Understanding When Singles Actually Need Life Insurance

Many single individuals often wonder if life insurance is truly necessary. Without a spouse or children relying on their income, it can feel like an added expense. However, several situations highlight the importance of life insurance as a valuable financial tool, even for those without a family. It's less about income replacement and more about shielding loved ones from potential financial burdens.

Protecting Your Family and Legacy

Life insurance is paramount for single people with dependents, such as children or elderly parents. It acts as a safety net, ensuring their financial stability if the unexpected happens. The death benefit can help with daily expenses, future education costs, or ongoing caregiving needs. This prevents significant financial hardship for those who depend on you.

Even without dependents, outstanding debts like student loans, mortgages, or co-signed loans can become problematic for family members. Life insurance can cover these liabilities, preventing loved ones from inheriting debt. This is particularly crucial if you've co-signed a loan with a family member.

The increasing need for life insurance among singles with financial responsibilities is becoming more recognized. For example, in 2023, 59% of single mothers expressed a need for life insurance to protect their children's financial future. In the United States, with the average life insurance payout around $160,000, having coverage can significantly lessen the financial strain on loved ones. Learn more about life insurance trends at Feather Insurance. This reinforces the idea that life insurance isn't just for families; it's a responsible financial strategy for anyone with significant financial obligations.

Covering Final Expenses

Another important reason for singles to consider life insurance is to cover final expenses. Funeral costs can be substantial, and an unexpected death can place a financial burden on family members left to manage these arrangements. A life insurance policy can provide the necessary funds to handle funeral arrangements and other end-of-life expenses, easing the burden during an already difficult time.

This is especially relevant for singles without substantial savings or assets. Planning for these eventualities, while it may seem distant, is a responsible financial practice. A smaller policy specifically designed to cover final expenses can be a cost-effective way to protect your family from unexpected costs.

Securing Your Future

Beyond immediate needs, life insurance can also contribute to long-term financial planning for single individuals. Some policies, such as whole life insurance, accumulate cash value over time. This cash value can be borrowed against or withdrawn under certain circumstances, providing a potential source of funds for future goals like a down payment on a house or supplementing retirement income.

However, it's essential to carefully evaluate the costs and benefits of these types of policies. Term life insurance, which offers coverage for a specified period, is often more affordable for those primarily concerned with immediate financial protection. The key is to assess your individual situation and financial objectives to determine the most suitable coverage.

Critical Situations Where Coverage Becomes Non-Negotiable

While life insurance needs vary for single individuals, certain situations make it crucial. These circumstances present significant financial risks to loved ones if you're uninsured. Understanding these scenarios helps determine if life insurance is right for you.

Providing for Dependents

For single parents, life insurance is essential. It's the foundation of their children's financial security. This coverage replaces lost income, ensuring children can maintain their current lifestyle and meet future needs, such as education. Without life insurance, children could face hardship after a parent's death. This coverage safeguards their future.

Beyond children, caring for aging parents also underscores the importance of life insurance. If you're single and financially supporting your parents, your absence would create a financial gap. Life insurance can provide funds for their ongoing care, maintaining their stability and quality of life.

Managing Shared Financial Obligations

Co-signed loans and business partnerships present additional situations where life insurance becomes vital for single people. If you co-signed a loan and pass away, the other borrower becomes solely responsible. Life insurance can cover the outstanding balance, protecting your co-signer and family from inheriting the debt.

Similarly, in business partnerships, life insurance can fund a buyout of your business share. This protects business continuity and ensures fair asset distribution to your estate and partner. This prevents potential conflicts and preserves your business.

Addressing Debts and Final Expenses

Even without dependents, outstanding debts necessitate life insurance. Student loans, mortgages, and credit card balances become the responsibility of your estate. This can burden family members left to settle these debts. Life insurance provides funds to cover these obligations, shielding your loved ones from inheriting financial liabilities.

Furthermore, final expenses, including funeral costs, can strain your family financially. A life insurance policy, even a smaller one, ensures these expenses are covered. This protects loved ones from unexpected costs during a difficult time.

Assessing Your Needs

Deciding if you need life insurance involves assessing your financial obligations and the potential impact of your absence. Consider who depends on you financially, if you have significant debts, and how your loved ones would manage final expenses. If any of these reveal a potential financial burden, life insurance becomes a necessary safety net, providing financial peace of mind for you and your loved ones.

When You Can Safely Skip Life Insurance (And Save Money)

Life insurance is a vital financial tool for many. However, certain single individuals may find it an expense they can forgo. Knowing these circumstances can free up funds for other financial goals. This section will help you decide if skipping life insurance makes sense for you.

