Demystifying Coordination of Benefits Rules: What You Need to Know

Navigating the world of Coordination of Benefits (COB) rules can be confusing. These rules are designed to ensure you receive the full benefits you're entitled to when covered by multiple insurance plans, but prevent overpayment. Essentially, if you have two or more insurance plans, they work together to cover your medical costs, up to 100% of the total expense. Understanding COB rules can make your claims process smooth and efficient.

Understanding the Basics of Coordination of Benefits

The fundamental principle of COB is determining which plan is primary and which is secondary. The primary insurance pays first, up to its coverage limit. For instance, if your primary plan covers 80% of a $1,000 medical bill, it will pay $800. The remaining $200 is then the responsibility of your secondary insurance. This process ensures no more than the total cost of the service is reimbursed.

COB in the United States poses significant administrative hurdles, especially within the healthcare industry. Inefficiencies in managing multiple health insurance plans lead to substantial administrative costs, estimated to exceed $800 million annually. The COB process is essential for avoiding overpayments and ensuring accurate claim processing. For more detailed statistics, you can refer to this resource: https://www.caqh.org/sites/default/files/solutions/cob-smart/COBwhitepaper.pdf Regularly reviewing your insurance coverage can help avoid unnecessary overlap. You can find helpful updates at Product Updates.

Common Scenarios and Determining Coverage Priority

Several factors influence which plan is considered primary. These can include your employment status, the relationship between policyholders (such as spouse or parent-child), and the type of coverage (medical, dental, or vision). The “birthday rule” often determines primary coverage for children of married parents. The parent whose birthday is earlier in the year holds the primary plan. For children of divorced parents, the custodial parent's plan typically has precedence.

- Employed vs. Retired/Laid Off: If you're covered by a former employer and another insurance source, the former employer's plan is typically primary.

- Two Jobs with Insurance: The insurance plan you enrolled in first generally acts as your primary coverage.

- Spousal Coverage: Each spouse’s employer-sponsored plan is generally considered primary for that individual.

- Medicare vs. Retiree Plan: Generally, before age 65, the retiree plan is primary; after 65, Medicare becomes primary.

Why Coordination of Benefits Matters

Effective COB ensures you maximize your coverage and minimize your out-of-pocket expenses. This involves understanding how your deductibles, copayments, and out-of-pocket maximums interact between plans. Without proper coordination, you could end up paying more than necessary or experience delays in claim processing. Understanding these rules can save you time, money, and stress. It can also help you avoid claim denials due to incorrect submission order. Knowing your primary and secondary insurance allows you to navigate the claims process smoothly and efficiently.

