Knowing When Filing a Claim Makes Financial Sense

Not every minor car accident requires an insurance claim. Sometimes, paying out-of-pocket is the better financial decision. Filing a claim can increase your premiums, even if the accident wasn't your fault. Understanding when to file a claim and when to pay yourself is essential for managing your insurance costs.

Weighing Your Deductible Against Damage Costs

Your deductible is the amount you pay before your insurance coverage begins. If the repair cost is less than your deductible, filing a claim isn't beneficial. For example, if your deductible is $500 and the repair cost is $300, you'll pay the entire $300 yourself. Filing a claim won't reduce your expenses and might increase your premiums.

Also, consider the potential premium increase after filing. Even if the repair cost is slightly higher than your deductible, paying out-of-pocket might be cheaper long-term, especially if it's your first claim in a while.

The Impact of Fault on Future Premiums

Determining who was at fault significantly affects your insurance rates. If you're at fault, expect a substantial premium increase. This happens because the insurance company now considers you a higher risk. But even if you're not at fault, your premiums could still rise slightly, depending on your insurer and state laws.

The accident's severity and the claim amount also influence premium increases. Larger claims, especially those involving injuries, typically result in higher premiums due to the increased cost to the insurance company.

The Rising Cost of Car Insurance Claims

The cost of filing a claim has increased dramatically. Since 2021, average repair costs have risen by about 40% due to higher parts and energy costs. Trade barriers like tariffs on imported auto parts add to the problem, potentially adding $26 to $52 billion annually to U.S. claim costs. This could drive premium increases of up to 19% by 2025. You can learn more about these rising costs here. These factors highlight the importance of carefully considering when filing a claim.

Long-Term Financial Implications

When deciding about filing a claim, think beyond the immediate expense. Consider the long-term financial impact. Multiple claims in a short period can significantly affect your insurability, resulting in higher premiums or even policy cancellation.

Even small claims can have a lasting impact on your insurance costs. Carefully weigh the current repair cost against the potential long-term effects on your premiums. This proactive approach will help you make informed decisions and protect your financial future.

Your Complete Step-By-Step Filing Roadmap

After an accident, navigating the car insurance claim process can feel overwhelming. This section provides a clear roadmap, breaking down the process into manageable steps. We'll cover everything from gathering crucial information immediately after the accident to effectively communicating with your insurance company.

