Mapping Your Self-Employed Health Insurance Landscape

Navigating health insurance as a self-employed individual can be daunting. Unlike those with employer-sponsored plans, you’re in charge of finding and financing your own coverage. This requires understanding plan types, eligibility, and costs. This section equips you with the knowledge to choose the right health insurance confidently.

Understanding Your Options

The first step is understanding the range of available options. Let’s break down the common choices:

Marketplace Plans: Offered through the Affordable Care Act (ACA) marketplace, these plans provide standardized benefits and potential income-based subsidies. Coverage is guaranteed regardless of pre-existing conditions.

Private Insurance: Purchased directly from insurers, these plans offer greater flexibility in plan design and provider networks. However, they usually have higher premiums and no subsidies.

Short-Term Insurance: Intended for temporary coverage gaps, these plans have lower premiums but don’t cover pre-existing conditions or offer comprehensive benefits.

Health Sharing Ministries: These operate outside traditional insurance, relying on shared member contributions. They may be more affordable but don’t guarantee coverage and have specific eligibility rules.

Professional Association Group Plans: Some professional organizations offer group health insurance to members, potentially with better rates and benefits than individual plans.

Matching Coverage to Your Situation

The best plan depends on your business structure, health needs, and budget. If you expect frequent medical visits, a Marketplace plan with a lower deductible might suit you. If you prioritize lower premiums, a high-deductible plan with a Health Savings Account (HSA) might be better.

Your business structure also affects your options. A C-corp has different opportunities than a sole proprietor. Researching plans specific to your legal structure helps maximize your choices. The private health insurance market is growing, driven by rising healthcare costs and chronic diseases. In 2023, the market was valued at USD 1.2 trillion and is projected to reach USD 2.4 trillion by 2032, a CAGR of 8.1%. Learn more here. This growth underscores the importance of understanding your options.

Navigating Eligibility and Applications

Each insurance type has specific eligibility requirements and application processes. Marketplace plans have open enrollment, while private insurance is often available year-round. Short-term plans have faster approvals but stricter limits. Understanding these nuances is crucial for obtaining timely coverage.

Tips from the Trenches

Here’s advice from experienced self-employed individuals:

Compare Provider Networks: Ensure your doctors are in-network, especially with Marketplace or private plans.

Understand Prescription Drug Formularies: Check if your medications are covered.

Budget for Out-of-Pocket Expenses: Include deductibles, copayments, and coinsurance in your healthcare budget.

Consider an HSA: If you opt for a high-deductible plan, an HSA offers tax advantages and helps save for medical expenses.

By carefully considering your options and using available resources, you can create an affordable health insurance strategy. This allows you to focus on running your business, knowing you have the right coverage.

The Real Cost Breakdown Nobody Talks About

Health insurance for the self-employed can often feel overwhelming. While the monthly premium is the most visible cost, it’s important to understand that it’s just one piece of the puzzle. For effective financial planning, you need a comprehensive view, which means looking beyond the premium to other expenses that can significantly impact your budget.

Hidden Expenses That Catch People Off Guard

Several costs associated with health insurance can catch self-employed individuals by surprise. These often-overlooked expenses can add up quickly, impacting your bottom line. Let’s break down some key terms:

Deductibles: Your deductible is the amount you must pay out-of-pocket for covered healthcare services before your insurance coverage kicks in. For example, with a $2,000 deductible, you’re responsible for the first $2,000 in medical bills.

Copayments: These are fixed dollar amounts you pay for certain services, like doctor visits or prescriptions. Copayments are typically due at the time of service. A common copayment for a doctor’s visit might be $30.

Coinsurance: This is your share of the costs for covered healthcare services after you’ve met your deductible. If your coinsurance is 20%, you’ll pay 20% of the bill, and your insurance will cover the remaining 80%.

Out-of-Pocket Maximum: This is the maximum amount you’ll have to pay out-of-pocket for covered services within a plan year. After reaching this limit, your insurance company covers 100% of the remaining costs.