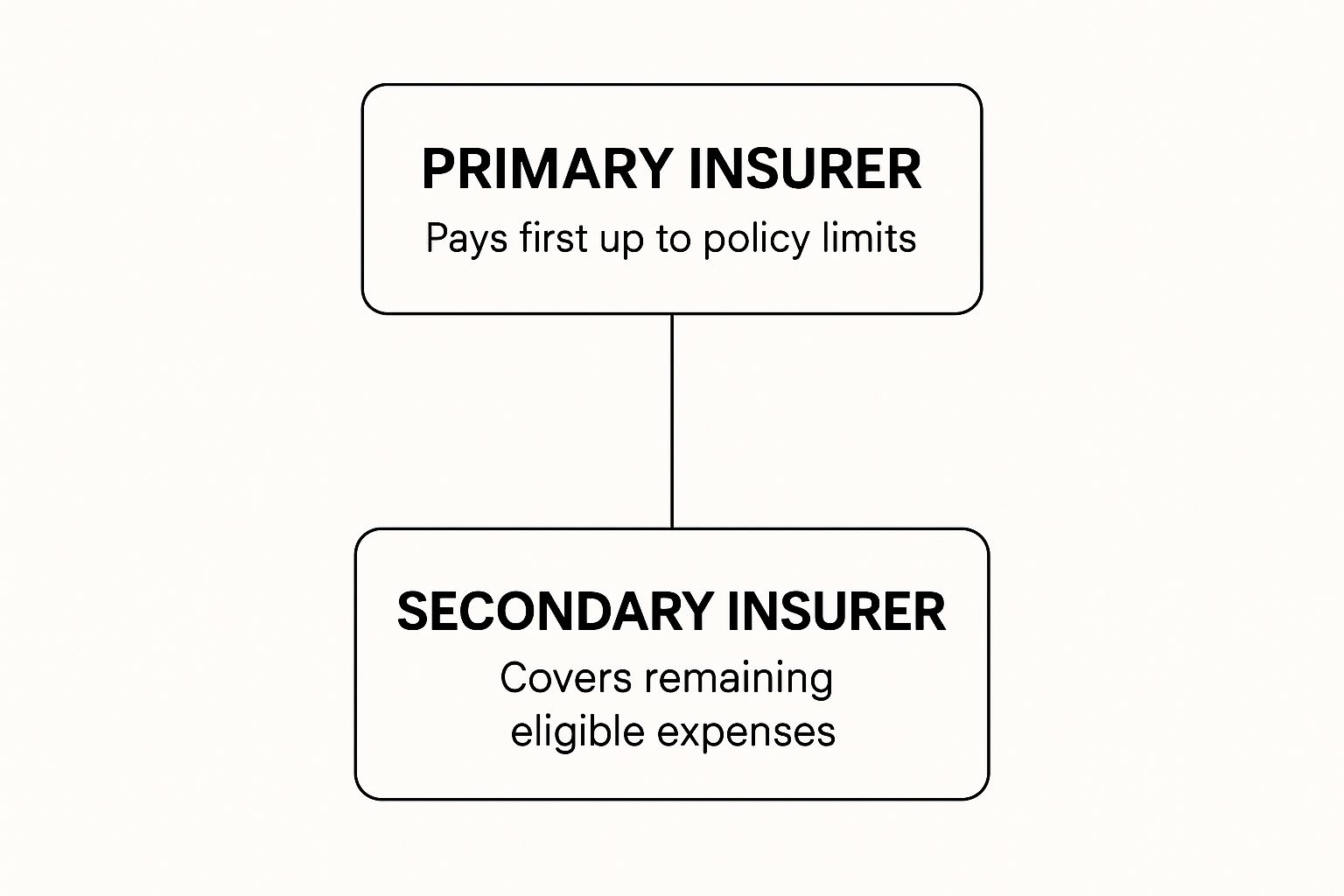

Primary vs. Secondary Coverage: Who Pays First and Why It Matters

This infographic illustrates how payment responsibility is structured when coordination of benefits (COB) rules are applied. The primary insurer pays first, up to their policy's limits. The secondary insurer covers remaining eligible expenses only after the primary insurer's obligation is met.

Decoding the Primary Insurer

Several factors determine which plan is primary. This is the foundation of COB rules. For instance, if you have employer-sponsored coverage and coverage under your spouse's plan, your employer's plan is typically primary.

However, with coverage from a former and current employer, the former employer's plan usually pays first. This also applies to those with continued coverage through COBRA.

Navigating Secondary Coverage

Secondary insurance begins paying after the primary insurer has met its responsibility. This helps minimize your out-of-pocket expenses. Secondary coverage doesn't duplicate benefits; it supplements them. Combined payments from both plans won't exceed the total cost of your medical expenses, preventing "double-dipping." Businesses are constantly looking for ways to improve verification processes, such as how Pazcare streamlined Background Verification.

The Birthday Rule and Other Scenarios

COB rules become more nuanced with children, especially in cases of divorced or separated parents. The birthday rule often applies: the parent whose birthday is earlier in the year typically has the primary plan.

Additionally, Medicare, Medicaid, and retiree plans have specific COB rules impacting which plan is primary and each plan's contribution.

To understand the hierarchy further, let's take a look at the table below:

Primary vs. Secondary Insurance Determination Hierarchy

This table outlines the standard order of benefit determination for various common scenarios when individuals have multiple insurance plans.

| Scenario | Primary Coverage | Secondary Coverage | Special Considerations |

|---|---|---|---|

| Employed with Spouse's Coverage | Your Employer's Plan | Spouse's Plan | |

| Employed with Former Employer's Coverage | Former Employer's Plan (e.g., COBRA) | Current Employer's Plan | COBRA continuation coverage typically considered primary. |

| Child of Divorced/Separated Parents | Parent with earlier birthday in the calendar year | Parent with later birthday in the calendar year | This is the "Birthday Rule." Exceptions may apply. |

| Medicare and Employer-Sponsored Retiree Plan | Employer-Sponsored Retiree Plan | Medicare | Specific rules govern coordination between Medicare and retiree plans. |

This table highlights common scenarios and how primary/secondary coverage is typically determined. However, individual plan details and specific circumstances can impact these determinations.

