Demystifying Insurance Coverage: What You're Really Buying

Before diving into the specifics of how much insurance coverage you need, let's clarify what it truly means for your financial security. It's more than just a monthly premium; it's a promise of financial protection against unforeseen events. This protection comes in various forms, designed to address specific risks. Understanding these different types of coverage is the first step toward determining your needs.

Decoding Insurance Jargon: Key Terms and Concepts

Understanding the language of insurance policies is crucial. Coverage limits define the maximum amount your insurer will pay for a covered loss. Deductibles represent the amount you pay out-of-pocket before your insurance coverage begins. For example, if your deductible is $500 and you have a $2,000 covered loss, you'll pay the first $500, and your insurance will cover the remaining $1,500. Understanding these interconnected elements is key to making informed decisions. You might also be wondering, like many others, how much life insurance you need.

Another important distinction is between replacement cost and actual cash value. Replacement cost covers the expense of replacing damaged property with new items. Actual cash value, however, factors in depreciation. This difference can significantly impact your financial recovery after a loss. The type of insurance you need also influences the appropriate coverage amount. For example, in personal lines Property & Casualty (P&C) insurance, global premiums grew by 9.5% from 2022 to 2023, totaling $1.1 trillion. This growth surpassed nominal global GDP by half a percentage point, highlighting the increasing demand for insurance coverage.

Why Generic Advice Falls Short: Understanding Your Unique Needs

Generic coverage recommendations often fall short because individual circumstances vary. Insurance carriers evaluate risk based on several factors, including your age, location, credit score, and claims history. What's adequate for one person might be insufficient for another. Many people find themselves financially vulnerable after claims because they relied on one-size-fits-all advice.

Finding the right amount of coverage involves identifying the optimal balance between inadequate protection and excessive premiums for unnecessary coverage. It requires careful evaluation of your personal finances, assets, and potential risks. Understanding how insurance works and how carriers assess risk empowers you to make informed decisions that provide genuine financial security.

Home Insurance Coverage: Beyond Standard Formulas

Calculating sufficient home insurance coverage involves more than just using an online calculator. It requires careful consideration of various factors to build a truly personalized plan that goes beyond simple formulas. This includes understanding the key difference between your home's market value and its rebuilding cost, which are often two very different numbers. This is critical because, if your home is destroyed, you need enough coverage to rebuild it, not just to purchase a comparable property.

Accurately Estimating Rebuilding Costs

One of the most important steps in determining appropriate home insurance coverage is getting an accurate estimate of rebuilding costs. This includes the cost of materials, labor, and permits necessary to reconstruct your home. Factors like local construction costs, the complexity of your home’s design, and even recent price hikes for building materials can all have a significant impact on this number. Investing in a professional appraisal specifically for rebuilding costs is a smart way to ensure you're working with reliable figures.

Inventorying Your Possessions: A Systematic Approach

Figuring out how much coverage you need also involves creating a comprehensive inventory of your belongings. This isn't just a mental checklist; it's a detailed record, ideally with photos or videos, and documentation like receipts. This inventory serves two important functions. It helps you accurately assess the value of your personal property for insurance purposes and it makes the claims process much smoother if you ever need to file one. Having this detailed documentation is extremely helpful when dealing with insurance companies after a loss.

High-Value Items: Beyond Standard Coverage

Standard home insurance policies typically have coverage limits for certain categories of items, like jewelry, artwork, or collectibles. If you own high-value items, you'll probably need extra coverage called scheduled personal property coverage to ensure these items are fully protected. This involves individually listing and appraising each item, adding an additional layer of protection to your overall coverage.

Liability Protection: Assessing Your Risk Exposure

Liability coverage protects you financially if someone is injured on your property and decides to sue. While standard policies offer some liability protection, it might not be sufficient. Think about your lifestyle, how often you have guests, and the possibility of accidents when deciding on the right amount of liability coverage. Having adequate liability protection is vital for financial security in case of unexpected events. You might be interested in: How to Secure the Best Home Insurance Coverage in 2025.

