your vehicle for non-collision incidents (theft, weather) | Drivers with newer, more valuable cars |

| Uninsured/Underinsured Motorist | Medium | Protects you if hit by a driver without enough insurance | All drivers, especially in areas with high uninsured rates |

By understanding the relationships between coverage types, deductibles, limits, and timing, you can customize your policy for maximum savings without compromising necessary protection.

Unlocking Discounts Most Drivers Miss Entirely

Finding the lowest car insurance premiums often depends on uncovering hidden discounts. Many drivers are unaware of the breadth of discounts available beyond the standard offerings. This article will explore these often-overlooked opportunities that can substantially lower your car insurance costs. For more tips on saving, check out this helpful resource: How to master car insurance savings.

Exploring the Discount Ecosystem

Car insurance discounts extend far beyond the typical good driver and multi-policy discounts. Many insurers offer discounts based on factors like professional affiliations, educational achievements, and memberships in specific organizations.

These discounts can be significant, yet often go unclaimed. For example, some insurers offer reduced rates to members of professional organizations like the American Bar Association, alumni associations, or even certain employee groups.

This underscores the importance of actively asking about all possible discounts. Don't hesitate to contact your insurance representative about any affiliations or memberships that might qualify you for savings.

Documenting and Proving Eligibility

To secure these discounts, proper documentation is essential. Having the necessary paperwork on hand simplifies the application process. This might include membership cards, professional certifications, or academic transcripts.

For example, if you're eligible for a good student discount, ensure you have your current grades readily available. This preparation can save you considerable time and effort.

Clear communication is also vital. When discussing discounts with your insurer, clearly explain your eligibility for each one. This precision helps ensure all applicable discounts are applied accurately. It can also reveal stacking opportunities, where multiple discounts combine for even greater savings.

Loyalty Programs and Long-Term Savings

Many insurance companies offer loyalty programs rewarding long-term customers with premium discounts and other benefits. However, loyalty doesn't always guarantee the absolute lowest rate.

It's crucial to periodically compare rates from other insurers to ensure your loyalty program truly maximizes your savings. Sometimes, switching insurers might offer greater long-term cost benefits, even if it means forgoing loyalty rewards.

Market trends can also significantly impact premiums. For instance, comprehensive car insurance premiums in the UK decreased by 17% between March 2024 and February 2025, resulting in an average annual premium of £777. You can find more detailed statistics here. This highlights the importance of staying informed about market fluctuations and their potential effects on your insurance costs.

By thoroughly exploring available discounts, meticulously documenting your eligibility, and strategically managing loyalty programs, you can uncover significant savings opportunities and substantially lower your car insurance premiums. Proactive and informed cost management is key.

Mastering the Art of Insurance Negotiation

Mastering the art of insurance negotiation means knowing how to effectively lower insurance premiums. A well-executed negotiation strategy can result in significant savings. By understanding the process, you can significantly reduce your car insurance costs. This section explores proven negotiation techniques, from gathering quotes to understanding persuasive communication.

The Power of Competing Quotes

Competing quotes are powerful negotiation tools. Gathering quotes from multiple insurance providers shows you're actively seeking the best rate. This encourages your current insurer to match or beat competitor offers.

Not all quotes are equal, however. Generate quotes that accurately reflect your desired coverage levels for a fair comparison. This strengthens your negotiating position. Just as you wouldn't compare a basic car model with a fully loaded version, compare insurance quotes with the same coverage for accuracy.

Timing Is Everything: When to Negotiate

Knowing when to negotiate is crucial. The end of a quarter or fiscal year can be opportune. Insurers sometimes have more pricing flexibility during these periods.

Negotiate when your policy is up for renewal. This is a natural time for reassessment and provides leverage for discussing discounts. Like negotiating a salary raise, you’re more likely to succeed during a performance review.

Documentation: Your Negotiating Armor

Documentation supports your negotiation. This includes your driving record, claims history, and other relevant information. This preparation demonstrates your responsible driving habits.

For example, if you've completed a defensive driving course, have the certificate ready. A clean driving record further strengthens your position. Solid evidence justifies a lower premium.

The Psychology of Persuasion

Effective negotiation involves understanding persuasion. Framing your history positively, emphasizing your loyalty, and using specific phrases can significantly impact the outcome.

Highlighting your long-term customer status and clean driving record appeals to an insurer's desire to retain responsible drivers. Explain your reasons for wanting a lower rate. Mentioning competitor offers and emphasizing loyalty creates a compelling case.

Negotiation Scripts and Insider Tips

A prepared script boosts confidence. Knowing what to say helps you navigate the conversation smoothly.

- Start by expressing your desire to stay with your current insurer, but emphasize the need for a competitive rate.

- Present your competing quotes, highlighting comparable coverage and lower premiums.

- Politely but firmly request your insurer match or beat these offers.

- Be prepared to compromise. Explore other discount options if a full match isn’t possible.

Finally, identify representatives with the authority to approve discounts. Speaking directly with a decision-maker streamlines the process. It often yields better results. By combining these techniques, you can significantly lower your car insurance premiums and control your insurance costs.

Comments are closed.