Building Your Foundation For Assessing Insurance Risk

The way insurers approach assessing insurance risk is constantly evolving. It's no longer just about basic checklists or gut feelings.

Top insurance companies now understand that a strong groundwork is essential for decisions that genuinely boost profitability and ensure long-term stability. This means combining established actuarial methods with current analytical tools.

Beyond Basic Scores: Crafting a Full Risk Picture

Using only simple scoring models can give an incomplete picture, possibly missing important details about an applicant. For example, a standard financial score might not reflect behavioral patterns or specific circumstances that greatly affect the likelihood of claims.

Because of this, successful insurers are moving towards creating more comprehensive risk assessment frameworks. These improved frameworks are designed to provide a fuller understanding of potential exposures.

They bring together various data points to build a more detailed and nuanced picture of each individual case. This enables more accurate underwriting and helps in adjusting coverage to match the identified risk precisely. As a result, assessing insurance risk becomes less about simple math and more about detailed evaluation.

Blending Numbers with Nuance: The Art and Science of Assessment

Good risk evaluation is a mix of art and science, requiring a smart balance between concrete data and seasoned judgment. The "science" component includes thorough quantitative analysis, using tools like actuarial tables, financial forecasts, and statistical models.

This forms the objective basis for any solid assessment. The "art," on the other hand, comes from the qualitative understanding that skilled underwriters contribute.

This could involve noticing subtle behavioral signs, taking into account specific local factors, or identifying trends that data by itself might not reveal. This blend of art and science lifts risk assessment beyond a purely mechanical task to a more thoughtful evaluation.

This balanced approach, for instance, is vital when planning for long-term financial security. For more details on applying these ideas, check out our guide on Future-Proof Your Family: How to Select the Best Life Insurance Policy in 2025.

Identifying Metrics That Truly Matter

To create these more developed frameworks, it’s crucial to concentrate on metrics that truly aid the process of assessing insurance risk. Not all information holds the same weight, and top companies are selective about what they track.

Important areas to consider often include:

- Loss History: Past claims data provides direct insight into risk propensity.

- Exposure Variables: Factors specific to the type of insurance, like property characteristics for home insurance or driving records for auto.

- Behavioral Data: Where permissible and relevant, data that indicates lifestyle or operational practices.

- External Factors: Economic indicators, geographical risks, and industry trends.

A key part of effectively assessing insurance risk is having a solid grasp of the wider financial picture of the insurance sector. This is because the industry's financial health directly shapes how premiums are calculated and policy conditions are set. For example, industry profitability, frequently measured by Return on Equity (ROE), offers important background information.

As of 2024, global insurance companies are expected to see their ROE rise to about 10%, with further growth anticipated to 10.7% in 2025. This positive trend can indicate a stronger market, which may affect underwriting capacity and pricing approaches. You can discover more insights about insurance industry performance.

By concentrating on these significant metrics, insurers can greatly improve their underwriting practices and develop more robust portfolios. This methodical approach to organizing risk evaluation is what distinguishes proactive companies, allowing them to stay competitive and manage their exposures carefully.

Leveraging Data Analytics That Actually Drive Results

Following a systematic path to risk evaluation, insurers today are increasingly using data analytics to gain an advantage. Beyond the general buzz around "big data," certain analytical methods are genuinely changing how companies manage assessing insurance risk. This shift is leading to clear improvements in choosing profitable policies.