Additional Living Expenses: Planning for Displacement

If your home becomes uninhabitable due to a covered incident, additional living expenses (ALE) coverage helps cover the costs of temporary housing, meals, and other essential living costs. Calculating the appropriate ALE coverage involves considering things like local housing costs, the potential length of your displacement, and the availability of alternative housing options. Planning for this in advance ensures you have the financial resources to maintain your lifestyle while your home is being repaired or rebuilt. A careful evaluation of these factors provides a clear understanding of your individual insurance requirements, allowing you to secure the correct coverage amount for your specific needs.

To help illustrate the different components of home insurance and recommended coverage amounts, the following table provides a useful breakdown:

Home Insurance Coverage Components

| Coverage Type | What It Covers | How Much You Need | Calculation Method |

|---|---|---|---|

| Dwelling | The physical structure of your house (walls, roof, floors). | Enough to rebuild your home | Reconstruction cost estimate from a contractor or appraiser (not market value) |

| Other Structures | Detached structures like garages, sheds, fences. | Typically 10% of dwelling coverage | 10% of dwelling coverage amount |

| Personal Property | Your belongings (furniture, clothing, electronics). | Enough to replace your possessions | Detailed home inventory with estimated replacement values |

| Loss of Use/ALE | Additional living expenses if your home is uninhabitable. | Enough to cover temporary housing and living costs. | Consider factors like hotel rates, restaurant meals, and transportation expenses. |

| Liability | Covers legal fees and medical bills if someone is injured on your property. | At least $300,000, but higher limits are recommended. | Assess your risk tolerance and potential liability exposure. |

| Medical Payments | Covers medical bills for minor injuries to guests on your property, regardless of fault. | Typically $1,000 to $5,000 | Based on desired coverage level |

This table summarizes key coverage types and how to determine the right amount for each. Remember, consulting with a qualified insurance professional can provide personalized guidance tailored to your specific circumstances.

Auto Insurance Protection: Why Minimums Leave You Exposed

State-required minimum auto insurance coverage fulfills legal obligations, but it may not offer sufficient financial protection after an accident. Opting for the minimum might seem budget-friendly, but it can expose drivers to substantial financial risks. How much coverage is truly necessary? Let's explore why minimums often fall short.

The Illusion of Sufficiency: Minimums vs. Reality

Consider this: you're involved in an accident resulting in significant injuries and property damage exceeding your minimum coverage. Suddenly, you're personally responsible for the remaining expenses, including medical bills, legal fees, and vehicle repairs. This can lead to financial hardship, depleting savings or resulting in wage garnishment.

Furthermore, medical and vehicle repair costs are constantly increasing. Adequate coverage from a few years ago might be insufficient today. Market trends and economic conditions also influence insurance needs. In 2023, global non-life insurance premiums rose by 3.9% in real terms, partially due to insurers raising rates to offset rising claims costs. This trend is evident in regions like the UK and Australia, where personal property and auto insurance premiums have surpassed inflation and disposable income growth over the past three years. Explore this topic further. This highlights the need to review your coverage regularly.