The Importance of Understanding Coordination

Understanding COB rules is crucial for managing your healthcare finances. It affects your deductibles, copayments, and out-of-pocket maximums. A high-deductible primary plan might mean more out-of-pocket spending before secondary coverage activates.

Knowing your plan coordination helps you budget for medical expenses and avoids unexpected costs. It can also prevent claim denials and ensure faster processing, reducing stress and providing timely access to care. Understanding primary and secondary coverage equips you to navigate the healthcare system and maximize your insurance benefits.

The Healthcare Coordination Maze: Preventing Coverage Nightmares

Healthcare claim processing can be a confusing experience, especially when multiple insurance plans are involved. This is where coordination of benefits (COB) comes in. This section explains how COB works and why it’s so important for managing your healthcare costs.

The Claim's Journey Through Coordination

When you submit a medical claim, your provider first sends it to your primary insurer. This plan processes the claim according to your benefits and pays its portion. The remaining balance, if any, is then sent to your secondary insurer. This coordinated system ensures you receive the maximum coverage allowed by your plans. However, problems can arise if the information provided is inaccurate or if the insurance plans disagree about their respective responsibilities.

Insider Tips for Smooth Claim Processing

Providing accurate information upfront is crucial for efficient claim processing. This includes double-checking policy numbers, subscriber information, and details about other coverage you may have. Billing specialists and claims adjusters emphasize proactive communication with both insurers. For example, notifying them of a pending claim involving multiple plans can help expedite processing and avoid potential delays.

Coordination's Impact on Your Finances

Coordination of benefits directly affects your out-of-pocket expenses. If your primary plan has a high deductible, for instance, you might have higher upfront costs before your secondary coverage begins paying. Coordination of benefits also influences how copayments and out-of-pocket maximums are applied across your plans. Understanding these interactions is essential for managing your healthcare budget effectively. In essence, understanding COB is not just about maximizing coverage; it’s a crucial part of financial planning. For more guidance on choosing the right plan, check out this helpful resource: Navigating the Health Insurance Maze: Tips to Choose the Right Plan for You.

Proactive Steps to Maximize Your Benefits

Taking proactive steps can help you avoid potential issues with COB. This includes maintaining accurate records of all your insurance policies and familiarizing yourself with each plan's specific rules. Directly verifying COB rules with your insurers is also recommended to avoid any surprises. These steps ensure you're getting the most out of your benefits when you have multiple insurance plans. It’s important to remember that COB isn't limited to healthcare. It also plays a role in the broader context of social security. The European Commission has proposed a revision of EU legislation on social security coordination, aiming to better protect EU citizens moving between countries. You can learn more about this here: EU Social Security Coordination. Staying informed about the wider implications of COB can help you confidently navigate the complexities of insurance. Being proactive and informed empowers you to manage your healthcare coverage and avoid unnecessary financial strain.

Global Benefit Navigation: Coordination Of Benefits Rules Abroad

Understanding how coordination of benefits (COB) works in your home country can be tricky. Add living, working, or retiring abroad to the mix, and navigating healthcare coverage gets even more complicated. This section explores the complexities of international COB, focusing on how different systems interact to ensure you receive the coverage you're entitled to.

Coverage Priority In Different Countries

Figuring out which insurance plan takes precedence when you have multiple plans in different countries isn't always straightforward. Numerous factors influence this, including each country's specific regulations, the type of insurance (public or private), and any applicable international agreements. Some countries, for example, prioritize the plan of the country providing the medical services, while others prioritize the plan of the individual's primary residence. Knowing the specifics of each country involved is crucial for smooth claims processing.

To help clarify the diverse approaches to cross-border benefit coordination, the following table provides a regional comparison:

Cross-Border Benefit Coordination by Region

This table compares how different international regions handle coordination of benefits across borders, showing key regulations and coverage types.

| Region/Agreement | Key Regulations | Benefits Covered | Documentation Required | Limitations |

|---|---|---|---|---|

| European Union | EU Regulations 883/2004 and 987/2009 | Healthcare, Pensions, Family Benefits, Unemployment Benefits | Portable Document A1, Proof of Insurance, Passport/ID | Variations in national implementation |

| Other International Agreements (e.g., bilateral agreements) | Varies by Agreement | Specific to the agreement, often focusing on healthcare | Varies by Agreement, typically includes proof of insurance and identity documents | Limited scope, may not cover all situations |

| No Agreement | National laws of each country involved | Highly variable, may not recognize foreign insurance | Proof of Insurance, Passport/ID, potentially additional documentation depending on local regulations | Complex, potential for denied claims and significant out-of-pocket costs |

This table illustrates the various factors that influence international benefit coordination. While agreements like those within the EU provide a framework, variations exist. Situations where no agreement exists can be particularly challenging, emphasizing the importance of understanding local regulations.

