Decoding the Deductible: What Insurers Don't Tell You

Let's face it, the term "deductible" can be confusing. It's a core part of any insurance policy, yet many policyholders don't fully understand what it means. This lack of understanding can lead to costly mistakes and unexpected expenses. This section aims to clarify the deductible definition that insurance companies often oversimplify. We'll explore how deductibles actually work and how they impact your coverage and your finances.

The True Purpose of a Deductible

A deductible is the amount you pay out-of-pocket before your insurance coverage begins. For instance, if you have a $500 deductible and a covered loss of $2,000, you pay the first $500. Your insurance company will cover the remaining $1,500. But the deductible's role goes beyond simple cost-sharing. It encourages policyholders to be more careful and avoid filing claims for minor incidents. Deductibles also allow insurance companies to manage risk and set premiums accordingly.

How Deductibles are Strategically Set

Insurance companies don't randomly choose deductible amounts. They use complex calculations to determine the right deductible levels for different policies. Factors such as past claim data, the type of coverage, and the insured's risk profile all play a role. A policy covering a high-risk property might have a higher deductible than a lower-risk property. Understanding the deductible definition insurance providers use internally—which can be different from the simplified version given to consumers—is critical. For a deeper dive, read our article about How to master the insurance deductible definition.

The Impact of Deductibles on Consumer Behavior

Deductibles greatly influence how consumers use their insurance. A high deductible often discourages people from filing small claims because they would have to pay the full cost up to the deductible. This can impact the overall cost of insurance. Speaking of costs, looking at insurance statistics can be informative. In 2020, the life and health insurance sector in the United States reached $945.6 billion. This highlights how important it is to understand deductibles within the larger insurance landscape. You can find more detailed statistics here: Insurance Statistics. Knowing how deductibles work is essential for making informed decisions about your insurance coverage.

Debunking Common Deductible Myths

There are several misconceptions about deductibles that can mislead consumers. One common myth is that all medical expenses apply to your deductible. However, some services, like preventive care, may be excluded. Another myth is that the lowest deductible is always the best choice. While a lower deductible means you pay less out-of-pocket when you file a claim, it usually comes with a higher premium. The key is finding the right balance between your deductible and premium. If you're just starting out with websites, a basic understanding of platforms like WordPress can be helpful. The best deductible for you depends on your individual needs and risk tolerance. You may find this helpful: How health insurance deductibles and out-of-pocket maximums work. Understanding these details is crucial for navigating the complexities of insurance and making sound financial decisions.

The Deductible Playbook: Mastering Different Policy Types

Not all deductibles are created equal. Understanding the deductible as it applies to insurance policies is crucial for making informed decisions about your coverage. This section breaks down how deductibles work across different insurance types, highlighting the nuances that can significantly impact your finances.

To help illustrate these concepts, we've included a data chart visualizing typical deductible ranges and how they are applied.

Health Insurance Deductibles

In health insurance, your deductible is the amount you pay out-of-pocket for covered healthcare services before your insurance company begins to pay. This can include doctor visits, hospital stays, and prescription drugs. For example, if your health insurance deductible is $1,000, you'll pay that amount before your insurance company starts covering expenses.

Deductibles significantly affect both the policyholder's financial burden and the cost structure of insurance plans. For instance, in 2023, the average annual family deductible for small companies was $5,074, while large companies averaged $3,547. This difference highlights the negotiating power of larger companies in securing lower deductibles for their employees. Explore this topic further: Trends in Employer Health Insurance Costs. Understanding these variations is crucial for managing your healthcare costs.

Auto Insurance Deductibles

Auto insurance deductibles apply when you file a claim for damage to your vehicle. There are two main types: collision and comprehensive. A collision deductible covers damage from accidents. A comprehensive deductible covers damage from other events, such as theft, vandalism, or natural disasters.

The amount you choose for your deductible will affect your premium. A higher deductible typically means a lower premium, but you'll have to pay more out-of-pocket if you file a claim.

Home Insurance Deductibles

Similar to auto insurance, home insurance deductibles also come into play when you file a claim. They typically apply to damage from covered perils like fire, windstorms, or theft. Certain events, like floods or earthquakes, may require separate policies with their own deductibles. Your home insurance deductible is the amount you are responsible for paying before your insurance coverage begins.