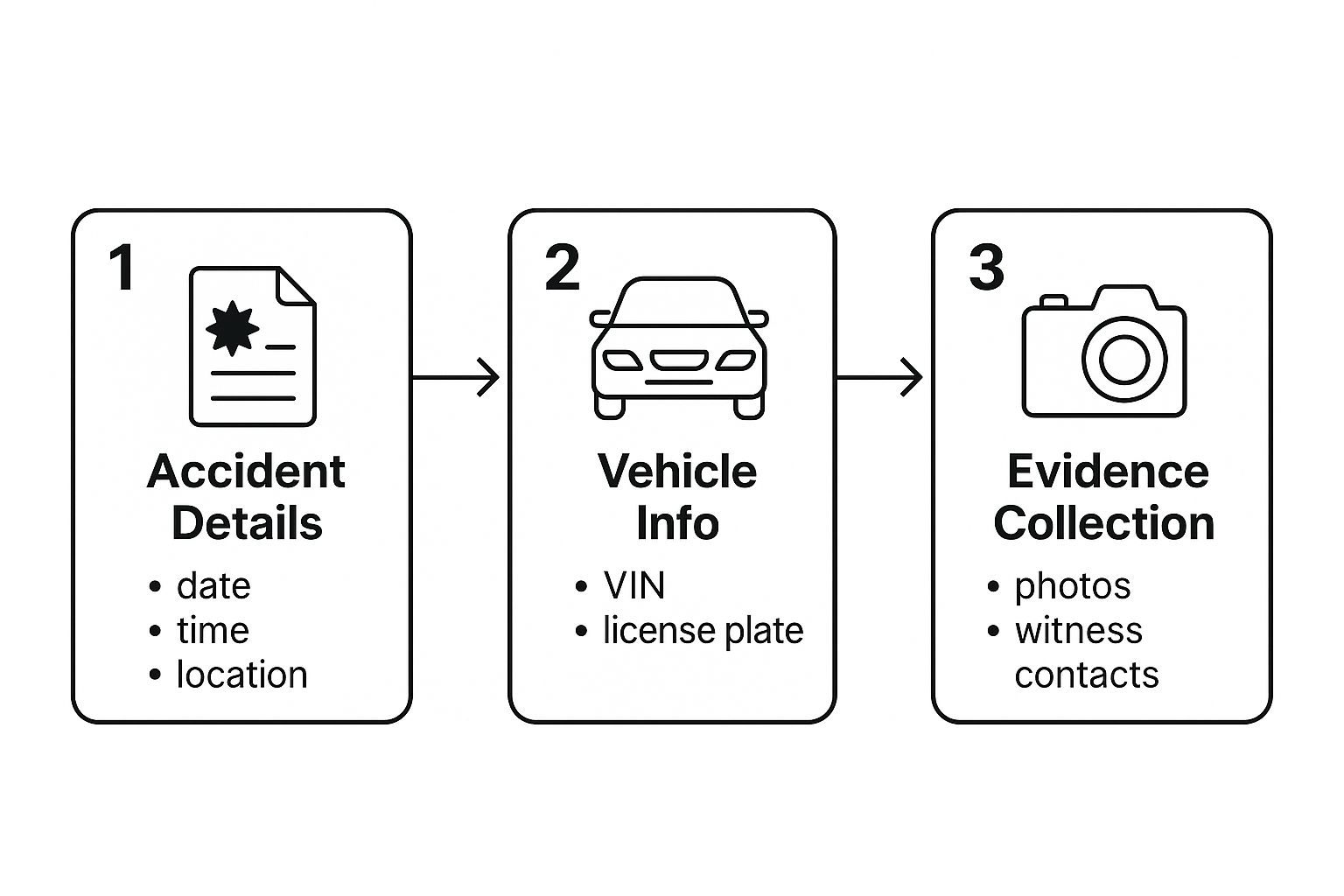

The following infographic visualizes the three key document gathering tasks you’ll need to complete:

Securing the accident details, vehicle information, and collecting evidence form the foundation of a successful claim. Each step builds upon the previous, ensuring a complete record of the incident.

First Steps After an Accident

The moments following an accident are crucial. Even seemingly minor details can significantly impact your claim. Prioritize safety first. If possible, move vehicles to a safe location and check for injuries. Contact the police to report the accident and obtain a police report number. This official documentation is essential for your claim.

Next, gather crucial information. Exchange contact and insurance details with everyone involved. This includes driver's license numbers, insurance policy information, and vehicle details. Document the date, time, and precise location of the accident for accurate record-keeping.

Documenting the Scene

Thorough documentation strengthens your claim. Take photos and videos of the accident scene, capturing vehicle damage, road conditions, and any visible injuries. If there are witnesses, collect their contact information as their statements can be invaluable.

Accurate and detailed documentation provides your insurer with a clear picture of the incident, which can expedite the claims process.

Contacting Your Insurance Company

Contacting your insurance company promptly is a vital step. Provide them with all the gathered information, including the police report number, accident specifics, and contact information for all involved parties. Be clear and concise when describing the events to avoid misunderstandings and delays.

Effective communication with your assigned adjuster is essential. Respond to their requests promptly and ask any clarifying questions you may have. Maintain a detailed record of all communication, noting the date and time of each interaction. To further assist you, we recommend this guide on navigating the aftermath of a car accident and filing a claim. These practices will help ensure a smoother claims experience.

To help you understand the claim filing process, we've compiled a table outlining the general timeline and potential repercussions of delays.

Car Insurance Claim Filing Timeline

Essential deadlines and timeframes for each step of the claim process

| Action Required | Timeframe | Consequences of Delay |

|---|---|---|

| Reporting the accident to the police | Immediately | Difficulty proving fault, potential fines |

| Notifying your insurance company | As soon as possible, typically within 24-72 hours | Potential denial of coverage |

| Gathering evidence (photos, witness statements) | Immediately after the accident | Loss of crucial evidence, weakened claim |

| Completing claim forms | As soon as possible, as directed by your insurer | Delays in processing and settlement |

| Cooperating with the adjuster | Throughout the claim process | Delays in assessment and payout |

| Reviewing the settlement offer | After the adjuster's assessment | Potential acceptance of an unsatisfactory offer |

This table provides a general overview, and specific timeframes may vary based on your insurance policy and state regulations. Adhering to these deadlines is crucial for a successful and timely claim settlement.

