Why Your Home Insurance Inspection Actually Matters

A home insurance inspection is more than just a routine step; it's a vital part of determining your coverage and premiums. These assessments are becoming increasingly standard practice, allowing insurance companies to accurately evaluate risk and set appropriate pricing. Think of it as a health check for your home, proactively identifying potential issues before they escalate into costly repairs. This preventative approach benefits both the homeowner and the insurance provider.

Understanding the Inspection's Purpose

Insurance companies use these inspections to collect detailed information about your property's condition, including safety features. Inspectors typically assess the age and condition of the roof, the state of electrical and plumbing systems, and the presence of functioning smoke detectors. This data enables insurers to create a comprehensive risk profile for your home. Inspections also help verify the information you provided on your insurance application, promoting transparency and trust between you and your insurer.

Home insurance inspections have become especially important in recent years for both new and existing homeowners. For example, if you're buying an older home or live in an area prone to severe weather events, an inspection is more likely. These inspections are conducted on a case-by-case basis, usually within 30 to 90 days of your policy's effective date. For further information on homeowner's insurance, visit the Insurance Information Institute.

How Inspections Impact Premiums

The results of your home inspection can directly affect your insurance premium. A well-maintained home with up-to-date safety features presents a lower risk and may qualify you for lower premiums. Conversely, if the inspection uncovers significant hazards, such as faulty wiring or a damaged roof, your premium could be higher.

This principle is similar to car insurance where safe drivers with good driving records receive better rates. Maintaining your home effectively mitigates risk and can lead to more favorable insurance terms. This proactive maintenance not only protects your investment but can also save you money on insurance costs. For more on selecting the right coverage, read our guide on choosing a home insurance policy. Understanding these factors helps you manage your insurance expenses effectively.

Inside the Inspector's Mind: What to Actually Expect

So, you've scheduled your home insurance inspection. Now what? This section clarifies the process, providing a clear understanding of what happens from scheduling to the final report. Knowing what the inspector is looking for can ease your concerns and help you prepare.

What Inspectors Look For and Why

Home insurance inspectors aren't expecting perfection; they're assessing risk. Their main objective is to evaluate the overall state of your property and identify potential hazards that could lead to future claims. For instance, they'll check your roof for damage or wear, looking for possible leaks. They'll also inspect electrical systems and plumbing for outdated components or safety issues. This data helps insurers accurately determine your premium based on the probability of a claim.

Should You Be Present During the Inspection?

Attending the inspection is highly recommended. This allows you to address any questions the inspector may have and offer information regarding repairs or upgrades. Consider it an opportunity to showcase your home – your presence demonstrates pride in your property and lets you highlight its positive attributes. You'll also learn firsthand about any potential issues the inspector finds, allowing you to address them proactively.

Preparing for a Smooth Inspection

Preparing for the inspection is straightforward. Having important documents like maintenance records and receipts for recent improvements readily available simplifies the process. This shows you're proactive about home maintenance. Also, ensuring easy access to all areas of your home, including the attic, basement, and crawl spaces, enables the inspector to conduct a comprehensive assessment, preventing delays or a second visit. The satisfaction rate among homeowners who participate in home insurance inspections is significant. For example, 94% of homeowners using platforms like Flyreel expressed satisfaction with their inspection experience. This high approval rating suggests that while inspections might seem intimidating, they are generally positive experiences. Learn more at LexisNexis Risk Solutions.

Addressing Privacy and Disruption Concerns

Homeowners often have valid concerns regarding privacy and disruption during inspections. Rest assured, inspectors are trained professionals who respect your privacy. Their focus is solely on the structural and safety elements of your property, not your personal items. Protecting your home involves more than just physical inspections; it includes financial security as well. You might want to consider exploring options for business insurance. Understanding the inspection process and preparing accordingly ensures a smooth and efficient experience.