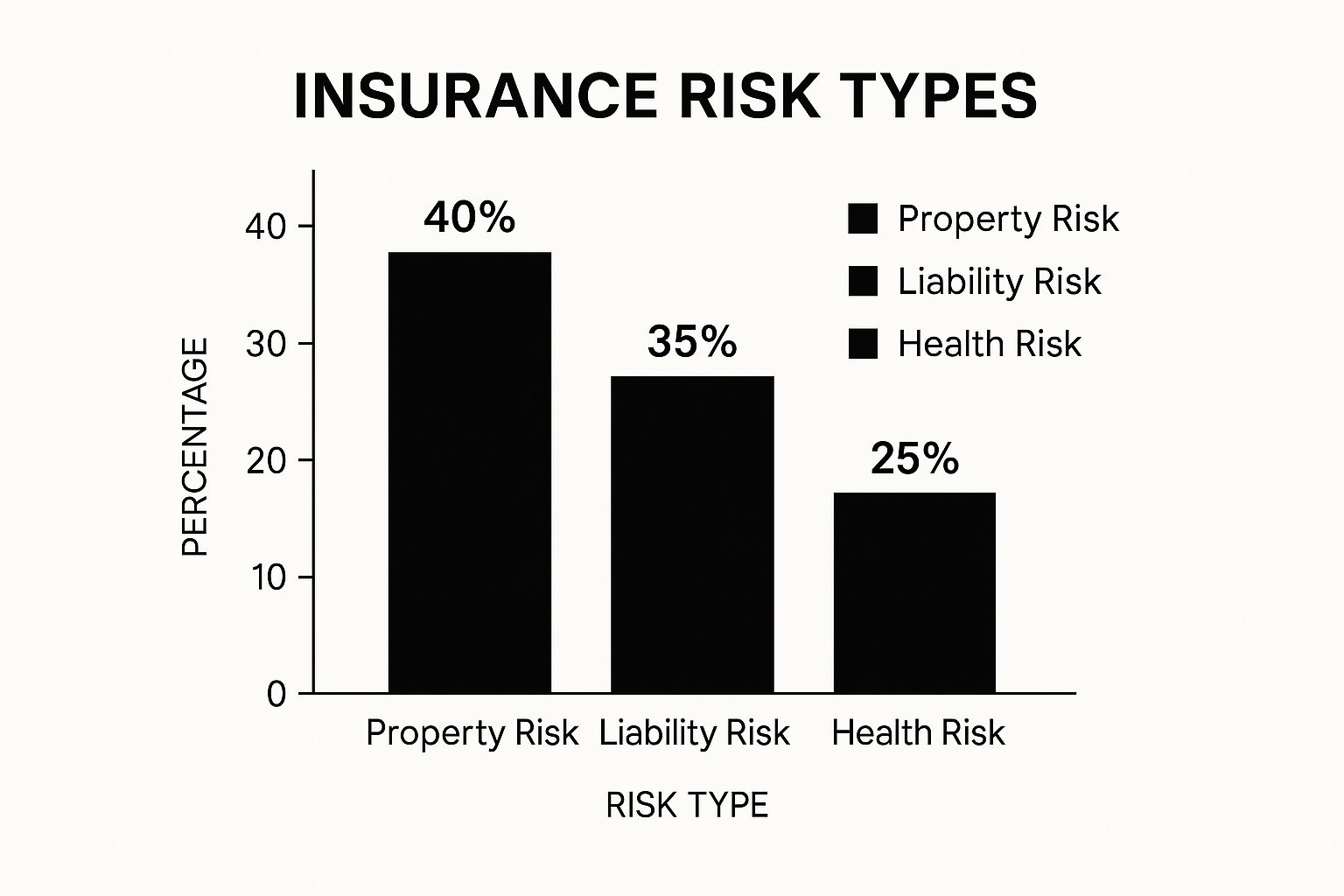

To offer a clearer picture of the challenges insurers face, the chart below shows the usual spread of primary risk categories they handle:

This visual makes it clear that Property Risk accounts for the largest share at 40%. Liability Risk follows closely at 35%, and Health Risk makes up a considerable 25%. These numbers show the varied difficulties in assessing insurance risk in different areas and the importance of precise analytical tools.

Real Applications of AI and Machine Learning

The true effect of data analytics is most apparent when Artificial Intelligence (AI) and Machine Learning (ML) are put to work. For instance, telematics in car insurance gather data from sensors to watch driving habits. This information lets insurers set personalized premiums and has been observed to lower loss ratios by promoting safer driving.