Mastering Modern Digital Claims Technology

The insurance industry is rapidly adopting digital tools, with apps and algorithms now playing a significant role in streamlining claims. Understanding these tools can expedite your claim and simplify the entire process. This section explores how technology is transforming claim filing, from mobile apps to virtual inspections.

Using Mobile Apps For Faster Claim Filing

Many insurance companies now offer mobile apps to simplify car insurance claims. These apps provide a convenient platform for submitting photos of the damage, uploading police reports, and even communicating directly with your adjuster. Some apps offer real-time claim tracking, providing updates on repair estimates and payment status. This immediate access to information can save valuable time and reduce the stress often associated with filing a claim.

Navigating Virtual Inspections And AI Assessments

Virtual inspections, utilizing photos and videos, are becoming increasingly common. This allows adjusters to assess damage remotely, often eliminating the need for an on-site visit. Furthermore, some insurers are employing AI-powered tools to analyze damage and provide initial estimates. While these tools offer increased convenience, it's important to be aware of their limitations to ensure a fair settlement.

The growth of technology in claims processing reflects a broader expansion of the insurance claims services market. The global market expanded from $184.93 billion in 2024 to a projected $210.11 billion in 2025. This represents a 13.6% compound annual growth rate. You can explore this growth further in the Insurance Claims Services Global Market Report. This expansion highlights the increasing importance of technology in the insurance industry.

When Human Intervention Is Still Best

While technology is reshaping claim filing, human interaction remains essential. AI and automated systems can sometimes misinterpret damage or undervalue repairs. If you disagree with an automated assessment, it's important to request a review by a human adjuster. For instance, if the AI estimates the damage at $500, but you believe it's closer to $1,000, escalating your concern is crucial. Complex claims, such as those involving disputed fault or significant injuries, often benefit from the expertise of a human adjuster. Knowing when to utilize technology and when to seek human intervention is key to a smooth and successful claims experience.

Navigating Total Loss and High-Stakes Scenarios

A total loss occurs when the cost of repairing your vehicle surpasses its actual cash value (ACV). This can be a stressful experience, especially when navigating the complexities of car insurance claims. This guide explains how insurance companies calculate total loss values and offers strategies for achieving a favorable settlement.

Understanding Total Loss Valuation

Several factors contribute to an insurer's calculation of a vehicle's ACV. The primary factor is the market value of your car before the accident. Insurers typically research comparable vehicles in your area to determine a baseline value. This research includes factors like the year, make, model, mileage, and overall condition of your vehicle.

They also take into account any pre-existing damage or modifications. A well-maintained car with low mileage and upgrades will generally have a higher ACV compared to an older car with high mileage and pre-existing damage. This helps provide a more accurate assessment of the vehicle's worth.

The increasing age of vehicles on the road adds another layer of complexity. The average age of vehicles in the U.S. reached 12.6 years in 2024, a substantial increase from the 9.5 years average in 2002. This trend influences claims as older vehicles are more likely to be declared total losses. For a more detailed analysis of these statistics, refer to this article: Claims Journal.

Negotiating a Fair Settlement

It's important not to immediately accept the insurer's initial offer. Negotiation is often crucial for securing a fair settlement. Conduct independent research on the market value of comparable vehicles to prepare a strong counter-offer. Online resources specializing in used car valuations can be particularly useful.

Remember to highlight any features or upgrades your car possessed that the insurer may have overlooked. Presenting comprehensive evidence supporting your car's value is essential for a successful negotiation. This documentation can strengthen your position during the claims process.

Handling Special Circumstances

Certain situations, like financed vehicles, classic cars, and disputed valuations, require specific expertise during a total loss claim. If you have a financed vehicle, you might owe more on the loan than the car's ACV. Gap insurance can bridge this financial gap.

Valuing classic cars is more complex due to their unique nature and potential for appreciation. Disputed valuations often necessitate careful negotiation and potentially an independent appraisal by a qualified expert. These steps can protect your financial interests in these unique situations.

Understanding Your Rights and Resources

Familiarize yourself with your rights regarding replacement vehicles and the appeals process. Your policy might offer coverage for a rental car while your claim is being processed.