Exterior Inspection Mastery: The Critical Checklist

Your home's exterior is the first line of defense against the elements, and it's also the first thing an insurance inspector sees. This initial assessment goes beyond mere curb appeal. It provides crucial insights into the overall condition of your property and the potential risks involved in insuring it. Understanding the inspector's focus is essential for a smooth insurance process and potentially impacts your premiums.

Roof, Gutters, and Drainage

A sound roof is paramount. Inspectors meticulously evaluate its condition, age, and materials. A damaged or aging roof presents a significant risk of leaks and subsequent water damage, which is a major concern for insurers. Clogged gutters and inadequate drainage can also lead to problems, potentially affecting the foundation and causing water damage. Maintaining these systems is crucial for a positive inspection outcome.

Foundation and Exterior Walls

The foundation is quite literally the base upon which your home stands. Inspectors will look for cracks, settling, or any signs of instability that could compromise the structural integrity. The exterior walls, including the siding, are also carefully examined for weather resistance, damage, and general upkeep. Well-maintained siding not only protects your home but also reflects responsible homeownership.

Windows, Doors, and Outbuildings

Windows and doors are checked for proper seals, security features, and signs of vulnerability. Damaged components can lead to security risks and energy inefficiency, both of which are red flags for insurers. Outbuildings such as sheds or detached garages are also evaluated for their condition and potential hazards.

Identifying Red Flags and Their Impact

Certain exterior issues can significantly impact your insurance. A roof nearing the end of its lifespan, substantial foundation cracks, or evidence of water damage can result in higher premiums or even coverage denial. Addressing these issues proactively before the inspection is highly recommended. While the specifics might vary, most inspections include the roof, chimney, gutters and downspouts, foundation, exterior doors, decks, and other outdoor structures. Although homeowners can technically refuse an inspection, this can lead to increased rates or even a loss of coverage. Property damage accounted for 97.8% of homeowners insurance claims in 2021, highlighting the importance of a thorough exterior inspection. For detailed statistics on homeowner's insurance, visit the Insurance Information Institute.

Prioritizing Repairs for Maximum ROI

Understanding which repairs provide the best return on investment from an insurance standpoint is invaluable. Consulting with contractors specializing in insurance-related repairs can provide valuable insights and cost-effective solutions. For example, repairing a damaged roof or ensuring proper drainage can significantly reduce your risk profile and potentially lead to lower premiums.

To help you prepare for your exterior inspection, we've compiled a detailed checklist outlining the critical areas and common issues inspectors look for.

Exterior Inspection Checklist: Critical Areas & Common Issues

This table breaks down the key exterior areas inspectors examine, common problems they look for, and the potential impact on your insurance coverage or premiums.

| Inspection Area | What Inspectors Look For | Common Problems | Potential Insurance Impact |

|---|---|---|---|

| Roof | Age, Material, Condition | Missing shingles, leaks, sagging | Increased premiums, coverage denial |

| Gutters & Downspouts | Proper function, debris-free | Clogs, leaks, damage | Water damage claims, higher premiums |

| Foundation | Stability, cracks, settling | Cracks, uneven settling, water damage | Structural issues, coverage limitations |

| Siding | Material, condition, damage | Rot, cracks, missing pieces | Water damage claims, higher premiums |

| Windows & Doors | Seals, security features | Broken glass, damaged frames, poor seals | Security risks, higher premiums |

| Outbuildings | Condition, structural integrity | Deterioration, damage | Coverage exclusions, liability concerns |

By understanding the key areas of focus for exterior home inspections, homeowners can proactively address potential issues and ensure their property is well-maintained. This preparation not only safeguards your investment but can also lead to more favorable insurance terms and greater peace of mind.

Interior Inspection Success: From Basement to Attic

A home insurance inspection involves a thorough examination of your home’s interior, just as much as its exterior. This assessment offers important details about your home's replacement value, safety, and potential risks. Understanding what inspectors look for can help you prepare and possibly lower your premiums.