Furthermore, satellite imagery and geospatial data are making a big difference in property insurance. Insurers can now evaluate vulnerability to natural disasters like floods or wildfires with much better accuracy. This often helps prevent major losses by pinpointing high-risk properties before a disaster strikes. Predictive models developed with these technologies help insurers spot potential risks much sooner and, as a result, price policies more accurately.

Identifying High-Return Data Sources

Not all data provides the same value, and the foundation of successful analytics in assessing insurance risk is finding sources that deliver the best Return on Investment (ROI). While conventional demographic data remains useful, other data streams are proving to be extremely valuable.

These can include:

- Behavioral data: Information collected from IoT devices or online activities (when obtained ethically and with permission).

- External unstructured data: Insights from social media trends, news articles, or industry-specific records.

- Granular claims data: In-depth review of past claims to find subtle patterns and connections.

Concentrating on these detailed data sources helps create a more refined understanding of risk profiles. This advanced method allows insurers to go beyond general classifications and move towards more personalized risk evaluations.

The worldwide insurance forecast indicates that growing data volumes are creating new avenues in risk assessment, pricing, and partnerships. Sophisticated data analytics can assist insurers in identifying potential risks earlier and modifying their pricing approaches appropriately. You can explore this topic further and discover more insights about the insurance industry outlook. This change highlights the necessity of adapting to new data sources for effective risk management.

Traditional vs. Modern Risk Assessment Methods

The move towards data-supported insights represents a notable departure from purely conventional methods. To better understand these differences in assessing insurance risk, the following table outlines conventional actuarial methods against contemporary, data-focused techniques.

Traditional vs. Modern Risk Assessment Methods

Comparison of conventional actuarial approaches with data-driven risk evaluation techniques

| Assessment Method | Data Sources | Accuracy Level | Implementation Cost | Time to Results |

|---|---|---|---|---|

| Traditional Actuarial | Historical loss data, demographic tables | Moderate, relies on averages | Lower initially | Slower |

| Modern Data Analytics | Diverse (telematics, IoT, geospatial, behavioral) | Higher, more personalized | Higher initially | Faster, real-time |

This comparison shows how modern techniques, though they might have higher initial setup expenses, provide better accuracy and quicker results. Such improvements are vital for staying competitive.

Frameworks for Effective Analytics Implementation

Putting advanced risk assessment tools into practice needs thorough planning to sidestep common issues. These can involve difficulties such as maintaining data quality, ensuring smooth integration with existing systems, and managing internal resistance to new processes. Successful insurance companies often use organized frameworks to make sure these tools improve, rather than interfere with, existing operations.

Important parts of these frameworks frequently include:

- Beginning with clearly defined pilot programs to check effectiveness and fine-tune models on a limited scale.

- Setting up definite governance and ethical guidelines for how data is used.

- Allocating resources for training and upskilling underwriting teams.

Moreover, gauging the success of these analytics is essential for showing their worth and fostering ongoing improvement. This means tracking Key Performance Indicators (KPIs) such as loss ratio improvements, underwriting speed, and pricing accuracy. By regularly checking these metrics, insurers can confidently expand successful pilot programs and ensure their method for assessing insurance risk stays strong and produces results.

Navigating External Forces That Shape Risk Assessment

Beyond detailed technical models and internal company data, truly effective assessing insurance risk depends on understanding the wider, often unpredictable, external forces. These outside factors can significantly change the risk landscape, pushing insurers to constantly update their approaches. Successfully handling these influences is crucial for ensuring stability and profitability in a constantly shifting market.

Economic Tides and Geopolitical Currents

The state of the global economy and the level of geopolitical stability are significant forces that directly affect the insurance industry. Economic volatility, including sharp changes in inflation or interest rates, can sway consumer habits, impact insurers' investment earnings, and alter how often or how severe certain claims are. Likewise, geopolitical uncertainty, stemming from trade disagreements to regional wars, can create new risks or worsen current ones, complicating the task of assessing insurance risk.

