Demystifying Car Insurance: Beyond the Monthly Premium

Understanding car insurance can seem complicated. It's much more than just a monthly payment; it's a vital safety net for your finances. This section breaks down the key parts of car insurance, explaining their meaning and importance. You'll learn the difference between simply having insurance and being truly protected. Want a quick primer on the basics? Check out this helpful resource: How to master car insurance basics.

Decoding Your Policy: Key Coverage Types Explained

Car insurance policies generally include several key coverage types, each designed for different situations. Let's explore the most common:

-

Liability Coverage: This covers damage you cause to others in an accident. It's split into bodily injury liability, which covers medical bills and lost wages, and property damage liability, covering repair or replacement of damaged property. Choosing enough coverage is critical, as too little can leave you personally responsible for remaining costs.

-

Collision Coverage: This covers damage to your own car from a collision with another vehicle or object, no matter who is at fault. It's key for protecting your car investment, particularly if it's newer or valuable.

-

Comprehensive Coverage: This covers damage to your vehicle from events other than collisions, such as theft, vandalism, fire, or natural disasters. If your car is stolen or damaged by a hailstorm, comprehensive coverage steps in.

For example, imagine your car is damaged in a hit-and-run. With only liability coverage, you're responsible for repairs. However, collision coverage means your insurer covers the damage. If a tree falls on your parked car, comprehensive coverage protects you. Getting the right insurance is crucial. For businesses, exploring business insurance is equally important.

Why Coverage Matters: Beyond Minimum Requirements

Many states require minimum liability coverage, but these often don't provide adequate protection. In a serious accident, minimum coverage may not be enough, leaving you financially exposed. Consider your assets and potential future earnings when deciding on coverage limits.

Furthermore, the car insurance industry is constantly changing. The global car insurance market is growing significantly, due to rising car ownership and new technologies. By 2025, the market is estimated at USD 973.33 billion, projected to reach USD 1,796.61 billion by 2034, a CAGR of 7.03%. This growth is largely driven by a growing middle class in emerging markets and technologies like artificial intelligence (AI), which improves efficiency and customer satisfaction. AI helps insurers streamline claim processing, reducing costs and improving accuracy. The North American market alone surpassed USD 309.57 billion in 2024, showing high demand. For more detailed statistics, see this report: Vehicle Insurance Market. Understanding these trends underscores the importance of proper car insurance coverage.