Business Insurance Deductibles

Business insurance deductibles function similarly to other types of insurance, requiring a business owner to pay a specific amount before the insurance coverage starts. The specific deductible type and amount can vary widely depending on the type of business insurance, the size of the business, and the specific risks covered. Business owners should carefully consider their deductible options to balance premium costs with their ability to handle potential losses.

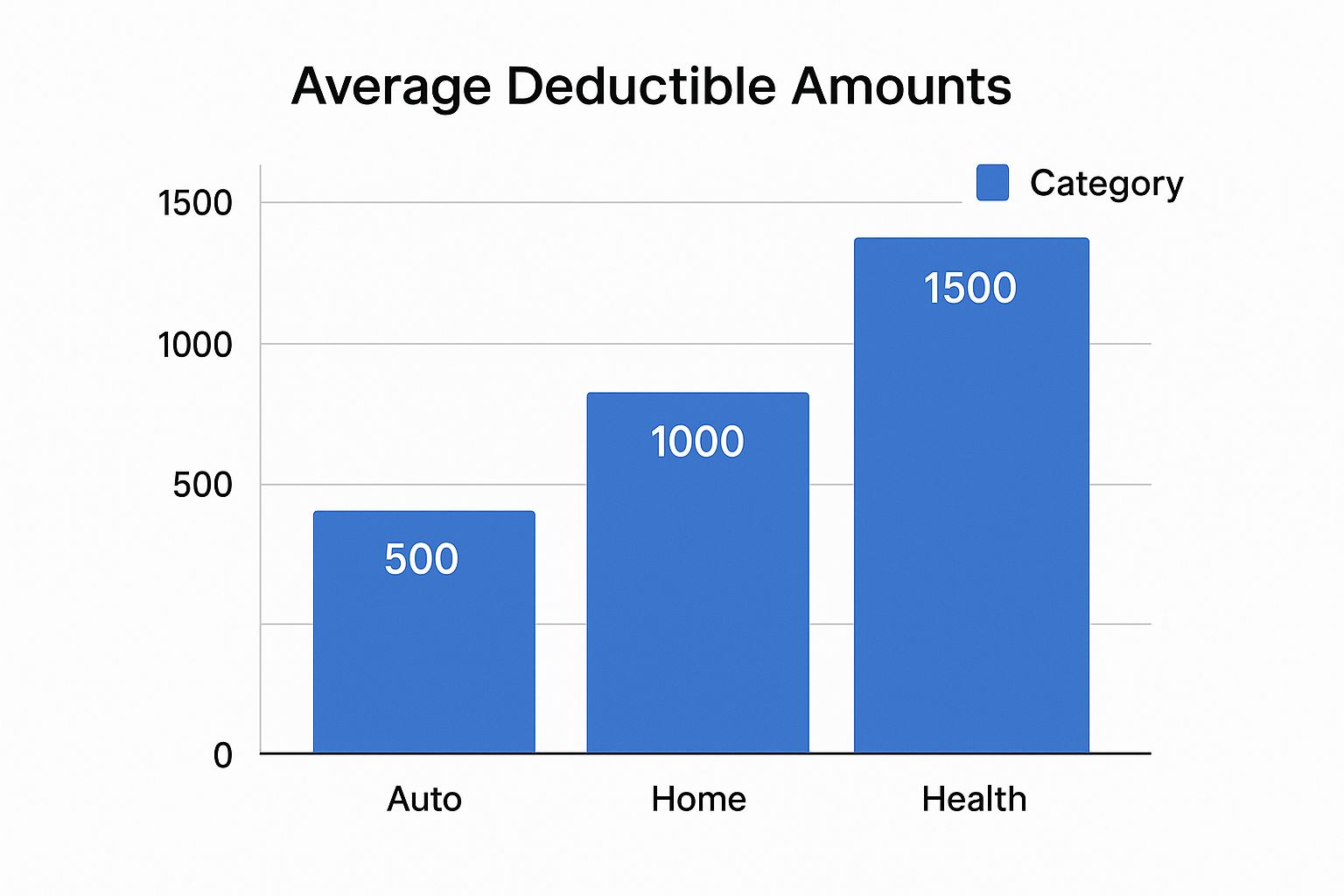

Visualizing Deductible Differences

The following data chart illustrates the typical deductible ranges and how they are applied across different insurance types:

[Infographic will be placed here]

- Health Insurance: $500 – $5,000+ (applied annually to covered medical expenses)

- Auto Insurance: $250 – $1,000+ (applied per incident for collision and comprehensive claims)

- Home Insurance: $500 – $2,000+ (applied per incident for covered perils)

- Business Insurance: Varies widely (applied per incident or annually depending on the policy)

This chart reveals that health insurance deductibles tend to have the widest range, possibly reflecting the variability in healthcare costs. Auto and home insurance deductibles are generally lower. The chart also emphasizes the importance of “per-incident” versus “annual” deductible application.

The following table provides further details on deductible types across major insurance policies:

Deductible Types Across Major Insurance Policies

A comparison of how deductibles work across different types of insurance policies.

| Insurance Type | Typical Deductible Range | How Applied | Special Considerations |

|---|---|---|---|

| Health Insurance | $500 – $5,000+ | Annually to covered medical expenses | Family plans often have higher deductibles than individual plans. |

| Auto Insurance | $250 – $1,000+ | Per incident for collision and comprehensive claims | Higher deductibles usually result in lower premiums. |

| Home Insurance | $500 – $2,000+ | Per incident for covered perils | Separate deductibles may apply for events like floods or earthquakes. |

| Business Insurance | Varies widely | Per incident or annually depending on the policy | Deductible amounts and application vary based on the specific type of business insurance. |

This table summarizes key differences in how deductibles are applied across different insurance types, allowing for a quicker comparison of typical ranges and special considerations. Understanding these nuances helps individuals and businesses make informed decisions about their insurance coverage.

The Premium-Deductible Balancing Act: Finding Your Sweet Spot

We've explored different deductible types across various insurance policies. Now, let's examine the crucial relationship between your premium and your deductible—a balancing act with a significant impact on your financial well-being. The common advice of "high deductible means low premium" is an oversimplification. There's a more nuanced financial picture to consider.

Calculating Your Financial Exposure

To truly grasp deductible definition insurance, we must understand actual financial exposure. Different deductible scenarios have different financial impacts.

For example, consider two scenarios: a $500 deductible with a $100 monthly premium versus a $2,000 deductible with a $50 monthly premium. The higher deductible initially seems attractive due to the lower premium. However, factor in potential out-of-pocket expenses in a claim, and this changes things.

You might be interested in: How to Master the Difference Between Health Insurance Deductible vs. Out-of-Pocket Maximum. This offers valuable insights into how out-of-pocket maximums affect healthcare costs.

The Tipping Point: When High Deductibles Don’t Make Sense

There's a point where higher deductibles no longer offer financial advantages. This “tipping point” hinges on your personal risk assessment. Factors include your financial stability, the likelihood of filing a claim, and potential claim costs.

A higher deductible might suit someone with a substantial emergency fund. However, for those living paycheck to paycheck, a lower deductible could offer essential financial protection.

How Actuaries Set Premiums and Deductibles

Insurance companies use actuaries—experts in assessing and managing risk—to develop premium-deductible relationships. They analyze significant amounts of data to calculate claim probability and associated costs.

Globally, the insurance market sees constant shifts. Factors such as economic conditions and claim payments influence insurance costs, including deductibles. The OECD's 2024 Global Insurance Market Trends report highlights how larger claims in 2022 led to 2023 price increases. This demonstrates how external forces affect your insurance. You can find more detailed statistics here: Global Insurance Market Trends 2024.

Real-World Examples and Life Circumstances

Life circumstances greatly influence the ideal deductible-premium balance. A young, healthy individual might prefer a lower premium with a higher deductible. A family with young children or someone with pre-existing conditions might prioritize a lower deductible and accept a higher premium.

Financial advisors often use email marketing to educate clients. Understanding your financial situation is key to informed decisions. Choosing the right deductible protects your financial well-being and ensures adequate coverage when needed.