Indeed, risk assessment in insurance is deeply influenced by these geopolitical factors and overarching economic conditions. The worldwide insurance market often finds itself in an unstable setting with high inflation and uncertain interest rates, which naturally impacts consumer confidence and overall economic expansion. For a deeper dive into these challenges, you can learn more about global insurance industry risks from S&P Global Ratings. Insurers, therefore, need to be skilled at reading macroeconomic signals and incorporating them into their risk assessment frameworks.

Adapting to Regulatory Shifts and Regional Nuances

Aside from worldwide economic movements, the regulatory landscape stands out as another key external element. The introduction of new laws, updates to compliance rules, or changes in what regulators focus on can demand major shifts in how insurers evaluate and handle risk. Such changes can influence everything from product development and capital reserves to data management procedures.

Furthermore, insurance companies must pay close attention to regional variations. A risk assessment approach that is effective in one area might not be appropriate elsewhere. This is because of differing:

- Local economic situations

- Legal systems

- Cultural views on insurance

- Unique exposures to natural disasters

Top insurance providers actively keep an eye on these external changes. They build adaptable systems for assessing insurance risk, which helps them tweak underwriting rules and pricing quickly. This way, they stay compliant and competitive while managing their risk levels. For instance, if a region experiences several unexpected major weather disasters, insurers might rapidly update their risk models and pricing for property coverage there, showing a quick reaction to new data. This ability to adapt is essential for maintaining robust underwriting standards, especially when faced with sudden external pressures.

Market Dynamics That Impact Risk Assessment Success

While broad external conditions present a complex environment, the immediate market situation significantly shapes the effectiveness of assessing insurance risk. These market factors are not fixed; they continually mold how insurers must select risks to stay both competitive and financially sound. To successfully manage these conditions, insurers need a solid grasp of current trends and the flexibility to adjust.

Balancing Accuracy with Competitive Positioning

Insurers are in a constant balancing act, aiming for accurate risk selection while also holding a competitive position in the market. During "soft" market cycles, which often feature lower premiums and plenty of available coverage, insurers might be tempted to ease their underwriting rules to attract more business. However, reducing the thoroughness of assessing insurance risk can lead to financial trouble later when claims arise.

This highlights why maintaining strong underwriting discipline is vital, even if competitors adopt more lenient approaches. The long-term stability of an insurance company often hinges on its capacity to avoid short-term gains that could weaken its overall risk portfolio. Achieving this balance is an ongoing test for the industry.

Adapting to Market Cycles and Regulatory Shifts

The insurance market moves in cycles, alternating between "hard" markets (higher premiums, stricter underwriting) and "soft" markets. Insurers who thrive are those that dynamically alter their risk assessment methods in tune with these cycles. For instance, in the first quarter of 2025, global commercial insurance rates saw a 3% decline, the third consecutive quarterly drop. Yet, some areas, like the US casualty market, experienced rate hikes due to issues such as large jury awards and increasing claim severity. Find more detailed statistics here.

Beyond these market fluctuations, regulatory changes often require updates to how risks are assessed. New laws or more stringent enforcement can change which data points are permissible or how certain risks should be weighted. Competitors' actions also matter; if major insurers change their risk appetite or pricing, it can shift the competitive field, compelling others to rethink their own strategies for assessing insurance risk.

Refining Risk Evaluation with Market Intelligence

Leading insurance companies use market intelligence to proactively improve their risk evaluation methods. This isn't just about reacting to new developments; it's about foreseeing shifts and strategically enhancing their assessment tools. A clear understanding of how these market forces affect various insurance segments is essential.

The following table provides a look at how primary risk factors and their evaluation weights can differ, showing the impact of market volatility and pricing sensitivity across various insurance products.

