Understanding What You'll Actually Pay For Coverage

When considering disability insurance, the costs can seem confusing. Most people pay between 1-3% of their annual income for comprehensive coverage. For many, this translates to a reasonable monthly premium. However, a number of factors influence the final cost.

Understanding these factors helps you budget and choose the right policy. This means understanding how insurers calculate premiums and what plays the biggest role in determining your monthly payments.

Deconstructing the Premium Calculation

Insurance companies use sophisticated algorithms based on historical data to assess risk. This risk assessment considers several factors.

- Your occupation

- Your age

- Your health history

- The specific terms of your chosen coverage

For example, someone in a physically demanding job might pay a higher premium than an office worker due to the increased risk of injury. This analysis determines how likely you are to file a claim and for how long.

Key Factors Influencing Cost

Several factors can significantly affect your premium. Your occupation plays a large part. A construction worker faces different risks than an accountant, impacting their premium.

Age is another key factor. Younger individuals usually pay less due to a statistically lower risk of disability. Your health status also matters. Pre-existing conditions might increase your monthly cost.

Finally, the benefit period (how long you'll receive payments if disabled) and the elimination period (the waiting time before benefits start) also affect the premium. A shorter elimination period often means a higher premium.

Coverage Type and Cost Variations

Your chosen coverage type significantly impacts the cost. Own-occupation policies, covering you if you can't perform your specific job, tend to be more expensive than any-occupation policies. Any-occupation policies cover you only if you can't perform any job.

This cost difference stems from the broader coverage offered by own-occupation policies. Balancing cost with necessary protection is key when choosing a policy. You might be interested in: Unlocking Life Insurance in 2025: Your Step-by-Step Guide to Choosing Wisely. Understanding these factors allows you to make well-informed decisions about disability insurance.

Key Factors That Actually Drive Your Premium Costs

Your disability insurance premium isn't arbitrary. It's calculated based on specific risk factors identified by insurance companies through years of data analysis. Understanding these factors empowers you to make informed decisions about your coverage and your financial future.

Understanding how these factors interact can help you choose the right coverage at a price that fits your budget. Let's break down the key elements that influence your disability insurance costs.