Liability Coverage: The Foundation That Protects Your Future

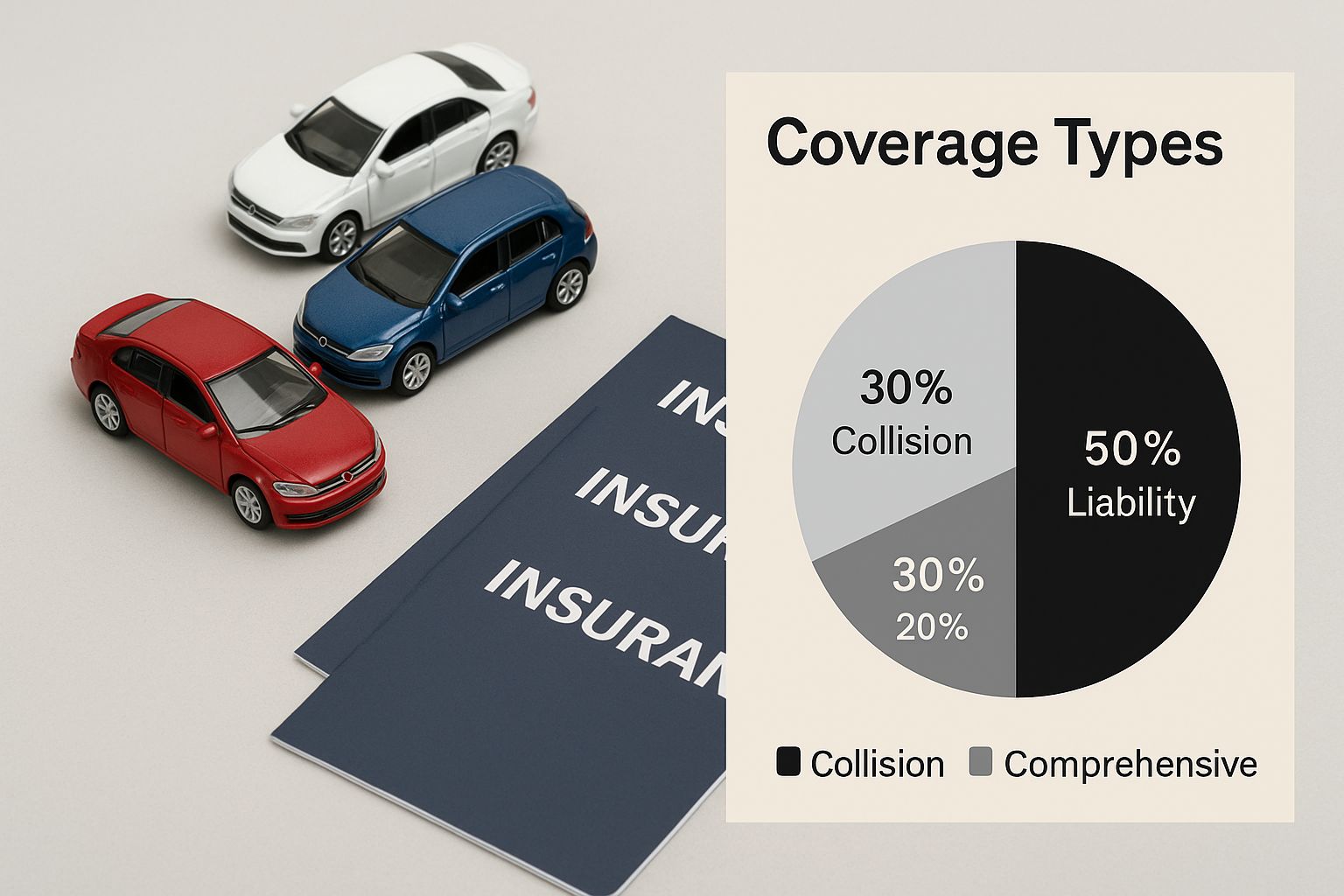

The infographic above illustrates the different types of car insurance coverage available. It uses toy cars and insurance booklets to represent the options, highlighting the importance of understanding your choices. This visual representation underscores the need to select the right coverage for your specific situation.

Understanding Bodily Injury and Property Damage Liability

Liability coverage forms the bedrock of any car insurance policy. This vital coverage protects you financially if you cause an accident that results in injury or property damage to others. It comprises two main parts: bodily injury liability and property damage liability. Bodily injury liability covers costs associated with injuries sustained by others in an accident you cause, such as medical expenses and lost wages.

For instance, if you are at fault and the other driver incurs significant medical bills, your bodily injury liability coverage would contribute towards these costs. Property damage liability, conversely, covers the expense of repairing or replacing someone else's property damaged in an accident you cause. This could include damage to their vehicle, a fence, or a building.

Imagine backing into a parked car; your property damage liability would cover the necessary repairs. Understanding both aspects of liability coverage is crucial for informed decision-making.

State Minimums vs. Adequate Protection: A Critical Distinction

Most states mandate minimum liability coverage levels. However, these minimums are often insufficient. While fulfilling the legal requirement to carry insurance, they may leave you vulnerable financially if a serious accident occurs. Medical and property damage costs can rapidly surpass these minimums, leaving you responsible for the difference.

Suppose you carry the state-required minimum of $25,000 for bodily injury liability and cause an accident resulting in $50,000 in medical expenses for the other party. You would be personally liable for the remaining $25,000. This highlights the importance of reviewing your coverage limits. Insurance professionals typically advise carrying higher limits to safeguard your assets and future income.