If you disagree with the insurer's valuation, you have the right to appeal. This typically involves submitting additional evidence and possibly consulting with an independent appraiser. Being proactive and informed can significantly improve your experience navigating these often challenging circumstances.

Working With Adjusters Like A Pro

Your insurance adjuster plays a vital role in settling your car insurance claim. A positive and productive relationship with them can significantly impact the outcome. This section offers valuable insights into how adjusters work and provides effective communication strategies.

Understanding the Adjuster's Role

The adjuster's main job is to investigate the accident and evaluate the damage. They'll carefully examine the police report, witness statements, and your description of the incident. The adjuster will also review the damage to your vehicle to determine the necessary repair costs. Ultimately, they decide the amount the insurance company will pay on your claim.

Effective Communication Strategies

Maintaining clear and consistent communication with your adjuster is essential. Respond promptly to any requests for information and keep them informed about changes to your situation. Being organized and proactive demonstrates your commitment to the process, contributing to a smoother claims experience.

Be assertive yet respectful during your interactions. Clearly express your needs and expectations while remaining professional and courteous. This approach fosters a more positive and productive working relationship.

Providing Essential Documentation

The adjuster's decision heavily relies on the documentation you submit. Provide all pertinent information, including photos, videos, and contact details for any witnesses. Include medical bills and repair estimates, if applicable. Accurate documentation is crucial for validating your claim and establishing its scope.

Navigating Difficult Conversations

Disagreements about fault or the settlement amount can sometimes arise. In such situations, remain calm and present your case logically. Use your collected documentation to support your perspective. If you're unsatisfied with the adjuster's response, consider speaking to their supervisor. Having a strategy for these potentially challenging conversations helps maintain a professional demeanor.

Knowing When to Escalate

If you face significant obstacles or believe the adjuster isn't acting fairly, escalate the matter. Contact the insurance company's customer service department or file a formal complaint with your state's insurance regulatory agency. Persistence is key, but knowing when to seek assistance from higher authorities is equally important.

Understanding the adjuster's role, communicating effectively, and preparing for potential challenges can considerably improve your claims process. By being proactive and informed, you can navigate the process with confidence and aim for a fair and timely resolution. This proactive approach ensures you're well-equipped to handle the various stages of your car insurance claim.

Maximizing Your Settlement and Protecting Your Rights

Negotiating a car insurance claim settlement can be a complex and challenging process. Many people accept the first offer from the insurance company, unaware they could potentially receive a much larger settlement. This section equips you with the knowledge and strategies to maximize your settlement and protect your rights every step of the way. You'll learn how to effectively negotiate with insurance adjusters and secure the compensation you deserve.

Documenting Additional Expenses

Car accidents often lead to unforeseen expenses beyond vehicle damage. These can include medical bills, lost wages due to time off work, rental car costs, and even childcare expenses if your injuries prevent you from caring for your children. It's crucial to meticulously document every expense with receipts and invoices. This comprehensive record will support your claim and ensure you are fairly compensated for all losses.

Handling Diminished Value Claims

Even after repairs, an accident can impact your vehicle's resale value. This loss is known as diminished value. You can pursue a diminished value claim to recover this financial loss. To effectively pursue this claim, obtain an independent appraisal from a qualified professional to quantify the diminished value. This assessment provides strong evidence to bolster your negotiation position.

Navigating Repair Shop Relationships

The choice of repair shop can significantly influence the claims process. While you have the right to choose your own shop, some insurance companies have partnerships with specific repair facilities. Understand the implications of choosing a partnered versus an independent shop, and research reputable shops known for quality work and fair pricing. Making an informed decision about your repair shop contributes to a satisfactory repair outcome.

Learn more in our article about how to master car insurance claims.

Negotiating for OEM Parts and Challenging Depreciation

When dealing with repairs, it’s beneficial to advocate for Original Equipment Manufacturer (OEM) parts. OEM parts are generally higher quality than aftermarket parts and can help maintain your car's value. It's also important to challenge unfair depreciation calculations on damaged parts. Insurance companies sometimes undervalue parts based on age or wear and tear. Providing evidence of regular maintenance helps demonstrate the true value of your vehicle's components.