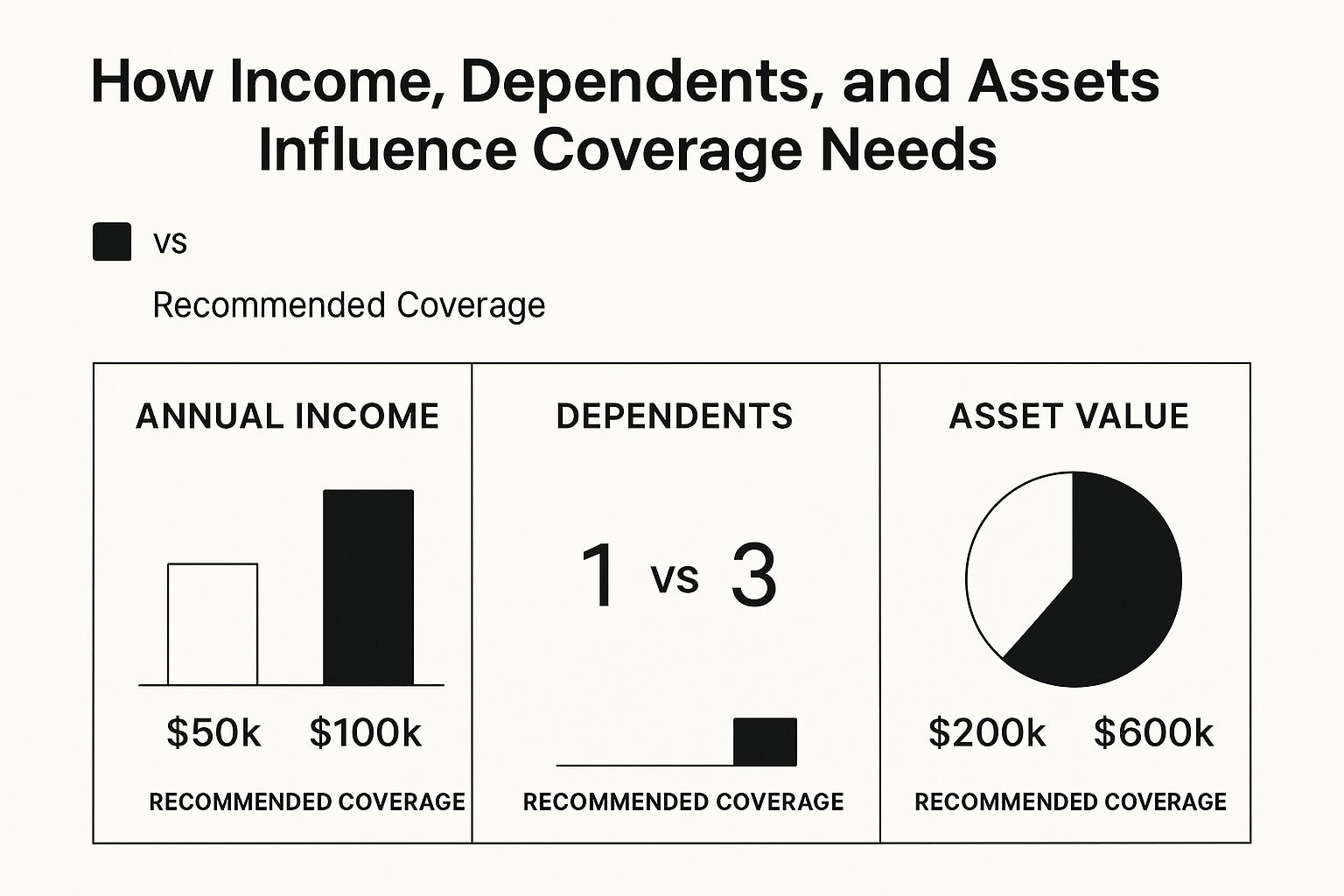

Calculating Appropriate Coverage: A Personalized Approach

Determining the right auto insurance coverage depends on individual factors. Annual income, dependents, and asset value all play a role. The infographic below demonstrates how these factors influence recommended coverage levels.

As income, dependents, or asset value increase, so does the recommended coverage. This visualization emphasizes the importance of tailoring coverage to your financial situation. It's not a one-size-fits-all solution.

Balancing Protection and Budget: Strategic Coverage Choices

Balancing comprehensive protection and affordability requires understanding auto insurance components. Prioritize coverage based on individual needs. To help you understand the differences and make informed decisions, let's look at a comparison of minimum and recommended coverage levels:

Auto Insurance Coverage Comparison

Comparison of minimum state requirements versus recommended coverage levels

| Coverage Type | State Minimum Example | Recommended Coverage | Potential Cost of Inadequate Coverage |

|---|---|---|---|

| Liability Coverage | $25,000 bodily injury per person / $50,000 bodily injury per accident / $25,000 property damage | $100,000/$300,000/$100,000 or higher | Lawsuits, wage garnishment, asset seizure |

| Collision Coverage | Varies by state (often none required) | Dependent on vehicle value; consider higher deductible for older cars | Out-of-pocket repair costs |

| Comprehensive Coverage | Varies by state (often none required) | Recommended for newer vehicles and those parked in high-risk areas | Out-of-pocket repair/replacement costs due to theft, vandalism, weather, etc. |

| Uninsured/Underinsured Motorist Coverage | Varies, often similar to liability minimums | Match your liability limits; consider higher limits | Medical expenses, lost wages, legal fees if hit by an uninsured/underinsured driver |

| Medical Payments Coverage (Med-Pay/PIP) | Varies by state | Dependent on health insurance coverage | Medical expenses for you and your passengers |

Note: State minimums are examples and vary. Recommended coverage is general guidance. Consult with an insurance professional to determine appropriate limits.

As the table demonstrates, sticking with state minimums across different coverage types can leave you vulnerable to significant financial burdens in the event of an accident. While recommended coverage may have higher premiums, it provides a stronger safety net.

- Liability Coverage: Protects you financially if you cause harm to others. Higher limits are crucial.

- Collision Coverage: Covers damage to your vehicle in an accident, regardless of fault.

- Comprehensive Coverage: Covers non-collision incidents like theft and weather damage.

- Uninsured/Underinsured Motorist Coverage: Protects you if hit by an uninsured driver.

- Medical Payments Coverage (Med-Pay/PIP): Covers medical expenses for you and your passengers.

Evaluate your risk tolerance and financial situation to make informed coverage choices. Don't settle for the minimum. Understand your needs and protect your future.

Health Insurance Strategy: Coverage That Actually Works

Choosing the right health insurance is a critical decision. It directly impacts both your physical and financial well-being. It's not a one-size-fits-all approach. Instead, a personalized strategy that addresses your specific needs is essential. This involves a careful evaluation of your healthcare needs and translating them into appropriate coverage. You might find this resource helpful: How to Assess Your Needs and Find the Right Provider.

Assessing Your Health Risks: A Personalized Approach

The first step in determining your health insurance needs involves assessing your health risks. This goes beyond your current health status. Factors like your age, family medical history, pre-existing conditions, and medication requirements are all important. For instance, someone with a family history of heart disease might prioritize coverage with comprehensive cardiac care. Understanding your individual health risks helps you anticipate potential future needs.

Understanding the Trade-offs: Premiums, Deductibles, and Out-of-Pocket Maximums

Navigating health insurance requires understanding premiums, deductibles, and out-of-pocket maximums. Your premium is the monthly payment for coverage. The deductible is the amount you pay out-of-pocket before your insurance kicks in. The out-of-pocket maximum is the most you'll pay for covered medical expenses in a year. A higher deductible often means a lower premium, but also higher upfront costs when you need care. Balancing these factors is key to finding a plan that suits your budget and healthcare needs. The global health insurance market is projected to reach $4.45 trillion by 2032. It's expected to grow at a 9.7% CAGR from its $2.32 trillion value in 2025. Find more detailed statistics here. This highlights the financial importance of the right coverage.

Evaluating Network Adequacy: Access to Quality Care

Choosing health insurance also involves evaluating network adequacy. This refers to the availability of doctors, hospitals, and specialists within your plan's network. A wide network is crucial, ensuring access to needed care. This is particularly important for those with specific healthcare needs or ongoing treatment from specialists. The location of network providers, relative to your home or workplace, is also a factor.

Supplemental Coverage: Dental, Vision, and Critical Illness

Beyond core health insurance, consider supplemental coverages like dental, vision, and critical illness. These can provide significant benefits, especially if you anticipate needing these types of care. Dental insurance helps manage the cost of checkups and procedures. Vision insurance reduces expenses for eye exams, glasses, and contacts. Critical illness insurance provides a lump-sum payment upon diagnosis of a covered illness, offering financial assistance during difficult times. However, carefully evaluate whether these supplemental plans align with your needs or are an unnecessary expense. Understanding these elements helps you create a comprehensive health insurance strategy, balancing cost with comprehensive protection.