How Age, Occupation, and Health Impact Your Premium

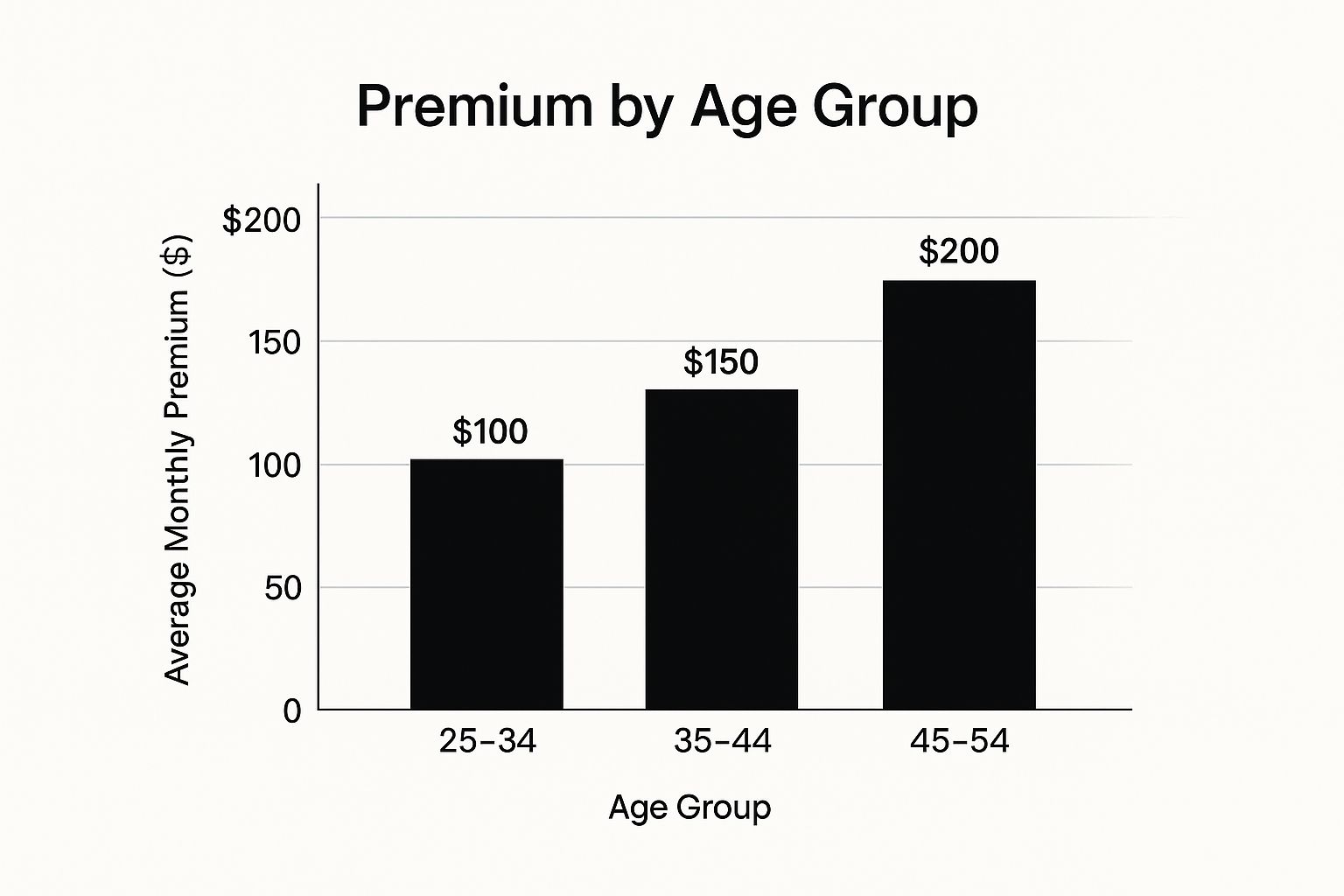

Several key factors play a significant role in determining your premium. Your age is a primary consideration. Younger individuals typically enjoy lower premiums due to a statistically lower risk of disability.

As you grow older, the statistical likelihood of needing disability insurance increases, resulting in higher premiums. The infographic above visually demonstrates how average monthly disability insurance premiums trend upward across different age groups. This reflects the increased probability of disability as we age.

Your occupation also significantly impacts your premium. Individuals in physically demanding or hazardous occupations, such as construction workers, face higher risks of on-the-job injuries compared to those in office settings. This increased risk is reflected in their premiums.

Your health status is another important factor. Pre-existing conditions can influence your premium, as they may increase the likelihood of a disability claim. However, this doesn't preclude you from obtaining coverage. It simply means your premium might be adjusted to reflect the associated risk.

Coverage Choices and Your Bottom Line

Beyond individual factors, your coverage choices directly affect your premium. The benefit period, the duration you'll receive payments if disabled, plays a significant role. Longer benefit periods offer greater financial security but come with higher premiums.

The elimination period, the waiting period before benefits begin, also influences the cost. This functions similarly to a deductible. Shorter elimination periods provide quicker access to benefits but generally mean higher premiums. A longer elimination period can reduce your premium, but you'll need to bridge the financial gap during the waiting period.

The type of coverage you choose also matters. Own-occupation policies, covering you if you can't perform your specific job, tend to be more expensive than any-occupation policies. Any-occupation policies cover you only if you cannot work in any occupation. The price difference stems from the broader protection offered by own-occupation coverage. For those researching how much disability insurance costs, these details are crucial.

To illustrate how these factors can impact your premium, consider the following table:

Premium Factors Comparison Table: A detailed comparison showing how different risk factors affect disability insurance premium costs

| Risk Factor | Low Cost Impact | Medium Cost Impact | High Cost Impact | Premium Difference |

|---|---|---|---|---|

| Age | Under 30 | 30-45 | Over 45 | Can vary significantly, often doubling or more between youngest and oldest age brackets |

| Occupation | Office worker | Teacher | Construction worker | Can range from a few dollars to hundreds of dollars per month |

| Health Status | Excellent health, no pre-existing conditions | Minor pre-existing conditions, well-managed | Major pre-existing conditions | Can significantly impact premium, potentially adding hundreds of dollars per month |

| Benefit Period | 2 years | 5 years | To age 65 | Longer benefit periods significantly increase premiums |

| Elimination Period | 90 days | 60 days | 30 days | Shorter elimination periods lead to moderately higher premiums |

| Coverage Type | Any-occupation | Modified own-occupation | Own-occupation | Own-occupation is typically the most expensive, followed by modified own-occupation, then any-occupation |

This table summarizes the key risk factors and their potential impact on premiums, highlighting the interplay between these elements. Understanding these factors can help you customize a policy that aligns with your individual needs and budget.