Risk Assessment Factors by Insurance Segment

Key risk evaluation criteria and weight factors across different insurance product lines

| Insurance Type | Primary Risk Factors | Assessment Weight | Market Volatility | Pricing Sensitivity |

|---|---|---|---|---|

| Property Insurance | Location, construction, catastrophe exposure, climate change | High on geographic & perils data | High | Moderate |

| Commercial Auto | Driver history, vehicle type, usage, telematics data | Moderate to High on claims & usage | Moderate | High |

| Cyber Insurance | Security posture, industry, data sensitivity, incident response | Very high on technical & procedural audits | Very High | High |

| General Liability | Business operations, industry sector, safety protocols | Moderate on operational & historical data | Moderate | Moderate to High |

This systematic view aids in customizing the process of assessing insurance risk. For example, the significant market volatility in cyber insurance means that assessment models must be updated regularly. To see how these dynamics affect a specific consumer area, you might find it useful to read: Navigating the Home Insurance Market: Tips for Finding the Best Policy in 2025.

Ultimately, anticipating market changes and aligning assessment capabilities accordingly are fundamental to achieving sustained success in the insurance sector.

Building Risk Assessment Frameworks That Scale

Successfully managing the complexities of the insurance market isn't just about reacting to trends; it calls for proactive, systematic approaches. Excellence in assessing insurance risk depends on solid Risk Assessment Frameworks that deliver consistent, actionable insights across different business lines and amidst fluctuating market conditions. These frameworks form the essential structure for effective risk evaluation.

Establishing Clear Assessment Criteria

The cornerstone of any framework designed to scale is the creation of clear assessment criteria. These standards serve as the baseline for all evaluations, making sure that risk is appraised consistently, no matter the assessor or the specific product line. For instance, underwriting criteria for a commercial property could detail required construction types, fire safety systems, and exposure to local hazards.

When these criteria are clearly defined and shared across the organization, the task of assessing insurance risk becomes more objective and dependable. Such clarity minimizes uncertainty and supports better-informed choices, ultimately leading to a more robust risk portfolio. This foundational step is key to developing a system that can expand alongside the business.

Developing Standardized Protocols with Flexibility

With clear criteria established, the focus shifts to crafting standardized protocols. These protocols map out the specific steps for risk evaluation, confirming that every assessment aligns with the set criteria and upholds quality control benchmarks. Such standardization is vital for consistent application, particularly within larger companies that have numerous underwriters or office locations.

Yet, standardization doesn't mean inflexibility. Good frameworks incorporate adaptability to manage the diverse range of risks insurers face, from individual auto insurance to intricate commercial liability cases. This ensures that while the fundamental method for assessing insurance risk stays uniform, there is capacity to adjust for the distinct features of various risks. For instance, a framework might standardize how data is gathered but still permit detailed examination of varied information, like specific local hazards for a home. For more on policy details, you might find this helpful: The Ultimate Guide to Choosing the Right Home Insurance Policy in 2025.

Creating Feedback Loops for Continuous Improvement

A genuinely scalable framework isn't static; it grows and gets better through effective feedback loops. These systems enable information from actual claims, underwriting results, and market changes to be used for refining assessment criteria and protocols. For example, if a certain risk category consistently results in greater losses than anticipated, the feedback system would initiate a review of its assessment method.

This cycle of review and adjustment helps ensure that the approaches for assessing insurance risk stay current and precise. Top insurers draw on information from several key areas:

- Claims analysis: Pinpointing patterns in how often losses occur and how severe they are.

- Underwriter experience: Gathering firsthand knowledge from professionals working directly with risks.

- Market intelligence: Keeping track of shifts in the risk environment and what competitors are doing.

- Regulatory updates: Maintaining ongoing regulatory compliance.

By methodically integrating this feedback, insurance companies can continually strengthen their risk assessment skills. This ensures their frameworks can grow with the business and also adjust to new and evolving risk scenarios. This dedication to ongoing improvement is fundamental to achieving lasting success in managing insurance risk.