These costs vary depending on the plan you choose. A high-deductible health plan typically has a lower monthly premium but higher upfront costs. A lower-deductible plan comes with a higher premium but lower out-of-pocket expenses when you need care.

Real-World Examples and Budgeting Strategies

Understanding how these costs play out in real-world scenarios can be helpful. Imagine a freelancer with a high-deductible plan. They might decide to set aside a portion of each payment to cover potential medical expenses before meeting their deductible. Alternatively, a consultant with a lower deductible might prefer the predictability of consistent, lower out-of-pocket costs, even if it means a higher premium.

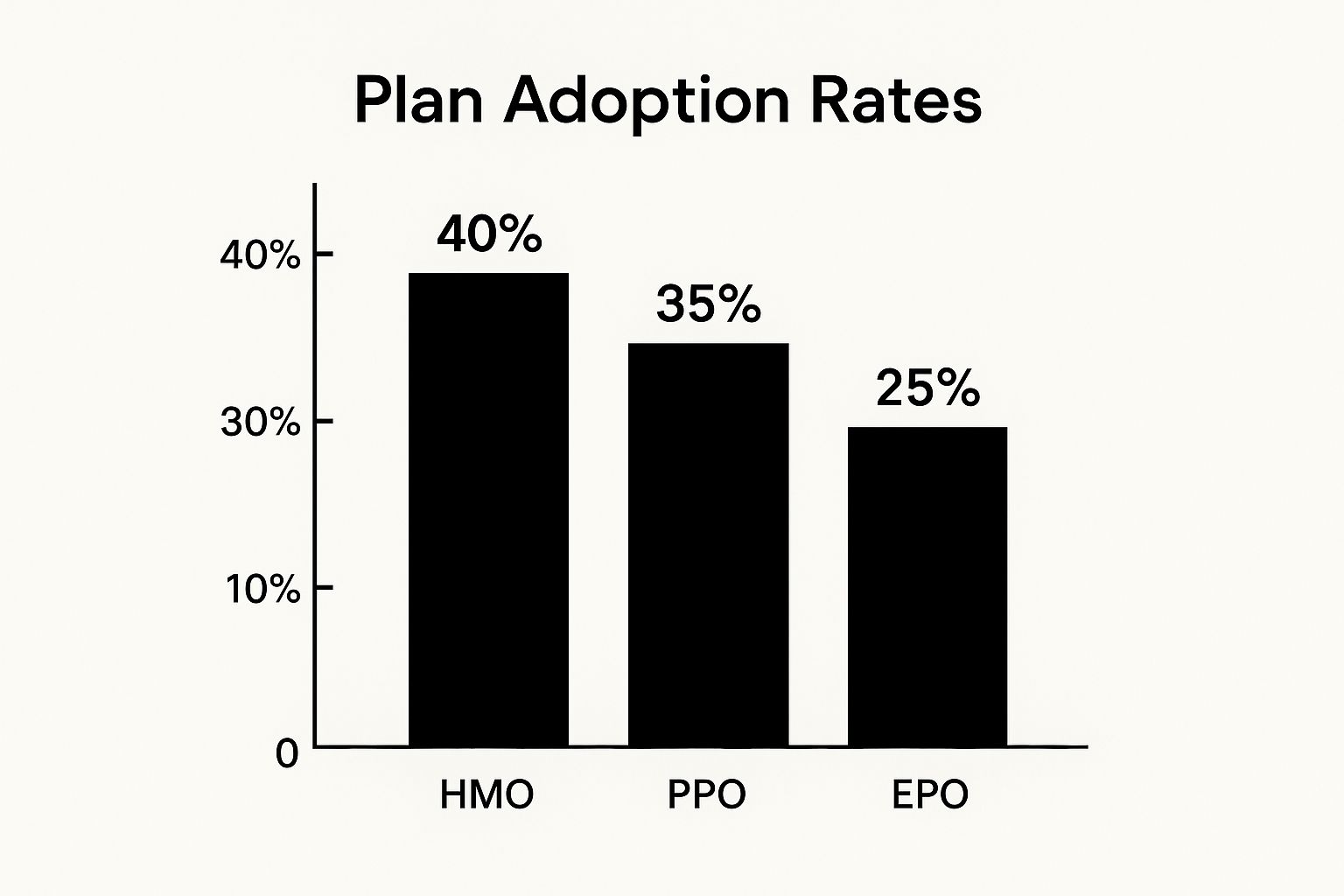

The infographic above illustrates the adoption rates of different health insurance plan types among the self-employed. 40% opt for HMOs, 35% for PPOs, and 25% for EPOs. HMOs remain the most popular option, likely due to their lower premiums and focus on preventative care. PPOs offer broader network flexibility at a somewhat higher cost. EPOs offer a balance between the two, with more limited networks than PPOs but more flexibility than HMOs.

To help visualize the cost differences between common insurance types, let’s look at the following table:

Average Health Insurance Costs Comparison

Compare typical costs between employer-sponsored and individual market plans for self-employed professionals

| Coverage Type | Single Premium | Family Premium | Self-Employed Contribution | Annual Deductible |

|---|---|---|---|---|

| Employer-Sponsored PPO | $8,951 | $25,572 | Variable (often around 50%) | $2,000 – $5,000 |

| Individual Market PPO | $7,200 – $10,800 | $20,160 – $30,240 | 100% | $3,000 – $8,000 |

| Employer-Sponsored HMO | $7,500 | $21,000 | Variable (often around 50%) | $1,000 – $3,000 |

| Individual Market HMO | $6,000- $9,000 | $16,800 – $25,200 | 100% | $2,000 – $5,000 |

Note: These figures are illustrative averages and can vary based on location, age, and plan specifics. Consult with a qualified insurance professional for personalized guidance.

As you can see, individual market plans tend to have higher premiums and deductibles compared to employer-sponsored plans. This highlights the financial responsibility self-employed individuals bear for their health coverage.

Location, Age, and Subsidies

Several factors influence health insurance costs. Premiums tend to be higher in locations where healthcare costs are higher. Age also plays a significant role, as older individuals generally require more medical care.