Short-Term Vs. Long-Term Coverage: What Each Really Costs

Understanding the differences between short-term and long-term disability insurance is crucial for sound financial planning. While short-term policies may appear more affordable initially, they may not offer the extensive protection you might need in the long run. Let's explore the actual costs associated with each type of coverage and how to determine the best fit for your individual circumstances.

Short-Term Disability Insurance: Initial Costs and Limitations

Short-term disability insurance usually covers a portion of your income (approximately 60-70%) for a limited time, typically between 3 to 6 months. Premiums are generally lower than long-term coverage, making them an attractive option for those on a tighter budget.

However, this lower cost comes with certain limitations. Short-term coverage doesn't address disabilities lasting beyond the benefit period. This could potentially leave a significant gap in your financial safety net. This is a crucial factor to consider when determining your disability insurance needs.

Long-Term Disability Insurance: Investment in Future Security

Long-term disability insurance, on the other hand, is designed for extended disabilities, potentially covering you until retirement. While premiums are higher than short-term policies, they offer a more comprehensive income replacement, typically around 40-60% of your pre-disability income.

This means long-term coverage offers greater financial security, protecting against substantial income loss due to a prolonged illness or injury. The growing emphasis on financial well-being has fueled market growth. The global disability insurance market, estimated at $4.11 billion in 2024, is projected to reach $4.58 billion in 2025, representing a 11.3% CAGR. For more detailed market analysis, see the Disability Insurance Global Market Report.

Combining Coverage for Comprehensive Protection

Many people opt to combine short-term and long-term coverage for maximum protection. The short-term policy covers the initial months of a disability while waiting for the long-term benefits to begin. This effectively bridges the financial gap created by the elimination period of the long-term policy.

This combined approach provides a balance between affordability and comprehensive protection. However, it's important to remember that this strategy might not be suitable for everyone.

Employer-Provided Coverage and Supplemental Options

Some employers offer group long-term disability insurance plans, often reducing costs for employees. However, these plans may have limitations on coverage amounts and definitions of disability.

This often means employees need to evaluate whether supplemental individual coverage is necessary to address potential gaps. Understanding how employer-provided coverage interacts with individual policies is essential for determining the appropriate level of protection.

The Hidden Cost of Coverage Gaps

Not having adequate coverage can lead to serious financial consequences. Lost income, combined with ongoing medical expenses, can quickly deplete savings and result in substantial debt.

This emphasizes the importance of carefully evaluating your individual needs and obtaining sufficient coverage to protect yourself against these potential hardships. Weighing the cost of premiums against the potential financial strain of being uninsured is a crucial step in determining the right amount of disability insurance for your situation.

How Market Growth Is Changing What You Pay

The disability insurance market is experiencing significant growth, impacting pricing and options for consumers. This expansion is largely driven by increased competition among insurance providers, a dynamic that benefits those seeking disability insurance coverage. This translates to more choices and potentially greater value for your insurance investment.

Competition Fuels Innovation and Affordability

As the market grows, insurance companies compete more aggressively for your business. This competition exerts downward pressure on prices and fosters innovation in coverage options. Some insurers are now offering more customizable policies, allowing you to tailor coverage to your specific needs and budget. This trend toward personalization empowers consumers to select plans aligned with their financial goals. Furthermore, the expanding market increases the likelihood of finding a policy that balances coverage and affordability.

More Choices, More Value

The expanding market not only lowers prices but also increases choice. This means access to policies with a wider array of benefits, riders, and payment options. The competitive landscape drives insurers to offer better value propositions, providing more for your premium. This increased accessibility makes disability insurance a viable option for a broader range of income levels. Finding suitable coverage within your budget is becoming more achievable.