No Dependents and Minimal Debt

If you are single, have no dependents, and minimal debt, life insurance might not be necessary. This is particularly true if you have enough assets to cover final expenses, such as funeral costs. If your savings and investments already cover these costs, a separate life insurance policy could be redundant. Your existing resources can handle potential end-of-life expenses without burdening anyone else.

Also, if no one relies on your income, the need for the income replacement a life insurance policy provides is lessened. This allows you to consider other investments aligned with your long-term financial goals, like retirement planning or building wealth.

Self-Insurance Through Strategic Savings and Investments

Some single individuals choose self-insurance. They do this by building a healthy emergency fund and investing strategically. This involves setting aside money specifically for potential expenses that life insurance would typically cover. These expenses can include funeral costs or outstanding debts. A dedicated savings account or investment portfolio can achieve this goal. This strategy allows you to directly manage your finances and potentially see higher returns than a traditional life insurance policy.

Evaluating Your Financial Picture

To determine if skipping life insurance is right for you, carefully consider your financial situation.

-

Calculate your net worth: Add up your assets (savings, investments, property) and subtract your liabilities (debts). A positive net worth, especially one exceeding anticipated final expenses, often indicates that life insurance may not be needed.

-

Project future expenses: Estimate potential future costs. Include funeral expenses, outstanding debts, and any financial support you might provide to family members. This will help you see if your current resources are sufficient.

-

Analyze your risk tolerance: Think about your comfort level with financial risk. Self-insurance requires a higher risk tolerance than having a life insurance policy.

If, after careful consideration, you decide life insurance isn't right for you now, look into other investment strategies. Think about maximizing contributions to retirement accounts, diversifying your investment portfolio, or paying down existing debt. These options often provide greater financial flexibility and potential long-term growth. However, consulting with a financial advisor is always recommended for a personalized financial strategy. Whether or not single people need life insurance depends entirely on their individual circumstances.

Choosing The Right Life Insurance Type For Your Situation

Navigating the world of life insurance can feel daunting, especially when you're single. Choosing the wrong policy can lead to unnecessary expenses or insufficient coverage. This section clarifies the key differences between term life insurance and permanent life insurance for single individuals.

Term Life Insurance: Temporary Protection

Term life insurance offers coverage for a set period, such as 10, 20, or 30 years. It's generally more affordable than permanent life insurance, making it a budget-friendly option for temporary needs. For single individuals with a mortgage, term life insurance can provide coverage until the loan is paid off, protecting loved ones from inheriting the debt. Similarly, single parents can use term life insurance to cover their child-rearing years.

Permanent Life Insurance: Lifetime Coverage and Investment Component

Unlike term life insurance, permanent life insurance offers lifelong coverage. It also includes a cash value component, which is an investment feature that grows over time. You can borrow against or withdraw from the cash value, providing a potential source of funds for future needs. However, permanent life insurance typically comes with higher premiums than term life insurance due to the lifelong coverage and cash value feature. For singles, this type of policy can be a good fit if they prioritize long-term financial security and have a larger budget for premiums.

Other Insurance Options for Singles

Single individuals should also explore other coverage options beyond term and permanent insurance. Many employers offer group life insurance as a benefit, which is often more affordable than individual policies. While it can provide a basic level of protection, group life insurance typically offers lower coverage amounts and might not meet all your needs. You might find this resource helpful: Navigating the Future: A Guide to Choosing the Right Life Insurance Policy. Additionally, some insurers offer specialized products for single demographics, along with supplemental coverage options to enhance existing policies.