Some self-employed individuals may qualify for subsidies through the Marketplace, which can lower their monthly premiums. Eligibility is income-based, making healthcare more accessible for those who qualify. In the United States, the cost of health insurance remains a significant concern for the self-employed. For example, in 2024, the average annual premium for employer-sponsored health insurance reached $8,951 for single coverage and $25,572 for family coverage, representing increases of 6% and 7%, respectively, from the previous year. Learn more about health insurance industry trends here. For a more detailed understanding of coverage options, check out this guide: How to master health insurance.

By carefully evaluating these factors and creating a solid budget, self-employed individuals can navigate the complexities of health insurance and obtain the coverage they need without compromising their financial stability.

Marketplace Plans Vs. Private Insurance: Which Wins?

Choosing the right health insurance as a self-employed individual presents a critical decision: Marketplace (ACA) plans or private insurance? This choice goes beyond a simple cost comparison. It’s about finding coverage that truly fits your individual needs. Marketplace plans offer essential health benefits and potential subsidies, while private insurance often provides greater flexibility and wider provider networks. Let’s explore how to navigate this important decision.

Understanding The Marketplace

Marketplace plans, offered under the Affordable Care Act (ACA), provide standardized coverage regardless of pre-existing conditions. These plans cover essential benefits, including hospitalization, maternity care, and prescription drug coverage. A major advantage is the possibility of income-based subsidies, which can significantly lower your costs. However, Marketplace plans have limited enrollment periods, so you can’t sign up whenever you choose.

Exploring Private Insurance

Private insurance, purchased directly from insurance companies, offers greater control over plan design and often includes wider provider networks. This flexibility allows you to tailor coverage to your specific needs and preferences. For example, if seeing a particular specialist is important, you can select a plan that includes them in-network. Keep in mind, though, that private insurance usually comes with higher premiums and you won’t be eligible for subsidies.