Essential Documentation For International Care

Before receiving medical care abroad, gathering the necessary paperwork is essential. This usually includes proof of insurance from all plans, passport or other identification, and possibly pre-authorization forms depending on the treatment and countries involved. Keeping detailed records of all medical expenses, such as receipts and itemized bills, is crucial for reimbursements. Without proper documentation, claims can be delayed or denied, leading to unexpected expenses.

International Agreements And Your Benefits

Several international agreements simplify cross-border benefit coordination. A prime example is the European Union. The EU's coordination of social security systems helps citizens moving between member states retain access to healthcare, pensions, family benefits, and unemployment benefits. This system operates under regulations like EU 883/2004 and 987/2009, updated in May 2010. The issuance of Portable Document A1 (for those working in multiple or posted to other EU states) has more than tripled in the last decade, reaching about 4.6 million in 2022. EU Social Security Coordination Statistics offer more details. While these agreements streamline access for those moving between participating countries, understanding the specific procedures remains essential.

Real-World Scenarios: Successes And Failures

Real-world examples illustrate the practical side of international COB. Consider an expatriate working in one country but insured in their home country. They might encounter difficulties coordinating claims, such as different forms, language barriers, and varying coverage. However, careful planning and communication with both insurers can greatly improve the process. Conversely, lack of preparation can lead to denials and financial strain. Understanding potential problems and preparing accordingly is vital.

Strategies For Navigating Multiple Systems

Successfully handling multiple healthcare systems requires a proactive, informed approach. Here are some key strategies:

-

Understand Your Policies: Review all your insurance policies, noting coverage limits, exclusions, and international claims procedures.

-

Contact Your Insurers: Speak with your providers before travelling or seeking care abroad to clarify their international claims processes and required documents.

-

Maintain Detailed Records: Keep organized records of all medical expenses, including receipts, bills, and insurance communications for potential appeals or disputes.

-

Seek Expert Advice: Consider consulting with a specialist in international insurance or a patient advocate if you face challenges navigating international COB rules. They can provide valuable guidance and support.

By using these strategies, individuals living, working, or travelling internationally can minimize potential problems and ensure access to their deserved healthcare coverage. The complexities of international COB require careful planning and informed decisions.

Breaking Through Coordination of Benefits Roadblocks: Solutions That Work

When coordination of benefits (COB) rules go wrong, it can impact both your finances and your peace of mind. This section addresses common coordination challenges, providing practical solutions based on real-world resolutions. We'll delve into why disagreements about primary/secondary payer status arise and empower you to navigate these situations effectively.

Common Disputes and Resolutions

One frequent issue is insurers disagreeing on which plan is primary. This can occur due to discrepancies in reported information, differing interpretations of coordination rules, or simple administrative errors. For example, if your employer's plan and your spouse's plan both consider themselves primary, you might face delays in claim processing while they resolve the conflict. In these situations, clear communication and documentation are key.

The COB process involves determining which health plan is primary and which is secondary when a person has multiple insurance plans. This process is crucial for avoiding overpayment and ensuring proper claim processing. However, the complexity increases with the involvement of various payers, including commercial, government-sponsored, workers’ compensation, and auto coverage. The Affordable Care Act (ACA) reforms have the potential to expand coverage, thereby increasing instances where COB is necessary, adding to the complexity of the existing system. Explore this topic further: Coordination of Benefits Research

Effective Communication and Documentation

When dealing with unresponsive claims departments, use clear, concise language, documenting every interaction. Keep records of dates, times, names of representatives, and reference numbers. This paper trail becomes essential when escalating the issue.

Additionally, provide copies of both insurance cards and any relevant Explanation of Benefits (EOB) statements. These documents help establish the facts of your case and can expedite the resolution process.

Appealing Incorrect Determinations

If you believe a coordination determination is incorrect, you have the right to appeal. This often involves writing a formal appeal letter outlining the discrepancy and providing supporting documentation. For instance, if your secondary insurance incorrectly denies a claim because they believe the primary insurance should have paid more, you would appeal with evidence of the primary insurance's payment and its coordination rules.