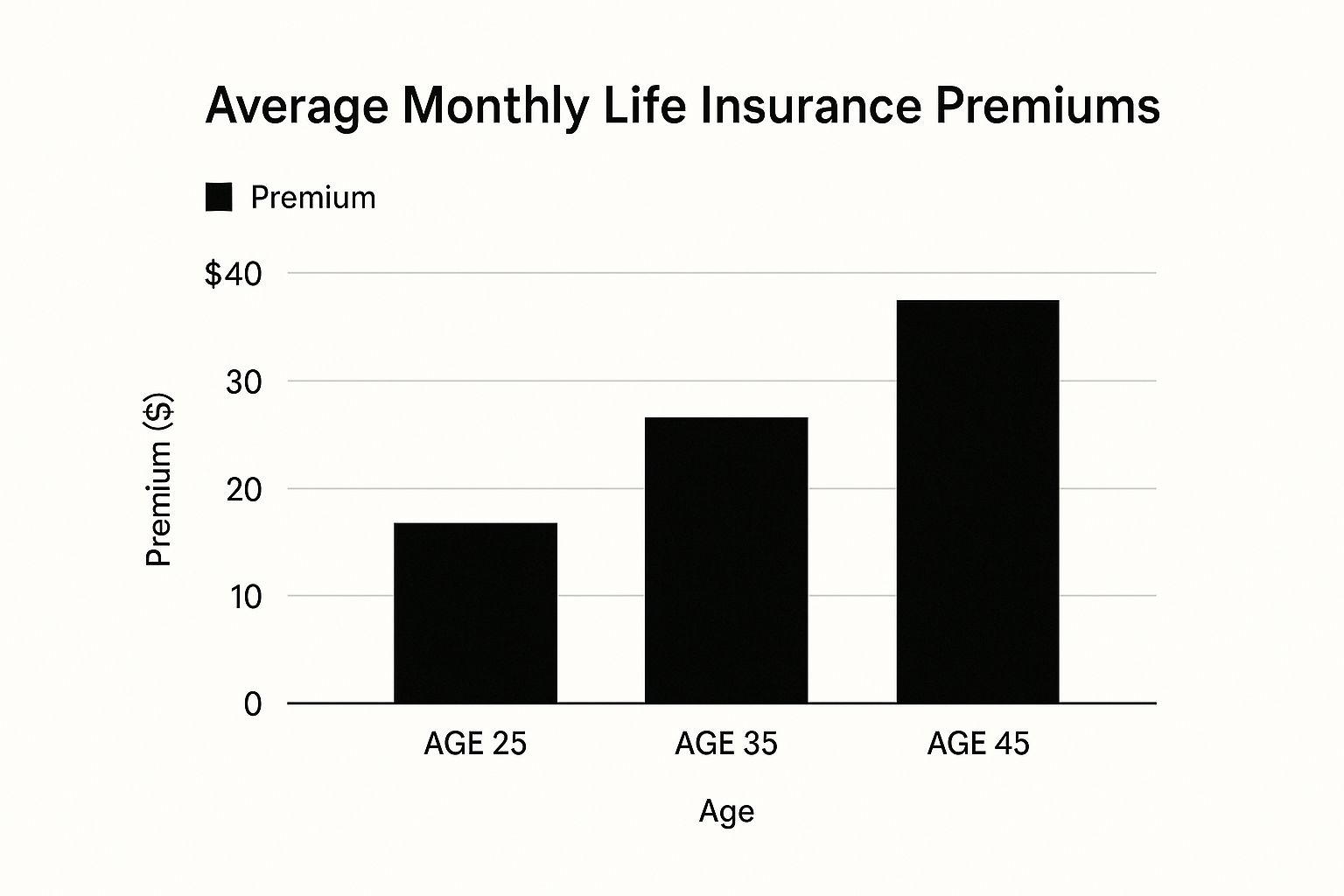

The infographic above illustrates average monthly life insurance premiums at different ages, showing how costs tend to rise as you get older. A 25-year-old can expect to pay around $15 per month, while a 45-year-old might pay closer to $40. This underscores the benefit of securing life insurance earlier in life when it’s more affordable.

To help you compare options, we've created a table summarizing the key differences between common life insurance types for singles:

| Life Insurance Types Comparison for Singles |

|---|

| Insurance Type |

| — |

| Term Life Insurance |

| Permanent Life Insurance |

| Group Life Insurance |

As you can see, each type of life insurance has its own advantages and disadvantages. Choosing the best policy for your situation requires careful consideration.

Choosing the right life insurance as a single person involves evaluating your individual needs, budget, and long-term goals. Factors such as your age, health, financial obligations, and dependents play a crucial role in this decision. By understanding the different types of coverage available and comparing costs, you can find a policy that offers adequate protection without overspending.

Calculating Your Perfect Coverage Amount Without Overpaying

Figuring out the right life insurance coverage as a single person is different than for families. This section provides formulas and tools designed for singles, whether you support others financially or are planning for your own future.

Analyzing Your Debt and Financial Obligations

Begin by assessing your debts. Make a list of all outstanding loans: student loans, mortgages, car loans, and credit card balances. Total these up to determine your overall debt burden. This is the first step in calculating necessary coverage to protect your estate.

Next, think about anticipated future financial obligations. This could include funeral expenses or contributing to a parent's care. While these costs can be difficult to estimate, they're important to consider. Adding these to your debt calculations provides a clearer understanding of your financial responsibilities. For more guidance from experts, check out our guide on how much life insurance you should buy.