The Future of Disability Insurance Pricing

This growth trajectory shows no signs of slowing. The disability insurance market is projected to reach $7.11 billion by 2029, growing at a CAGR of 11.6% between 2025 and 2029. Looking further ahead, the market value is estimated to hit $12.36 billion by 2034, with a CAGR of 11.48% from 2024 to 2034. Learn more about Disability Insurance Market Share. These projections underscore the continued expansion of the sector and the potential for greater innovation and accessibility. Now is an opportune time to explore your options and consider how disability insurance can safeguard your financial future.

Regulation and Technology Drive Accessibility

Regulatory changes and technological advancements further enhance the accessibility of disability insurance. Streamlined online application processes simplify and expedite obtaining coverage. This increased efficiency contributes to cost savings for consumers. Coupled with the expanding market, these developments create a more consumer-friendly environment for those seeking income protection. These trends signal that disability insurance is becoming increasingly integrated into financial planning, making it an essential consideration for securing your financial well-being.

Why Your Location Affects What You Pay

Where you live can significantly impact the cost of your disability insurance. Many people assume insurance pricing is consistent nationwide, but regional differences can lead to substantial premium variations. These variations are due to a combination of factors, including state regulations, the competitive landscape of insurers in your area, and even local demographics.

State Regulations and Their Impact on Premiums

State regulations play a major role in disability insurance pricing discrepancies. Some states mandate specific benefits or place limitations on policy terms, directly affecting coverage costs. For instance, states with stricter regulations concerning pre-existing conditions might experience higher average premiums. Additionally, state-run disability insurance programs, like California's State Disability Insurance (SDI), can influence the pricing and availability of private coverage. This interaction between state and private insurance contributes to a complex pricing structure.

The Competitive Landscape and Your Wallet

Competition among insurance providers in your region can be advantageous. In areas with numerous insurers, companies frequently compete on price to attract customers. This competition can result in lower premiums and more favorable policy terms. Conversely, in areas with fewer insurers, consumers might have limited choices and potentially higher prices. Understanding the competitive landscape in your area can be helpful when negotiating rates and securing the best coverage. You might be interested in: Read also: Understanding the Top Factors That Drive Up Your Home Insurance Costs.

Demographics and Employment Patterns

Local demographics and employment patterns also contribute to regional pricing differences. Areas with a higher concentration of high-risk occupations, such as construction or manufacturing, might experience higher average premiums due to the increased risk of workplace injuries. Moreover, demographic factors like age and overall health within a region can subtly influence insurance pricing. These combined factors illustrate how your location indirectly affects disability insurance costs.

North American Market Leadership

North America currently leads the disability insurance market. In 2024, the North American market reached $1.92 billion, with projections indicating continued growth at a CAGR of 11.60%. This market leadership is partially attributed to supportive government initiatives for people with disabilities and social security benefits that encourage insurance adoption. Explore this topic further. This robust North American market influences global pricing trends, affecting policy choices and costs for consumers worldwide.

Proven Strategies To Lower Your Premium Costs

You don't have to simply accept the first disability insurance premium quote you receive. Smart policyholders use proven strategies to reduce their costs without sacrificing essential coverage. This section explores practical approaches that could potentially save you hundreds or even thousands of dollars throughout the life of your policy. These insights are drawn from real policyholders and insurance professionals experienced in optimizing coverage and minimizing expenses.

Adjusting Elimination Periods: A Powerful Lever for Savings

One of the most effective ways to lower your premium is by adjusting your elimination period. This is the waiting period between when your disability begins and when your benefit payments start, much like a deductible for health insurance. A longer elimination period—for example, 90 days instead of 30 days—can significantly reduce your premium. This means you'll be responsible for covering your expenses during the waiting period, but the long-term premium savings can be substantial.

Optional Riders: Value Versus Expense

Many policies offer optional riders that enhance your coverage. However, not all riders are equally valuable. Some, like a cost-of-living adjustment (COLA) rider, can protect your benefits from inflation and provide true long-term value. Others may be less essential and add unnecessary expense.

Carefully evaluate each rider to make sure it aligns with your needs and doesn't unnecessarily increase your premium. Focus on riders that address your major concerns and offer real value, not just extra features.