Strategic Deductible Selection: Beyond Basic Calculations

Choosing the right deductible is a crucial aspect of managing insurance costs. It's more than just a simple calculation; it's a strategic decision that should reflect your personal financial situation and how comfortable you are with risk. This section explores how to make informed decisions about deductibles, going beyond basic premium comparisons.

Evaluating Deductibles Based on Your Financial Profile

Smart financial planning involves selecting a deductible that aligns with your overall financial well-being. This means considering more than just your current income. Factors such as the strength of your emergency fund, potential future healthcare needs, consistency of cash flow, and your personal comfort level with financial risk all play a role.

A healthy emergency fund, for example, can act as a safety net, allowing you to comfortably choose a higher deductible and enjoy lower premiums. Conversely, if your savings are limited, a lower deductible might be a better choice to minimize the financial impact of unexpected events.

Understanding Your Risk Tolerance and Financial Behavior

Your financial habits can offer valuable insights into which deductible level is right for you. Are you a diligent saver who tracks expenses carefully? This could suggest a higher comfort level with risk and the ability to handle a higher deductible. However, if unexpected costs often disrupt your budget, a lower deductible may offer greater peace of mind.

Leveraging Health Savings Accounts (HSAs)

If you're considering a high-deductible health plan (HDHP), Health Savings Accounts (HSAs) can be a valuable asset. HSAs offer triple tax advantages: contributions are tax-deductible, the earnings grow tax-free, and withdrawals for eligible medical expenses are also tax-free. These advantages can significantly offset the higher out-of-pocket costs associated with an HDHP. Strategically using an HSA can potentially lower your overall healthcare expenses while also allowing you to benefit from lower premiums.

A Framework for Strategic Deductible Decisions

To help you choose the right deductible, consider the framework below. It provides a data-driven approach to guide your decision-making process based on your individual financial circumstances.

Deductible Decision Framework

A data-driven approach to choosing the right deductible amount based on financial circumstances.

| Financial Situation | Risk Tolerance | Recommended Deductible Range | Key Considerations |

|---|---|---|---|

| Strong emergency fund, stable income | High | Higher end of the range | Potential for lower premiums and long-term savings |

| Limited savings, fluctuating income | Low | Lower end of the range | Protection against large out-of-pocket expenses |

| Moderate savings, stable income | Moderate | Middle of the range | Balance between premium savings and risk protection |

| Anticipating high medical expenses | Low | Lower end of the range | Minimize out-of-pocket costs for healthcare |

| Healthy lifestyle, minimal medical history | High | Higher end of the range | Lower premiums may be more cost-effective |

This framework is a starting point. The "right" deductible is a personal choice based on your unique situation. Speaking with a financial advisor can provide further guidance in aligning your deductible definition insurance choices with your overall financial plan.

Deductible Myths That Cost You: Separating Fact From Fiction

The insurance industry can be complex, and deductibles are a prime example. This section aims to clarify common misconceptions about insurance deductibles, empowering you to make informed choices and avoid unexpected costs. Understanding the deductible definition insurance companies use is the first step toward managing your insurance expenses.

Myth 1: All Medical Expenses Count Toward Your Deductible

Many assume every medical expense contributes to their deductible. This isn't always the case. Some plans don't include certain services, such as preventive care or out-of-network treatments. For example, annual checkups or vaccinations might be covered entirely before you meet your deductible.

This applies to other insurance types as well. Not all covered expenses necessarily count toward your deductible. Certain expenses might have different cost-sharing within the deductible definition outlined in your policy. Carefully review your policy documents to understand which expenses apply to your deductible. This is particularly important for those with high-deductible health plans.

Myth 2: The Lowest Deductible Is Always Best

Choosing the lowest deductible seems logical to minimize out-of-pocket expenses after a claim. However, lower deductibles often come with higher premiums. This can be more expensive over time, especially if you rarely file claims.

Consider the potential premium savings of a higher deductible against the risk of greater out-of-pocket costs if you need to make a claim. Evaluate your health history, expected medical needs, and financial situation. A healthy individual with solid finances might benefit from a higher deductible and lower premium.