To help illustrate this point, let's take a look at the following comparison:

State Minimum Liability Requirements vs. Recommended Coverage

This table compares minimum state-required liability coverage amounts with expert-recommended coverage levels to demonstrate the protection gap many drivers face.

| Coverage Type | Average State Minimum | Recommended Minimum | Rationale for Higher Coverage |

|---|---|---|---|

| Bodily Injury Liability | $25,000/person, $50,000/accident | $100,000/person, $300,000/accident | Increased medical costs and potential lawsuits |

| Property Damage Liability | $25,000/accident | $100,000/accident | Higher vehicle repair/replacement costs and potential property damage |

As you can see, the recommended coverage significantly exceeds the average state minimums. This is due to several factors, including rising healthcare and vehicle repair costs, and the potential for larger lawsuit settlements. Choosing higher coverage limits offers greater protection against unforeseen expenses in the event of a serious accident.

Calculating Appropriate Coverage Limits: A Practical Approach

Finding the right liability coverage limits for your needs involves assessing your financial situation, including your assets, income, and risk tolerance. A good rule of thumb is to have enough coverage to protect your assets from potential lawsuits. Consider your driving habits and the areas where you frequently drive as well.

Coverage Across State Lines and Key Exclusions

Your liability coverage generally extends to accidents in other states, protecting you while traveling. However, certain exclusions may apply. Intentional acts, like road rage incidents, are typically excluded. Damage to your own vehicle is also not covered under liability; you'll need collision or comprehensive coverage for that. Understanding these aspects of car insurance can help you avoid unexpected expenses.

Vehicle Protection Strategies: Comprehensive Vs. Collision

Protecting your vehicle involves more than just basic liability coverage. It requires understanding comprehensive and collision coverage, two key aspects of car insurance. These coverages protect your car from different types of damage, and understanding the distinctions can save you money and reduce stress in the long run.

Decoding Comprehensive Coverage: Protection From The Unexpected

Comprehensive coverage protects your vehicle from damage not related to a collision with another vehicle or object. This encompasses a wide array of incidents:

- Theft: If your car is stolen, comprehensive coverage can help pay for a replacement.

- Vandalism: This covers damage from malicious acts, such as keying or graffiti.

- Fire: Whether from an accident or another cause, comprehensive covers fire damage.

- Natural Disasters: Damage resulting from hail, floods, or falling trees is typically included.

- Animal Collisions: Hitting a deer or other animal is usually covered under comprehensive.

For instance, if a hailstorm damages your parked car, comprehensive coverage will likely help pay for the necessary repairs. This type of coverage provides valuable protection against unforeseen circumstances.

Understanding Collision Coverage: Protection In A Crash

Collision coverage protects your vehicle from damage caused by a collision with another vehicle or object, irrespective of who is at fault. This includes:

- Collisions with other vehicles: This is the most frequent type of collision claim.

- Single-vehicle accidents: Hitting a guardrail or a tree falls under collision coverage.

- Rollover accidents: Damage from a rollover, even without another vehicle involved, is covered.

Imagine accidentally backing into a pole. Collision coverage would help pay for the repairs to your car.

Comprehensive Vs. Collision: Key Differences Summarized

| Feature | Comprehensive | Collision |

|---|---|---|

| Cause of Damage | Non-collision events | Collision with another vehicle or object |

| Fault | Not relevant | Not relevant |

| Deductible | Applies | Applies |

Remember, both comprehensive and collision coverage have deductibles. Your deductible is the amount you pay out-of-pocket before your insurance coverage begins. A higher deductible lowers your premium, but increases your expenses if you need to file a claim. Read also: How to Master Comprehensive and Collision Insurance Decisions.

When To Consider Dropping Coverage

As your car ages and its value depreciates, the cost of comprehensive and collision coverage might exceed the potential payout from a claim. At that point, you could consider dropping these coverages. This is a personal decision based on your financial situation and risk tolerance.

Leased Or Financed Vehicles: Coverage Requirements

Lenders typically require comprehensive and collision coverage for leased or financed vehicles. This protects their investment. Failure to maintain these coverages may violate the terms of your loan or lease agreement.