Calculating Income Replacement for Dependents

If you have dependents, determine the amount of income replacement they'd need if you were to pass away. Factor in their current living expenses, future education costs, and any ongoing care they might require. This calculation ensures their standard of living is maintained.

For example, if your child's annual expenses are $20,000 and you aim to provide for them until college graduation in 10 years, you'll need at least $200,000 in coverage. Keep in mind, this doesn't account for potential cost of living increases or unexpected expenses.

Planning for Future Financial Obligations

Look beyond immediate needs. Consider future goals like a house down payment, starting a business, or paying off future debts. These goals, while important, can add up to significant sums that should be included in your coverage calculations.

Also, consider your specific circumstances. If you have student loans, research forgiveness programs that could potentially lower your debt. If caring for aging parents, explore long-term care insurance options to supplement your life insurance coverage. Understanding these details leads to a more precise assessment of your needs.

Balancing Coverage with Affordability

The following table, "Singles Life Insurance Coverage Calculator," provides a practical breakdown of expenses and financial obligations singles should consider when determining their life insurance needs. Use this as a guide to organize your thoughts and gain a better understanding of your coverage amount:

| Expense Category | Typical Range | Your Amount | Priority Level | Notes |

|---|---|---|---|---|

| Funeral Expenses | $5,000 – $15,000 | High | ||

| Outstanding Debts | Varies | High | Include student loans, mortgages, etc. | |

| Income Replacement for Dependents | Varies | High | Calculate based on dependents' needs | |

| Future Financial Obligations | Varies | Medium | ||

| Parent Care | Varies | Medium | ||

| Other Expenses | Varies | Low |

By calculating your debts, future obligations, and potential income replacement needs, you can determine a coverage amount that offers sufficient protection without overspending. Finding the right balance is essential. Too little coverage can leave loved ones financially vulnerable, while excessive coverage can strain your budget.

Smart Strategies For Getting Quality Coverage On A Budget

Singles often face unique financial considerations, making affordable life insurance a priority. Securing quality coverage without overspending requires a strategic approach. This section explores proven methods from insurance professionals to maximize value and minimize costs.

Timing Your Application and Seeking Discounts

The timing of your life insurance application has a significant impact on your premiums. Applying while younger and healthier typically secures lower rates. Insurance companies assess risk based on age and health status, so even a few years can make a difference in your premium payments. Many insurers offer discounts, such as non-smoker discounts and preferred health discounts. Actively inquiring about these can further reduce your costs.

Navigating Agents vs. Direct Purchases

Choosing between an insurance agent and a direct purchase affects cost and convenience. Agents offer personalized guidance and compare policies from multiple insurers like State Farm. However, their commissions are often included in your premiums. Direct purchases through online platforms like Policygenius offer more control and potentially lower costs by eliminating the intermediary. Weigh the benefits of professional advice against potential premium increases to find the right balance.

Mastering Comparison Shopping and Premium Structuring

Effective comparison shopping is crucial for finding the best life insurance deal. Don't settle for the first quote. Obtain quotes from multiple insurers and compare coverage amounts, premiums, and policy features. Online comparison websites can streamline this process. How you structure premium payments also impacts overall costs. Paying annually often leads to lower premiums than monthly installments due to reduced administrative fees. Consider automating these payments to simplify budgeting. You might be interested in: How to master comparison shopping for lower life insurance premiums.

Choosing the Right Riders and Avoiding Costly Mistakes

Policy riders, additional features added to your policy, can enhance coverage but increase premiums. Carefully evaluate which riders truly benefit you. A waiver of premium rider, waiving premiums if you become disabled, might be valuable. Avoid unnecessary riders that inflate costs without providing significant benefits. Common mistakes like overestimating coverage needs or omitting relevant health information can also lead to unnecessary expenses. Accuracy in your application is essential.

Optimizing Medical Exams and Negotiating Strategies

Medical exams are often required for life insurance applications. Understanding how these exams affect premiums is helpful. Maintaining a healthy lifestyle beforehand can positively influence the results. Some insurers allow premium negotiation, particularly for larger policies. Don't hesitate to inquire about negotiation options to potentially secure a lower rate.

Final Thoughts on Cost-Effective Life Insurance

Finding affordable life insurance as a single person requires careful planning and research. Factors like your age, health, and chosen policy type influence your final premium. By following these strategies, you can make informed decisions and find a policy that provides adequate protection without straining your budget. Securing your financial future doesn't have to be expensive. The right approach can help you obtain valuable life insurance coverage at an affordable price.

Comments are closed.