Understanding Your Rights Regarding Rental Coverage and Repair Timelines

Your insurance policy likely provides coverage for a rental car while your vehicle is being repaired. Thoroughly understand the specifics of your rental car coverage, including the duration and any limitations on the type of rental vehicle you can choose. Additionally, establish reasonable repair timelines with both the repair shop and the insurance adjuster. Holding them accountable to a realistic schedule prevents unnecessary delays and minimizes inconvenience.

To understand various coverage options and their impact on settlements, refer to the following table:

Understanding the different types of coverage available and how they affect the settlement process is crucial. The following table provides a comparison:

Types Of Coverage And Settlement Options

| Coverage Type | Settlement Method | Typical Payout | Best For |

|---|---|---|---|

| Collision | Repair or replacement of your vehicle | Actual cash value or repair costs | Accidents involving another vehicle or object |

| Comprehensive | Repair or replacement of your vehicle | Actual cash value or repair costs | Damage not caused by a collision (e.g., theft, vandalism, natural disasters) |

| Uninsured/Underinsured Motorist | Covers medical expenses and lost wages | Varies depending on policy limits | Accidents caused by an uninsured or underinsured driver |

This table summarizes the various coverage types, how they handle settlements, typical payout amounts, and the situations they best address. Having a clear understanding of your coverage is essential for navigating the claims process effectively.

The Appeals Process: When Negotiations Fail

If you are unable to reach a satisfactory agreement with the insurance adjuster, you still have options. Most insurance companies have an internal appeals process, which allows you to formally submit an appeal outlining your reasons for disagreeing with the settlement offer. Understanding how to navigate this process is essential for achieving a fair resolution. If the internal appeal is unsuccessful, consider contacting your state's insurance department or consulting with an attorney. Throughout the claim process, understanding your rights and the resources available to you is vital. Being informed and proactive enables you to negotiate effectively and potentially avoid unnecessary stress and financial loss.

Protecting Your Rates and Future Insurability

Your car insurance claim journey doesn't end with the settlement check. Smart decisions after a claim can significantly impact your future premiums and your standing with insurance providers. Understanding the long-term effects of filing a claim is crucial for maintaining affordable car insurance.

How Long Claims Stay on Your Record

Claims typically remain on your insurance record for three to five years, influencing your perceived risk level. This duration varies depending on the insurance company and the state. Even after a claim disappears from your record, its effects can linger. Insurers often consider your claim history when calculating premiums, even for seemingly unrelated factors. For example, a past at-fault accident could affect your rates when you add a teenage driver to your policy.

Which Claims Impact Rates the Most

Not all claims are created equal. At-fault accidents have the most significant impact on your rates, potentially increasing premiums substantially. Claims involving serious injuries or extensive property damage also lead to higher premiums due to the increased cost to the insurer. Additionally, multiple claims within a short time frame can indicate a higher-risk driver, resulting in steeper premium increases.

Rebuilding Your Claims-Free Discount

Many insurers offer claims-free discounts to reward safe driving habits. Filing a claim, even if you're not at fault, could cause you to lose this discount. However, most insurance companies have programs that allow you to gradually earn back this discount over time by maintaining a clean driving record. For example, some insurers offer a step-down approach where the discount increases incrementally for each year of safe driving after a claim.

When to Switch Carriers

After a claim, comparing quotes from other insurance companies can be beneficial. While loyalty to one insurer can have advantages, sometimes switching carriers is the most cost-effective option. However, remember that all insurers access similar claim history reports. While a new insurer might initially offer a lower premium, your claim history will likely catch up, leading to future increases. Learn more in our article about how to master lowering your car insurance bill.

Proper Claim Closure and Documentation Retention

Even after the settlement, retain all documentation related to the claim. This includes the initial claim form, correspondence with the adjuster, repair estimates, and settlement agreements. Keeping these records ensures you have a complete history of the claim should any discrepancies arise later. Additionally, confirm with your insurer that the claim is officially closed and accurately reflected on your record. This step prevents any surprises when renewing or applying for new insurance coverage.

Building a Positive Relationship With Your Insurer

Maintaining a respectful and professional relationship with your insurance company can be valuable in the long run. Responding promptly to requests, providing accurate information, and communicating effectively helps build trust and can be beneficial during future interactions. While it's essential to advocate for your needs, maintaining a collaborative approach can contribute to a smoother experience overall. This long-term view on relationship management with your insurer can be advantageous when navigating future claims or policy changes.

Comments are closed.