Specialized Protections And Replacement Cost

Consider additional coverage for custom parts or equipment not included in standard policies. Replacement cost coverage, though more expensive, provides the full value of replacing your car with a new one, rather than its depreciated value. These are important factors to consider when developing a comprehensive car insurance strategy.

Medical Protection: Safeguarding Against Healthcare Costs

Medical expenses after a car accident can add up quickly, even with health insurance. This section explains two key car insurance coverages that address medical costs: Personal Injury Protection (PIP) and Medical Payments Coverage. We'll also discuss how these coverages work with your health insurance and offer guidance on selecting the right coverage limits.

Personal Injury Protection (PIP): No-Fault Medical Coverage

PIP, often referred to as "no-fault" coverage, pays for medical expenses and sometimes lost wages after an accident, no matter who caused it. Whether you were at fault or not, your PIP coverage will help pay your bills. PIP often covers other expenses too, such as lost wages, childcare, and home healthcare services needed because of the accident. This can be a vital financial safety net, especially if injuries prevent you from working.

Medical Payments Coverage: An Alternative to PIP

In states where PIP isn't required, Medical Payments Coverage offers a similar benefit. It helps cover medical expenses for you and your passengers, regardless of fault. However, unlike PIP, it typically doesn't cover lost wages. Your medical bills will be addressed, but the financial burden of lost income could still be a problem. Deciding between PIP and Medical Payments Coverage, or whether to have both, depends on your state's requirements and your specific situation.

Coordinating With Health Insurance: A Crucial Step

Both PIP and Medical Payments Coverage work alongside your health insurance. They can cover deductibles, co-pays, and other out-of-pocket expenses that your health insurance might not. If you have a high-deductible health plan, for instance, these coverages can help with costs until your health insurance takes over. This can shield you from large medical bills right after an accident. Because the interplay between these coverages can be complicated, it's important to understand your policies and how they work together.

Lost Wages, Essential Services, and Funeral Expenses

PIP may also cover a portion of lost wages if you can't work due to accident-related injuries. It can also cover essential services, such as childcare or home healthcare, that become necessary after an accident. Some coverages even help with funeral expenses in the event of a fatality. Car insurance costs themselves have been fluctuating. In 2024, average car insurance rates in the U.S. increased by 16.5%, after a 12% rise in 2023. However, 2025 projections anticipate a slower increase of 7.5%, with average full coverage costs topping $2,100 annually. Costs are rising especially fast in states like Nevada and Florida. You can find more detailed statistics at 2025 State of Auto Insurance. These cost increases add yet another financial layer to the difficulties after a car accident, highlighting the importance of understanding your coverage options.

Determining Appropriate Coverage Limits

Choosing the right coverage limits for medical protection depends on your current health insurance and individual circumstances. If your health insurance is comprehensive and has low out-of-pocket costs, you may not need as much medical coverage on your car insurance. But if your health plan has a high deductible or limited coverage, higher car insurance medical limits can offer important protection. Coordinating your health insurance and car insurance medical coverage is crucial for a well-rounded financial protection strategy. This ensures you're prepared for medical expenses after an accident, no matter who is at fault.

Beyond Basics: Strategic Add-Ons Worth Their Premium

Having covered the core components of car insurance, let's explore the "extras"—those optional coverages that can provide significant value in specific situations. This isn't about buying every add-on, but understanding which ones truly enhance your protection strategy without unnecessarily inflating your premium.

Uninsured/Underinsured Motorist Coverage: Protecting Yourself From Others' Shortcomings

One of the most crucial add-ons is Uninsured/Underinsured Motorist Coverage. This protects you if you're hit by a driver who either has no insurance or insufficient coverage to pay for your damages. In some states, a significant percentage of drivers are uninsured.

If one of them causes an accident that injures you, this coverage can help with medical bills, lost wages, and other expenses. This protection extends to hit-and-run accidents as well. This means even if the at-fault driver flees, you still have a financial safety net.

Uninsured/underinsured motorist coverage becomes particularly vital if you live in an area with a high rate of uninsured drivers.