Electrical Systems and Wiring

Inspectors meticulously assess your electrical system, including the electrical panel, wiring, and outlets. They look for outdated wiring, potential fire hazards, and any indication of DIY electrical work. This evaluation prioritizes safety and the risk of electrical fires, which can be costly and dangerous. Up-to-code wiring significantly reduces this risk.

Plumbing and HVAC

Plumbing and HVAC systems are critical parts of the inspection. Inspectors examine these systems for leaks, corrosion, and the age and condition of pipes, water heaters, and HVAC units. Even a minor leak can cause substantial water damage over time. Regular maintenance and prompt repairs are essential for these systems.

Structural Elements and Safety Features

The inspector assesses the structural soundness of your home, checking for cracks, signs of water damage, and the state of load-bearing walls. They also evaluate the presence and working order of smoke detectors, carbon monoxide detectors, and fire extinguishers. These safety features help minimize risks and can even result in discounts on your home insurance premiums. These inspections are fundamental for managing risk and ensure the property’s replacement cost is accurately calculated. They also confirm the presence and condition of safety features like fire alarms, anti-theft systems, and fire extinguishers. This comprehensive process aims to uncover potential risks missed on the initial insurance application. Learn more about home insurance inspections.

Attics, Basements, and Utility Rooms

Often overlooked, these areas can hide underlying problems. Inspectors check for proper insulation, ventilation, and any signs of pests or water damage in attics and basements. In utility rooms, the focus is on the condition of appliances such as furnaces and water heaters. Addressing issues in these areas beforehand demonstrates proactive home care. When inspecting your home’s exterior, carefully examine potential points of weather entry. Reviewing practical weatherproofing tips can help you identify and fix vulnerabilities.

Preparing for the Interior Inspection

Simple preparations can significantly impact the inspection process. Decluttering, cleaning, and providing easy access to all areas of your home will make the inspection smoother. Keeping records of recent upgrades and repairs, including receipts, is also beneficial. Understanding what inspectors look for allows you to present your home in its best light. This preparation can contribute to a more efficient inspection and potentially better insurance terms. Through proactive home maintenance, homeowners can confidently address potential problems and safeguard their investments.

Your Pre-Inspection Gameplan: Setting Up For Success

Preparing for a home insurance inspection doesn't have to be stressful. With a strategic approach, you can showcase your home's best features and potentially improve your coverage. We've compiled a timeline and prioritization framework, based on advice from insurance and inspection professionals, to help you prepare effectively.

Prioritizing Tasks For Maximum Impact

Focus on maintenance tasks that make the biggest difference during an inspection. Addressing a minor roof leak now, for example, can prevent costly damage later and improve your inspector's assessment. Functional smoke detectors and an up-to-code electrical panel demonstrate proactive maintenance and a commitment to safety. This signals to insurers that you're a responsible homeowner, potentially impacting your premiums. For more insights on insurance policies, check out this helpful resource: Navigating the Home Insurance Market: Tips for Finding the Best Policy.

Organizing Essential Documents

Gather all relevant documentation, including records of recent repairs, upgrades, and maintenance. Receipts for a new roof or HVAC servicing records are great examples. Organized documentation saves the inspector time and presents a picture of diligent homeownership, showcasing your attention to detail and proactive maintenance.