Bundling and Group Coverage: Unlocking Discounts

Bundling your disability insurance with other policies, like life insurance, can often result in discounts with some insurers. Similarly, exploring group coverage through professional associations or employer-sponsored plans can significantly lower costs. These group plans often have more competitive rates than individual policies, offering an excellent pathway to affordable coverage. You might be interested in: Learn more in our article about Smart Choices for 2025: How to Find the Perfect Life Insurance Policy.

Timing and Negotiation: Proactive Strategies

Applying for disability insurance while you're young and healthy can secure lower premiums because your risk profile is generally more favorable. Also, don't hesitate to negotiate with insurance companies. While it might seem intimidating, simply asking for a better rate can sometimes yield positive results. This proactive approach can make a real difference in obtaining the most affordable coverage. Comparing quotes from multiple insurers can give you leverage during negotiations, showing that you're aware of market pricing.

To help illustrate these cost reduction strategies, let's look at a comparison of their potential impact. The following table summarizes the key differences and similarities between each strategy.

Cost Reduction Strategies Comparison: A comprehensive comparison of different strategies to reduce disability insurance premiums and their potential savings.

| Strategy | Potential Savings | Coverage Impact | Best For | Implementation Difficulty |

|---|---|---|---|---|

| Longer Elimination Period | Significant | Delays benefit payments | Those with sufficient emergency funds | Easy |

| Decline Unnecessary Riders | Moderate | Reduces coverage enhancements | Those focusing on core income protection | Easy |

| Bundle Policies | Moderate | Potentially no impact | Those needing multiple insurance types | Easy |

| Group Coverage | Significant | May have limited customization options | Those belonging to eligible groups | Moderate |

| Apply While Healthy | Significant | Locks in lower rates for the policy term | Those in good health and under 40 | Easy |

| Negotiate Rates | Moderate | No impact | Those comfortable negotiating | Moderate |

As you can see, some strategies offer significant savings while others provide more moderate reductions. Choosing the right combination of strategies depends on your individual circumstances and financial situation.

By implementing these strategies, you can take control of your disability insurance costs and ensure you're receiving the best possible value for your investment in income protection. This balanced approach allows you to combine the important protection of disability insurance with responsible financial planning.

Is The Investment Worth It? A Realistic Cost Analysis

Understanding the costs associated with disability insurance is essential. However, the crucial question remains: is it a worthwhile investment? This analysis goes beyond marketing hype, examining real-world scenarios where coverage becomes invaluable. It will help you confidently determine suitable coverage levels and decide if the premiums align with your financial goals.

The Probability of Needing Coverage

While nobody wants to contemplate becoming disabled, the statistical likelihood of needing coverage during your working life is significant. Many underestimate this risk. Understanding the real numbers can be eye-opening. For instance, a 20-year-old worker has a one in four chance of becoming disabled before retirement. This statistic underscores the need for income protection. Planning for potential income disruption isn't merely prudent; it's a practical necessity.

Comparing Premiums to Potential Lost Income

A compelling way to evaluate disability insurance is comparing premium costs to potential lost income. Imagine an unexpected illness or injury prevents you from working. Without disability insurance, your income vanishes, jeopardizing your financial stability. Disability insurance replaces a portion of that lost income, allowing you to manage essential expenses and maintain a reasonable living standard. This income replacement can be the difference between financial security and hardship.

Real-World Examples: The Value of Coverage

Real-world examples highlight the benefits of disability insurance. Consider a skilled professional who suffered a debilitating injury, preventing them from working for years. Their disability insurance policy provided a safety net, covering mortgage payments, medical expenses, and other living costs. This allowed them to focus on recovery without the crushing weight of financial distress. Disability insurance offers peace of mind, financial stability, and the chance to concentrate on healing.

Addressing Common Objections and Misconceptions

Some believe disability insurance is unnecessary or too expensive. These arguments often arise from misconceptions about coverage costs and the likelihood of disability. By comparing premium costs to the potential financial fallout of an extended illness or injury, the value becomes clear. This analysis facilitates informed decisions and empowers individuals to prioritize their financial well-being. Furthermore, strategies exist to manage premium costs, such as adjusting the elimination period or exploring group coverage. Addressing these objections with facts and practical examples provides a comprehensive understanding of disability insurance's value in safeguarding your financial future. This perspective allows you to assess whether the premiums fit within your financial plan.

Comments are closed.