Measuring And Improving Your Risk Assessment Performance

Successfully assessing insurance risk is far from a one-off job; it's an ongoing process of checking how you're doing and making things better. To keep your strategies effective and your business profitable, it's vital to regularly measure your performance and always look for ways to improve. This forward-thinking approach helps insurers stay prepared for new challenges and keep their financial footing secure.

Identifying Key Performance Indicators (KPIs) for Success

The first important step in making your risk assessment better is to clearly define what success means for you. When it comes to assessing insurance risk, several Key Performance Indicators (KPIs) can give you a clear picture of how well your current methods are working.

A primary measure is the Loss Ratio, which looks at incurred losses against earned premiums; a consistently low and stable loss ratio often points to accurate risk evaluation and pricing. The Combined Ratio takes this further by adding underwriting expenses, where a figure below 100% usually means your underwriting is making money.

Another key metric is Assessment Accuracy, which checks how well your initial risk predictions matched actual claims. Lastly, Underwriting Efficiency – how much time and money it takes to assess each risk – is crucial, because smoother processes can boost profits without sacrificing accuracy.

Establishing Meaningful Benchmarks and Tracking Progress

After you've pinpointed your KPIs, the next move is to set up meaningful benchmarks. These benchmarks act as a standard to measure your performance against and shouldn't be random; they need to come from solid data.

You can create these benchmarks using several sources:

- Historical Performance: Your own company's past figures provide a straightforward baseline to compare against and improve upon.

- Industry Averages: Looking at how you stack up against general industry numbers can show where you stand competitively and where you can grow.

- Specific Goals: Setting clear, challenging but reachable targets for improvement can focus your team's efforts.

Carefully tracking these KPIs over time is very important. This long-term view is extremely useful for assessing insurance risk trends, identifying where your assessment models might be becoming less effective, or spotting new risks you hadn't fully accounted for. For instance, if the loss ratio for a certain type of policy starts to creep up, it's a strong sign that you need to revisit the underwriting rules for that specific group.

Building Robust Feedback Loops for Continuous Enhancement

Getting better at assessing insurance risk really depends on learning from your experiences and the data you collect. This involves setting up and keeping solid feedback loops that feed new information back into how you assess risk.

A key part of this is Claims Experience Integration. Every single claim, whether paid or not, offers a wealth of information. It's crucial to regularly examine claims data – looking at the type of loss, how severe it was, and how it stacked up against your initial risk assessment – to make your models better. For example, if one type of commercial property keeps having more liability claims than you predicted, you definitely need to look at your assessment rules for that business category.

Also important is Market and Underwriter Feedback. Gathering observations from your frontline underwriters, brokers, and even customers can give you useful qualitative information. These people might spot new risk elements or slight changes in the market that your data models haven't picked up yet. This ongoing cycle is similar to the "maintain the assessment" stage found in other areas of risk management, helping your risk assessment methods to develop and get better.

The Role of Regular Reviews and Maintaining Accuracy

Having scheduled, regular performance reviews is a critical piece of this improvement puzzle. These reviews aren't just about glancing at charts and figures; they are deep-dive strategic talks with underwriters, actuaries, and managers to figure out why your performance numbers look the way they do.

During these reviews, you should take a hard look at:

- Assessment Quality: Are your risk assessments applied consistently by different underwriters or teams? Is the thinking behind underwriting choices clear, properly recorded, and easy to defend?

- Identifying Improvement Opportunities: Where are the biggest differences between what you predicted and what actually happened? What specific adjustments to your data, analytical tools, or internal ways of working could help narrow these differences?

The main objective here is to make sure your methods for assessing insurance risk stay sharp and correct in a market that's always shifting. Just like businesses in other sectors have to adjust to new tools or changing threats, insurers need to keep honing their understanding and measurement of risk. This dedication to constant improvement is key to keeping your business profitable over the long haul and properly looking after your policyholders.

Comments are closed.