Life Insurance Calculation: Beyond Basic Income Replacement

Life insurance is a cornerstone of sound financial planning. It's more than simply replacing your income; it's about securing your family's future and ensuring their lifestyle remains stable if you are no longer around. But how much coverage is enough? The answer depends on several factors specific to your individual situation.

Moving Beyond Simple Multipliers: The Need for a Comprehensive Approach

Traditional methods of calculating life insurance, such as multiplying your income by a set number, often prove inadequate. They don't fully address the complex financial realities of individual families. Income replacement is certainly a key element, but other important considerations must be factored in.

These additional factors include outstanding debts like car loans or credit card balances, your mortgage balance, future education expenses for your children, and even end-of-life costs. A truly comprehensive needs analysis considers all of these components.

The DIME Formula and Needs-Based Analysis: A Deeper Dive

The DIME formula offers a more structured approach. DIME stands for Debt, Income, Mortgage, and Education. This method calculates your life insurance needs by adding together your total debts, your desired replacement income multiplied by a chosen factor, your outstanding mortgage balance, and your children’s projected education expenses. This gives you a broader picture of your family's potential financial obligations.

Even the DIME formula, however, might not encompass all your needs. A full needs-based analysis delves even deeper. It considers your family’s specific circumstances, such as the ages of your children, their anticipated future needs, your spouse's earning potential, and any existing assets like investments or savings. This personalized approach helps determine the most suitable coverage amount.

Life Stages and Coverage: Adapting to Changing Needs

Life insurance needs change over time. A young family with a mortgage and young children has different needs than a couple nearing retirement. A young family might focus on covering the mortgage and their children's education. As children become financially independent, the focus may shift to ensuring a comfortable retirement for a surviving spouse.

Recognizing these evolving needs is essential for adjusting your coverage accordingly. You might find helpful resources like the 2025 Life Insurance Handbook: Expert Tips.

Integrating Existing Assets and Employer Benefits: Avoiding Overlap

Remember to account for your existing assets and any employer-provided life insurance benefits when calculating your needs. These resources can significantly offset your coverage requirements, preventing you from paying for more insurance than necessary. Existing savings, investments, and a spouse’s income all contribute to your family’s overall financial security.

Factoring these elements into your calculations ensures that your life insurance complements your existing resources. This approach allows you to obtain the most efficient and cost-effective coverage. By carefully considering these factors, you can gain a clear understanding of how much coverage is necessary to truly protect your family’s financial future. This careful analysis empowers you to make well-informed decisions and choose a policy that provides lasting security and peace of mind.

Specialized Protection: Coverage Beyond the Basics

Standard insurance policies are fundamental, but they often don't cover every possible scenario. This means there might be gaps in your financial safety net. This section explores specialized insurance options, offering a deeper level of protection and security. Knowing how much coverage you need starts with understanding these options.

Umbrella Insurance: Extending Your Liability Protection

Umbrella insurance provides an additional layer of liability coverage on top of your existing policies, such as homeowner's, auto, or boat insurance. This extra layer can be essential if you face a lawsuit with damages exceeding your current liability limits.

Imagine being involved in a serious car accident resulting in substantial medical expenses for others. If those costs exceed your auto policy's limits, your personal assets could be at risk. An umbrella policy can help protect you in these situations. The appropriate amount of umbrella insurance depends on several factors: your net worth, potential liability risks, and your comfort level.

Disability Income Insurance: Protecting Your Earning Power

What happens if you can't work due to an illness or injury? Disability income insurance can replace a portion of your lost income, helping you cover essential expenses. This type of coverage is especially vital if you're the primary income earner for your family.

The amount of disability income insurance you need depends on your current income and living expenses. Existing savings or investments can also influence your needs. If you have significant financial reserves, you might require less disability coverage.

Long-Term Care Insurance: Planning for Future Needs

As people live longer, the need for long-term care services increases. Long-term care insurance helps cover the cost of these services, which can include nursing homes or assisted living facilities. With healthcare costs continually rising, this type of insurance is becoming increasingly important.