Escalating Issues and Seeking Assistance

Sometimes, internal appeals are insufficient. In these cases, escalating the issue to your state's insurance department or seeking assistance from a patient advocate might be necessary. These external resources can provide guidance and intervene on your behalf.

Technological Solutions and Vulnerable Populations

Technology is simplifying coordination of benefits. Electronic data interchange (EDI) between insurers allows for faster, more accurate information sharing. However, vulnerable populations, such as those with limited technological access or language barriers, may face unique challenges. Addressing these disparities is crucial to ensure everyone benefits from coordinated coverage. You might be interested in: The Ultimate Guide to Choosing the Right Home Insurance Policy in 2025.

Steps for Resolving COB Issues

Here's a step-by-step approach to resolving COB problems:

- Gather Your Information: Collect all relevant insurance cards, policy documents, and EOBs.

- Contact Your Insurers: Communicate clearly with both insurers, documenting each interaction.

- File an Appeal: If necessary, submit a formal appeal letter with supporting evidence.

- Escalate if Needed: Contact your state's insurance department or a patient advocate if the issue persists.

By understanding your rights and taking proactive steps, you can overcome coordination roadblocks and ensure you receive the full benefits you deserve. Effective COB management is essential for maximizing your coverage and minimizing financial stress.

The Future of Coordination of Benefits Rules: What's Coming Next

The insurance industry is in constant flux, and coordination of benefits (COB) rules are no different. This section explores emerging trends and technological advancements set to reshape how these rules operate, impacting both insurers and policyholders. By understanding these upcoming changes, you can ensure a smoother experience in the future.

The Impact of Digital Transformation

Digital transformation is already simplifying complex insurance processes. This includes automating claim submissions, digitizing medical records, and enhancing communication between payers. These improvements can result in faster processing and fewer errors, benefiting both patients and insurance companies. For instance, automated systems can quickly verify coverage across multiple plans, minimizing manual data entry and reducing human error. This translates to quicker reimbursements and a less complicated process for everyone.

Standardization Efforts and Their Effects

Growing standardization across insurance providers is another key trend. While plan specifics will likely vary, standardization aims to simplify data exchange and coordination. This might involve adopting universal claim forms or standardized Electronic Data Interchange (EDI) formats. Improved interoperability will streamline coordination by facilitating communication between different systems.

The Rise of Value-Based Care and Coordination Requirements

Value-based care models are also influencing coordination of benefits rules. These models prioritize preventative care and positive health outcomes. Consequently, there's an increasing need for effective coordination between healthcare providers and insurance plans. This necessitates robust data sharing and clear communication to ensure patients receive the right care and avoid unnecessary or duplicate services.

Legislative Changes and Their Implications

Recent legislative changes in many areas are reshaping the COB landscape. These changes can impact eligibility, covered benefits, and coordination procedures. Keeping abreast of these updates is crucial for both insurers and consumers to maintain compliance and optimize benefits.

Cutting-Edge Solutions: Blockchain and AI

Technological innovations like blockchain verification and AI-powered determination are transforming coordination in some areas. Blockchain offers a secure and transparent method for verifying policy information and tracking claims, mitigating fraud and boosting efficiency. AI can automate the process of identifying primary and secondary payers, speeding up claim processing. While widespread adoption may take time, these technologies hold significant potential for streamlining COB.

Preparing for the Future of Coordination

How can you prepare for these evolving COB rules? Here are some strategies:

-

Stay Informed: Keep up with industry trends, legislative changes, and technological advancements.

-

Embrace Digital Tools: Use online portals and mobile apps to manage insurance information and track claims.

-

Communicate Proactively: Clearly communicate your coverage details to all healthcare providers and insurers.

-

Review Your Policies Regularly: Review your policies to ensure they meet your needs and understand any changes in coordination procedures. You might be interested in: 2025 Life Insurance Handbook: Expert Tips for Selecting the Best Policy for You.

-

Seek Professional Advice: Consult with an insurance professional if you have complex coverage or face coordination challenges.

By taking these proactive steps, you can navigate the changing landscape of coordination of benefits rules and ensure you receive the full coverage you're entitled to. The future of COB is moving toward increased efficiency, transparency, and patient empowerment. Embracing these changes will be essential for optimizing your healthcare experience and managing costs effectively.

Comments are closed.