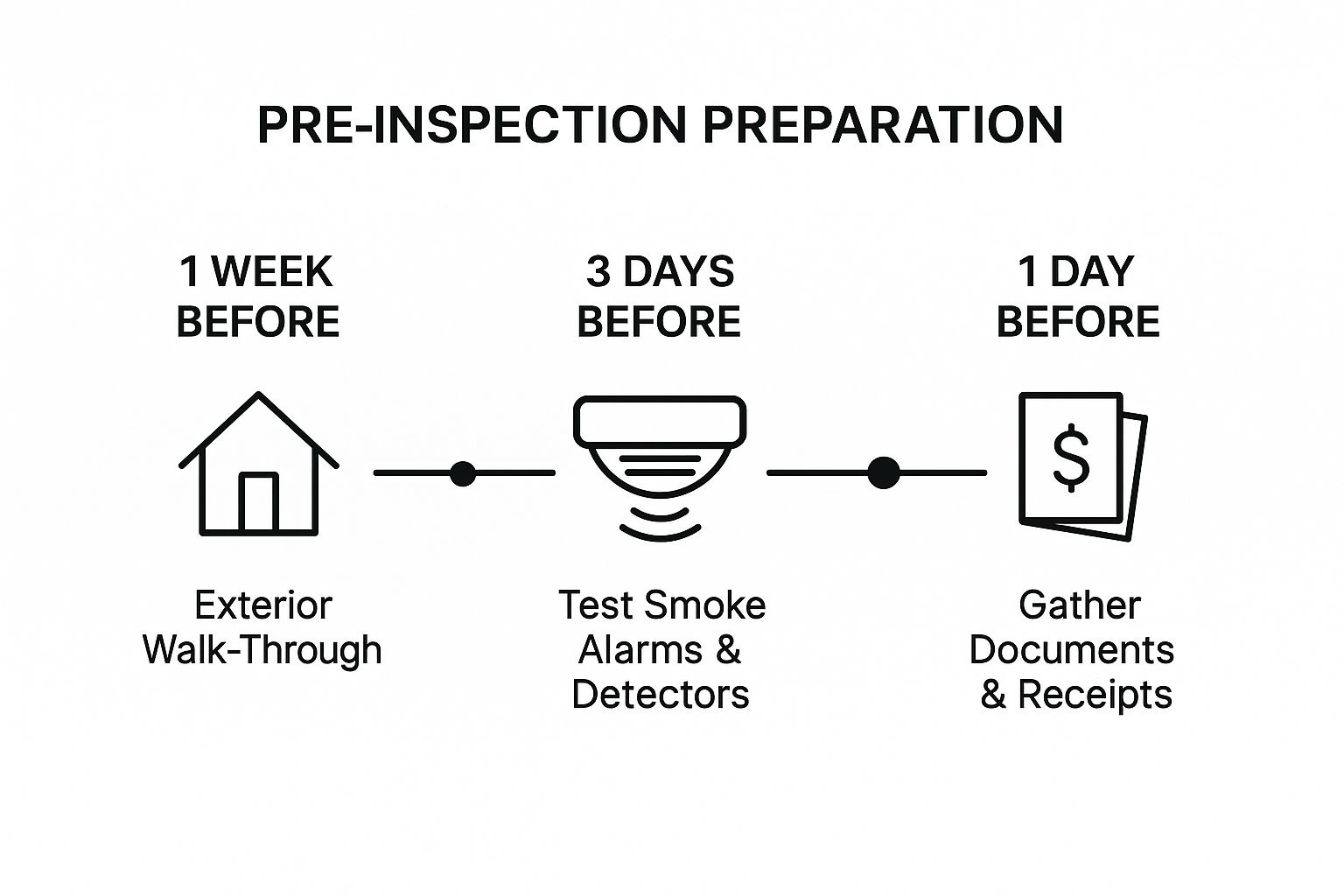

Visualizing Your Pre-Inspection Timeline

The infographic below outlines key pre-inspection milestones to keep you organized:

This timeline visualizes three crucial preparation stages: one week before (exterior walkthrough), three days before (test smoke alarms and detectors), and one day before (compile documents and receipts). These steps ensure a smooth and efficient inspection. These milestones provide ample time to address potential issues and present your home in its best light.

Strategic Planning: Months, Weeks, and Days Before

Our preparation plan outlines what to address in the months, weeks, and days leading up to your inspection. Long-term preparations, like major repairs or upgrades, should begin months in advance. Weeks before, focus on cleaning gutters, decluttering, and yard work. In the final days, concentrate on checking safety devices, gathering documents, and ensuring easy access throughout your home. This structured approach helps avoid last-minute stress and ensures thorough preparation.