Comparing Key Features

The table below summarizes the key differences between Marketplace and private insurance plans:

| Feature | Marketplace Plans | Private Insurance |

|---|---|---|

| Cost | Potentially lower with subsidies | Generally higher premiums |

| Benefits | Standardized essential health benefits | Customizable, may exclude some services |

| Provider Network | Can be limited | Often broader choices |

| Enrollment | Open enrollment periods | Often available year-round |

| Pre-existing Conditions | Guaranteed coverage | May have exclusions or higher premiums |

Scenarios Where Each Option Shines

For lower-income self-employed individuals, Marketplace subsidies can make coverage much more affordable. Imagine a freelancer earning below the subsidy threshold. A Marketplace plan could provide comprehensive coverage for substantially less than a private plan. This makes accessing essential healthcare financially feasible, enabling them to concentrate on growing their business.

On the other hand, a high-earning entrepreneur might prioritize the flexibility and wider network offered by a private plan. They may be willing to pay higher premiums for access to preferred specialists or hospitals, or for more tailored coverage.

Hybrid Approaches And Enrollment Strategies

Some self-employed individuals choose a hybrid approach. They may combine a high-deductible health plan with a Health Savings Account (HSA) to maximize tax advantages and manage costs. Others bridge coverage gaps with short-term insurance. This can be helpful when transitioning between jobs or waiting for Marketplace open enrollment.

Understanding provider networks, prescription drug formularies, and enrollment strategies is crucial. Actively managing your enrollment and coverage helps ensure you’re protected year-round. For example, noting Marketplace open enrollment dates on your calendar can prevent coverage gaps and potential penalties.

By carefully evaluating the advantages and disadvantages of each option, understanding your individual circumstances, and employing effective enrollment strategies, you can secure the best health insurance for your self-employed journey.

Tax Benefits That Actually Save You Money

One of the biggest perks of self-employment is the opportunity to save significantly on health insurance costs through tax deductions. This isn’t simply about getting a refund; it’s about strategically reducing your overall healthcare expenses. Careful planning can have a substantial impact on your financial well-being.

The Self-Employed Health Insurance Deduction

The self-employed health insurance deduction allows you to deduct the premiums you pay for your own health insurance, as well as coverage for your spouse and dependents. This deduction lowers your adjusted gross income (AGI), which directly reduces your taxable income. This can lead to thousands of dollars in savings every year. For instance, if you pay $10,000 in annual premiums and fall into the 22% tax bracket, this deduction could save you $2,200 on your taxes.

There are certain eligibility requirements to keep in mind. You cannot be eligible to participate in an employer-sponsored health plan, even if your spouse has coverage through their employer. Maintaining accurate records is also essential. Keep detailed records of all premium payments, including invoices and payment confirmations. This will simplify things if you are ever audited by the IRS.

Maximizing Savings with HSAs

Health Savings Accounts (HSAs) provide a triple tax advantage for those enrolled in high-deductible health plans (HDHPs). Contributions are tax-deductible, the funds grow tax-free, and withdrawals for qualified medical expenses are also tax-free. This presents a valuable opportunity to build long-term savings while managing current healthcare costs.

HSAs have annual contribution limits, which are adjusted annually. Be sure to review the current limits to maximize your contributions. Many entrepreneurs see HSAs as a key part of their retirement planning, taking advantage of the tax-free growth and withdrawals for future medical needs. This allows them to accumulate substantial health savings while effectively managing current healthcare expenses. Learn more about assessing your healthcare needs and finding the right provider in our article: How to master your health insurance needs.

Claiming Deductions and Staying Informed

You can typically claim the self-employed health insurance deduction on Form 1040, Schedule 1. Using tax preparation software or consulting with a tax professional can simplify this process and ensure accuracy. Tax laws and health insurance regulations are subject to change. Staying updated on these changes, including contribution limits and eligibility requirements, is crucial for maximizing your tax benefits.

Building a Tax-Savvy Healthcare Strategy

Understanding and utilizing the self-employed health insurance deduction and the benefits of HSAs can significantly impact your approach to health insurance. It’s not just about selecting a plan; it’s about developing a comprehensive healthcare strategy aligned with your business objectives and long-term financial well-being. Understanding these benefits not only reduces your current tax burden but also sets the foundation for a more secure financial future. You may find this resource helpful: How to assess your health insurance needs and find the right provider.