Rental Reimbursement and Roadside Assistance: Practical Help When You Need It Most

Rental Reimbursement coverage helps pay for a rental car while your vehicle is being repaired after a covered accident. This can be a lifesaver if you rely on your car for daily commutes or essential errands.

Roadside Assistance provides on-the-spot help for issues like flat tires, dead batteries, or towing needs. While often available through separate memberships, bundling it with your insurance can streamline the process and ensure you're covered regardless of location.

Gap Insurance: Bridging the Financial Gap After a Total Loss

Gap insurance is specifically designed for financed or leased vehicles. It covers the difference between the actual cash value of your car and the outstanding loan or lease balance if your car is totaled. This is particularly important in the first few years of ownership, when depreciation can significantly lower a vehicle's value.

This coverage can save you from owing thousands of dollars even after your insurance pays out for a totaled car.

Diminished Value and Rideshare Endorsements: Addressing Specific Needs

Diminished Value Coverage compensates you for the decrease in your car's resale value after an accident, even after repairs. This is often overlooked but can be significant, especially for newer or high-value vehicles.

With the rise of ridesharing, Rideshare Endorsements offer tailored protection for drivers using their personal vehicles for commercial purposes, filling gaps that standard policies might not address.

Optional Coverage Comparison: Cost vs. Benefit Analysis

The following table breaks down supplemental coverage options by typical cost ranges, potential benefit amounts, and scenarios where each proves most valuable.

| Coverage Type | Average Annual Cost | Potential Benefit | Who Needs It Most |

|---|---|---|---|

| Uninsured/Underinsured Motorist | Varies by state and coverage limits | Up to policy limits | All drivers, especially in areas with high uninsured driver rates |

| Rental Reimbursement | $20-$50 | Varies by daily/total limits | Drivers who rely heavily on their car |

| Gap Insurance | $20-$50 | Difference between car's value and loan balance | Drivers with financed or leased vehicles |

| Roadside Assistance | $20-$50 | Cost of towing, jump-starts, etc. | Drivers who travel frequently or have older cars |

| Diminished Value | Varies | Loss in resale value | Owners of newer or high-value vehicles |

| Rideshare Endorsement | Varies | Coverage while driving for ridesharing services | Rideshare drivers |

This table provides a starting point. Consult with your insurance agent to determine the best options and pricing for your specific situation. Strategically selecting add-ons, based on your individual needs and driving habits, can enhance your car insurance coverage and offer valuable protection without overspending.

Premium Optimization: Maximum Protection at Minimum Cost

Optimizing your car insurance premiums involves finding the sweet spot between comprehensive coverage and manageable costs. It's about getting the protection you need without breaking the bank. This section explores how your coverage choices affect your premium, empowering you to make smart decisions about your car insurance.

Understanding The Factors Influencing Your Rates

Several key factors determine your car insurance premium. Your driving history, including any accidents or traffic violations, plays a significant role. Where you live also matters. Rates often vary based on local traffic density and crime rates.

The make and model of your car also influence your premium. More expensive vehicles generally cost more to insure. Your chosen coverage type also has a direct impact. Liability-only coverage typically costs less than full coverage, which includes comprehensive and collision.

Finally, your annual mileage affects your rate. More time on the road statistically translates to a higher risk. Understanding these factors can help you anticipate and manage your insurance costs, allowing you to make informed choices about your coverage.

Strategic Deductible Choices: Balancing Risk and Reward

Your deductible is the amount you pay out-of-pocket before your insurance coverage takes effect. A higher deductible lowers your premium but increases your expenses if you need to file a claim. Choosing the right deductible requires careful consideration.

A higher deductible can lead to significant premium savings, but you need to ensure you can afford the out-of-pocket expense in case of an accident. A lower deductible means higher premiums but a smaller out-of-pocket cost if you have a claim.

This decision depends on your individual financial situation and risk tolerance. If you have a robust emergency fund, a higher deductible might be a good option. If you'd rather minimize out-of-pocket expenses, a lower deductible could be a better fit. For more information on managing insurance costs, read about how to lower home insurance.