Myth 3: Deductibles Are Never Waived

While deductibles are standard in most insurance policies, they can be waived under certain circumstances. Some policies waive deductibles for specific services, like certain preventive care. In other cases, insurers might waive deductibles after catastrophic events or for specific policyholders.

These waivers are not guaranteed and depend on the policy and the circumstances of the loss. For instance, some insurers might waive deductibles after a natural disaster to help affected policyholders. Review your policy or contact your insurer to understand the conditions under which your deductible might be waived.

Myth 4: Tornadoes During Hurricanes Always Fall Under the Hurricane Deductible

Deductibles can be confusing, even in specific situations like tornadoes during hurricanes. Many assume a higher hurricane deductible automatically applies to all damage during a hurricane. However, the reality depends on your policy's specific language.

As discussed in a blog post about tornado damage during hurricanes, some policies define "hurricane windstorm" to include tornadoes, even outside hurricane-force wind areas. This means a higher hurricane deductible might apply even if a tornado hits your property outside the main hurricane impact zone.

By understanding deductibles and dispelling these common myths, you can make more informed insurance decisions. This knowledge helps you choose plans that meet your needs and budget, maximizing your financial protection.

Advanced Deductible Strategies: Techniques For Sophisticated Consumers

For those looking to truly optimize their insurance coverage, understanding advanced deductible strategies is essential. These strategies can offer significant advantages when properly applied, providing both cost savings and enhanced protection.

Disappearing Deductibles and Claim-Free Rewards

One innovative approach is the disappearing deductible. This type of deductible decreases over time, often rewarding policyholders for claim-free periods. For example, your deductible might decrease by $100 each year you don't file a claim, eventually disappearing altogether.

This incentivizes responsible behavior and can lead to substantial long-term savings. This strategy is becoming increasingly popular in auto insurance policies, but is also being adopted in other areas like homeowners insurance.

You might be interested in: Demystifying Homeowners Insurance: Understanding Your Coverage.

Deductible Carry-Over and Year-End Spending

Some policies offer a deductible carry-over provision. This allows you to apply any amount you paid toward your deductible at the end of the year to the next year's deductible. This is particularly relevant for health insurance.

For example, if you have a $1,000 deductible and pay $700 toward it by December, the remaining $300 might be applied to the next year, giving you a head start on meeting your deductible. This can be advantageous for those anticipating significant medical expenses at the beginning of the following year, allowing you to maximize your medical spending and minimize your out-of-pocket costs.

Family Aggregate Deductibles: Enhanced Household Protection

Families may benefit from a family aggregate deductible. This type of deductible applies to the combined expenses of all family members covered under the policy. Instead of each individual meeting their own deductible, the family as a whole works toward a single deductible.

For instance, a family with a $2,000 aggregate deductible will receive coverage once the combined out-of-pocket expenses of all family members reach $2,000, regardless of which family member incurred the expenses. This offers greater financial protection, especially for families with multiple members likely to need medical care in a given year.

Evaluating Specialized Deductible Structures

It's important to carefully evaluate whether specialized deductible structures genuinely provide value or merely mask higher overall costs. Compare plans not only based on deductible amounts, but also on premiums, co-pays, and out-of-pocket maximums. A seemingly attractive disappearing deductible might come with significantly higher premiums that negate the potential savings.

Negotiating Favorable Deductible Terms

Don't be afraid to negotiate deductible terms, especially with commercial policies where greater flexibility often exists. By presenting a strong case based on your claims history and risk profile, you might be able to secure a more favorable deductible, potentially lowering your costs without sacrificing coverage.

Cost-Benefit Analysis of Complex Deductible Provisions

Conducting a thorough cost-benefit analysis can be challenging, particularly when comparing complex deductible provisions across different policy types. Consider creating a spreadsheet to compare different scenarios. Input potential claim costs and premiums for various plans, calculating your total potential out-of-pocket expenses under each. This will help you identify opportunities for substantial savings.

By understanding and strategically applying these advanced deductible strategies, you can make informed decisions about your insurance coverage. This knowledge empowers you to optimize your insurance protection and maximize your financial well-being. The key is finding the right balance between premium costs and potential out-of-pocket expenses, a balance tailored to your individual or family needs and financial circumstances.

Comments are closed.