Staying Ahead of Industry Changes and Trends

The self-employed health insurance market is in constant flux. Understanding these changes is essential for making informed decisions about your coverage and future planning. This involves keeping abreast of emerging trends, regulatory shifts, and innovative products geared towards independent professionals. By recognizing these opportunities, you can build a proactive and adaptable strategy for your business’s growth.

The Rise of Telemedicine and Personalized Healthcare

Telemedicine has evolved beyond simple video calls to offer a wider range of services for busy entrepreneurs. These include mental health support, specialist consultations, and chronic disease management—valuable features for those with limited time. These advancements offer more convenient healthcare access, making it easier to prioritize your well-being. In addition, data analytics are transforming plan design, leading to more personalized coverage and pricing. This shift allows you to select plans that truly align with your needs.

Regulatory Changes and Gig Economy-Focused Products

The regulatory environment for health insurance is constantly changing. Legislative changes can significantly impact your options and costs. Staying informed about these changes enables proactive adjustments to your coverage strategy. For example, some insurers are now developing products specifically for gig workers and freelancers. This reflects a growing recognition of the unique challenges faced by the self-employed. These specialized products often offer more flexible coverage and address income fluctuations common among independent professionals.

Economic Factors and Industry Growth

Economic factors significantly affect both the availability and cost of health insurance. Inflation, healthcare costs, and broader economic trends all shape the market. The U.S. health insurance sector is projected to grow at a rate of 5%-6% in 2025, despite challenges like weak Medicare Advantage rates and inflationary pressures. More detailed statistics can be found here. This steady growth underscores the continued importance of health insurance. Understanding these broader trends is crucial for long-term planning and making informed decisions about your self-employed health insurance.

Building an Adaptive Coverage Strategy

An adaptive coverage strategy is essential for navigating the evolving health insurance landscape. This involves regularly reviewing your options, staying informed about new products and services, and adapting your coverage to your changing needs. By actively managing your health insurance, you can secure the best possible coverage aligned with your business goals and financial objectives. in-sura-nce.com provides valuable resources and comparisons to help you navigate these choices.

Alternative Coverage Solutions That Actually Work

Finding the right health insurance as a self-employed individual can be a challenge. Traditional plans might not always be the best fit for your budget or needs. Fortunately, several alternative options are available to explore. It’s important to carefully weigh their advantages and disadvantages before making a choice.

Health Sharing Ministries: Community-Based Coverage

Health sharing ministries (HSMs) provide an alternative approach to traditional health insurance. Members contribute to a shared pool of funds used to cover medical expenses. This community-focused model can lead to lower monthly costs. However, it’s crucial to remember that HSMs are not insurance. They don’t guarantee coverage and often have specific requirements, sometimes faith-based. Pre-existing conditions may not be covered, and there’s no legal requirement for the ministry to pay your medical bills.

Short-Term Medical Insurance: Bridging the Gaps

Short-term medical insurance offers temporary coverage, usually with a quicker approval process than traditional plans. This type of coverage is often used to fill gaps between jobs or while waiting for other coverage to begin. Keep in mind that short-term plans typically exclude pre-existing conditions and have limited benefits. They aren’t suitable for long-term needs and may leave you with significant costs if you experience a serious illness during the coverage period.

Direct Primary Care: A Different Approach to Routine Care

Direct primary care (DPC) offers a different way to manage routine medical care. Bypassing insurance, you pay a fixed monthly fee for access to primary care services. This often includes unlimited visits and consultations, potentially reducing the cost of regular checkups and minor illnesses. However, DPC doesn’t cover major medical expenses like hospitalizations or specialist visits. You’ll likely need supplemental coverage, such as catastrophic insurance, for these situations.

Combining Approaches for Comprehensive Coverage

Many self-employed individuals combine these alternatives for a more comprehensive strategy. For example, pairing DPC with catastrophic coverage can offer broader protection while managing expenses. Another common approach is using short-term insurance while waiting for open enrollment in a marketplace plan, ensuring continuous coverage during transitions. You might be interested in: How to master navigating the health insurance maze.