Discounts and Bundling: Maximizing Your Savings

Many insurance companies offer discounts based on several factors, such as a clean driving record, insuring multiple vehicles, or bundling policies. Bundling your car insurance with other policies, like home or renters insurance, can often result in considerable savings.

Discounts can effectively lower your premium without compromising your coverage. Some insurers also offer discounts for safety features installed in your car or for completing defensive driving courses. Taking advantage of these opportunities can make a real difference in your overall insurance expenses.

Policy Review Timing: Adapting to Life Changes

It's essential to review your car insurance policy regularly, particularly after significant life events like marriage, buying a new car, or moving. These changes can influence your coverage needs and may qualify you for new discounts.

For instance, adding a teenage driver to your policy will likely increase your premium. Relocating to a new area could also affect your rates. Regular policy reviews ensure your coverage continues to meet your current needs and remains affordable.

Claim Strategy: When to Pay Out-of-Pocket

For minor accidents with minimal damage, it might be cheaper to pay for repairs out-of-pocket than to pay your deductible and potentially face higher premiums after filing a claim. Carefully evaluate the repair costs and your deductible before filing a claim.

Sometimes, paying out-of-pocket is the more cost-effective choice in the long run. This proactive approach can help you keep your premiums lower over time. By understanding these aspects of car insurance, you can optimize your premiums and secure the protection you need at a price you can afford.

Building Your Protection Strategy: Personalized Coverage Decisions

Building a robust car insurance coverage strategy involves more than just finding the cheapest policy. It requires a personalized approach that considers your specific needs, financial situation, and risk tolerance. This section provides a practical framework for making informed decisions about your car insurance coverage, ensuring you're adequately protected without overspending.

Assessing Your Risk Profile and Financial Resilience

The first step in building a personalized car insurance strategy is understanding your risk profile. This involves considering factors like your driving history, the type of vehicle you drive, and your location. For example, drivers with a history of accidents or tickets generally face higher premiums. Similarly, living in a busy urban area might increase your risk compared to a rural setting.

Next, assess your financial resilience. How much could you comfortably pay out-of-pocket after an accident? This helps determine the right deductible and coverage limits. If you have a healthy emergency fund, you might be comfortable with a higher deductible, which lowers your premium. If your savings are limited, a lower deductible might offer better peace of mind, despite a higher premium.

Comparing Policies Beyond Premium Quotes

When comparing car insurance policies, look beyond just the premium. Carefully examine the coverage details. Don't just focus on the price; delve into the specifics of what's covered and, importantly, what's not covered. Use a coverage comparison worksheet to compare different policies side-by-side. Pay close attention to the coverage limits, deductibles, and any exclusions.

Identifying Red Flags and Negotiation Approaches

Be wary of policies with extremely low premiums. They might have limited coverage or high deductibles. Carefully review the policy documents for any red flags, such as exclusions for certain accidents or limitations on coverage amounts. Don't hesitate to negotiate with insurance providers. Ask about discounts, such as safe driver discounts or bundling discounts, to maximize your savings. To combine comprehensive coverage with savings, explore strategies to reduce insurance premiums.

Debunking Insurance Myths and Establishing a Review Protocol

Many myths surround car insurance, such as the false belief that red cars cost more to insure. Educate yourself about these myths to avoid basing decisions on misinformation. Establish a regular review schedule for your car insurance. Review your policy annually, or after major life changes like buying a new car, moving, or getting married. This ensures your coverage aligns with your current needs and financial situation.

Addressing Common Consumer Questions: Optimizing Your Protection

Consumers often have questions about car insurance. Common inquiries include: "How much car insurance do I really need?" and "What's the best way to optimize my coverage without overpaying?" The answers depend on individual circumstances.

A young driver on a budget might prioritize minimum liability coverage. A family with significant assets might opt for higher liability limits and additional coverages like umbrella insurance. By thoroughly understanding car insurance coverage, drivers can confidently navigate the complexities of insurance and make informed decisions to protect their financial future.

Comments are closed.