It's also important to differentiate between necessary fixes and explainable issues. Some repairs are essential for safety and coverage, while others can be addressed with professional documentation or an explanation to the inspector. This distinction can save you time and money.

A pre-inspection professional assessment can be valuable, especially for older homes or those with potential hidden issues. A professional can identify problem areas and provide cost estimates, allowing you to address significant concerns beforehand and potentially avoid costly surprises. This proactive approach gives you greater control over the inspection process and contributes to a more favorable outcome.

To help you further organize your pre-inspection preparations, we've created a detailed timeline:

Pre-Inspection Preparation Timeline

This table provides a structured timeline of actions to take before your home insurance inspection, from long-term preparations to day-of considerations.

| Timeframe | Areas to Focus On | Recommended Actions | Priority Level |

|---|---|---|---|

| Months Before | Major Repairs & Upgrades | Roof repairs, HVAC system replacement, plumbing upgrades | High |

| Weeks Before | Exterior & Yard Maintenance | Gutter cleaning, landscaping, decluttering outdoor spaces | Medium |

| 3 Days Before | Safety Devices | Test smoke detectors, carbon monoxide detectors, security systems | High |

| 1 Day Before | Document Organization & Accessibility | Compile repair records, ensure access to all areas of the home, confirm appointment details | High |

This table summarizes the key preparation phases, emphasizing the importance of addressing major concerns well in advance and focusing on safety and accessibility in the final days. By following these guidelines, you can approach your home insurance inspection with confidence and ensure a positive outcome.

After the Clipboard: Turning Results Into Opportunities

The home inspection is complete, but the journey to a well-protected and optimally insured property continues. This is where you transform the inspector's findings from potential anxieties into opportunities for improvement. This section guides you through interpreting the inspection report, addressing identified issues, and ultimately strengthening your insurance position.

Decoding the Inspection Report

Understanding the report is the first step. It's a detailed document outlining the inspector’s observations, highlighting both strengths and weaknesses of your property. Pay close attention to any areas marked as needing attention. These are typically categorized by severity, from minor maintenance recommendations to critical repairs requiring immediate action. Think of the report as a roadmap to a safer, more insurable home.

Addressing Identified Issues: A Strategic Approach

Not all issues are created equal. Prioritize repairs based on safety and potential impact on your coverage. For example, a faulty electrical system poses a higher risk than peeling paint, so address it first. For less critical issues, provide supporting documentation to your insurer, demonstrating your awareness and willingness to address them over time. This proactive approach can mitigate potential premium increases.

Negotiating With Your Insurer

The inspection report isn't a final verdict. If you disagree with any findings, you can dispute them with your insurer. Provide supporting evidence like contractor assessments or recent repair records. This is particularly important for issues that could significantly impact your premiums. Effective negotiation involves clear communication and a willingness to find mutually acceptable solutions.

Understanding the Impact on Your Policy

The inspection results can influence your policy terms and premiums. Major issues might lead to higher premiums, while significant improvements could result in discounts. You might be interested in: Understanding Homeowners Insurance: How to Calculate Your Coverage Needs. This knowledge allows you to make informed decisions about your coverage.

Prioritizing Improvements and Exploring Alternatives

Cost-effective prioritization is key. Focus on repairs that offer the greatest impact on both safety and insurance costs. In some cases, exploring alternative coverage options may be beneficial. This is especially true if your home has unique features or is located in a high-risk area. Comparing policies and providers can help you find the best fit.

Proactive Maintenance: Your Long-Term Strategy

Consistent maintenance between inspections is the most effective way to reduce risk and maintain affordable premiums. Regular upkeep, like cleaning gutters and servicing your HVAC system, demonstrates responsible homeownership. This prevents small issues from becoming major problems. This proactive approach not only protects your home but also strengthens your relationship with your insurer, potentially leading to better coverage terms and lower costs over time.

Comments are closed.