Evaluating Alternatives: Real-World Considerations

Researching real-world experiences is essential when evaluating these alternatives. Some self-employed individuals find HSMs beneficial due to lower costs, while others encounter difficulties when unexpected medical bills arise. Short-term insurance can be helpful for bridging gaps, but its limitations can leave some individuals vulnerable.

To help you compare these different coverage options, the table below summarizes key features, benefits, and limitations:

Health Coverage Alternatives Comparison

Compare features, benefits, and limitations of alternative health coverage options for self-employed individuals

| Coverage Type | Average Cost | Key Benefits | Limitations | Best For |

|---|---|---|---|---|

| Health Sharing Ministry | Varies, generally lower than traditional insurance | Community-based, potential cost savings | Not insurance, may exclude pre-existing conditions | Individuals seeking lower-cost options and who understand the risks |

| Short-Term Insurance | Lower premiums than traditional insurance | Temporary coverage, faster approval | Limited benefits, excludes pre-existing conditions | Bridging coverage gaps |

| Direct Primary Care | Fixed monthly fee | Unlimited primary care visits, direct access to physician | Doesn’t cover major medical events | Routine care and cost predictability |

Choosing the right health insurance strategy requires careful evaluation. Consider your individual needs and budget to determine the best fit for your self-employed lifestyle. Researching available options and learning from the experiences of others are key steps in making informed decisions about your healthcare coverage.

Key Takeaways

Securing the right health insurance as a self-employed professional requires careful planning and a deep understanding of your options. This guide offers practical steps to help you evaluate your needs, compare plans, and avoid common pitfalls.

Evaluating Your Needs

Before comparing plans, assess your individual healthcare needs. This involves considering factors like your current health status, anticipated medical expenses, and risk tolerance. Ask yourself:

- How often do you visit the doctor?

- Do you have any pre-existing conditions?

- What’s your budget for healthcare?

- Are you comfortable with a higher deductible for lower premiums?

Honestly answering these questions helps you focus on plans that align with your requirements. For example, if you anticipate frequent doctor visits, a lower-deductible plan might be better. If you prioritize lower monthly premiums, a high-deductible plan with a Health Savings Account (HSA) could be a better fit.

Comparing Plans Effectively

Once you understand your needs, compare plans based on key factors:

- Monthly premiums

- Deductibles

- Copayments

- Coinsurance

- Out-of-pocket maximums

- Provider networks

Use online comparison tools and contact insurance representatives for detailed information. Ask specific questions:

- What services are covered?

- What’s the cost-sharing structure for different services?

- Are my preferred doctors in-network?

- What’s the plan’s prescription drug formulary?

Creating a table to compare plans side-by-side can be invaluable, allowing you to visualize differences and make informed decisions.

Avoiding Common Pitfalls

Several common mistakes can lead to higher costs and coverage gaps:

- Overlooking Hidden Costs: Factor in expenses like deductibles, copayments, and coinsurance beyond the monthly premium.

- Ignoring Provider Networks: Ensure your preferred doctors are in-network to avoid higher costs.

- Missing Open Enrollment Deadlines: If choosing a Marketplace plan, note open enrollment dates to avoid coverage gaps and penalties.

- Not Reviewing Coverage Annually: Re-evaluate your needs and plan options each year to ensure your coverage is still appropriate.

Documentation and Ongoing Management

Keep copies of your policy documents, premium payment confirmations, and correspondence with your provider. This is helpful during claims and tax filing. Review your coverage annually or after significant life changes, like marriage or having a child. Your needs and ideal plan can change, so regular evaluation is crucial.

As a self-employed individual, managing health insurance is an ongoing process. By actively evaluating your needs, comparing plans strategically, and avoiding common pitfalls, you can secure coverage that protects your health and finances. Consider alternatives like Health Sharing Ministries, short-term plans, and Direct Primary Care. In-sura-nce.com can help you find the right policy. They offer expert reviews, comparisons, and practical advice to navigate the complexities of health insurance for the self-employed, plus information on other types of insurance.

Comments are closed.