It's important to recognize that long-term care insurance can be expensive. Alternatives include specifically earmarking savings for future care needs or researching government programs like Medicaid. The decision to purchase long-term care insurance is a personal one, based on factors like your health, family history, and financial situation.

Business Insurance: Protecting Your Enterprise

If you're an entrepreneur or involved in a side hustle, business insurance is crucial for protecting your endeavors. There are several types of business insurance to consider. General liability insurance covers injuries or property damage connected to your business operations. Professional liability insurance, often called errors and omissions insurance, protects you against claims of negligence or mistakes in your professional services. Property insurance covers damage or loss of business property.

Determining the appropriate level of business insurance involves assessing your specific business model, potential risks, and industry needs. A consultant, for instance, likely needs more professional liability coverage than a retailer. Choosing the right coverage can safeguard your business from significant financial setbacks.

Choosing the right blend of specialized insurance coverages requires careful planning. Consider your individual needs, financial status, and how much risk you're comfortable with. By understanding these specialized options and evaluating your unique situation, you can build a comprehensive insurance strategy to protect your future.

Insurance Checkups: When and How to Reassess Your Coverage

Life is full of changes. New jobs, new homes, new families—these milestones all affect your insurance needs. Just as your wardrobe evolves over time, your insurance coverage shouldn't stay stagnant. This section offers a practical approach to reassessing your coverage, ensuring you have adequate protection without overspending.

Life Events That Trigger Insurance Reviews

Certain life events warrant an immediate review of your insurance coverage. Buying a new home, for instance, requires updated homeowner's insurance reflecting the property's replacement value. Similarly, a new car necessitates adjustments to your auto insurance. Marriage, the birth of a child, or starting a business are all significant life changes with varying insurance implications.

Even seemingly small changes, like paying off your mortgage or a child graduating college, can influence your life insurance needs. Retirement is another major transition that often requires a comprehensive reassessment of all insurance types, from health and life to auto and home. Proactively reviewing your coverage after these events is essential for maintaining the right level of protection.

Conducting Effective Coverage Audits: Identifying Gaps and Overlaps

A coverage audit is a systematic review of all your insurance policies—a financial health check for your insurance portfolio. It helps identify potential gaps in coverage and eliminate redundant overlaps where you might be paying twice for the same protection.

Begin by gathering all your policy documents. Carefully review the coverage details for each policy, including limits, deductibles, and exclusions. List your assets, potential liabilities, and specific needs to see if your current coverage aligns. For those in specialized fields, consider targeted communication strategies like those used by insurance agents to enhance client interaction. This audit may uncover gaps where you need more coverage or areas where you can reduce coverage to save money.

Working With Insurance Professionals: Optimizing Your Protection

Seeking professional guidance is always a good idea. An insurance agent can offer personalized recommendations, explain complex policy details, and help you choose the best options. They can also answer your questions and assist with comparing quotes from different insurance companies. This expertise is invaluable in ensuring your coverage aligns with your evolving needs.

Building Your Insurance Timeline: Regular Reviews for Different Life Stages

Establish a personalized timeline for regular insurance reviews. Young adults starting their careers might review their policies annually as their circumstances change quickly. Established families may review coverage every two to three years, adjusting for new milestones. As you approach retirement, more frequent reviews can ensure your coverage aligns with your changing financial situation and healthcare needs.

Coverage Evaluation Checklist: A Proactive Approach

Using a coverage evaluation checklist is a proactive way to systematically assess your coverage based on your current life stage, finances, and risk tolerance. A comprehensive checklist covers key areas like home, auto, health, life, and disability insurance, ensuring no crucial aspect of your financial protection is overlooked. By incorporating these strategies into your financial planning, you can effectively manage your insurance needs, ensuring appropriate coverage while avoiding unnecessary costs. This proactive approach empowers you to make informed decisions about your protection, enabling you to adapt to life's changes with confidence and peace of mind. Remember, just as your life evolves, so should your insurance.

Comments are closed.