Understanding Today's Home Insurance Landscape

Home insurance premiums are on the rise, and understanding the reasons behind this increase is the first step toward potentially lowering your costs. Multiple factors are converging to create this upward trend, impacting homeowners across the board. This section explores these market forces and how they specifically affect your individual premium, providing valuable context for saving money.

The Perfect Storm: Factors Driving Premium Increases

Several key factors contribute to the rising cost of home insurance. A primary driver is the increasing frequency and severity of climate events. Hurricanes, wildfires, and severe storms cause substantial damage, leading to higher claims payouts for insurance companies. These costs are then passed on to policyholders through increased premiums.

Inflation also plays a crucial role. The rising cost of building materials and labor directly impacts the expense of rebuilding or repairing a home after a claim. Consequently, even minor repairs are now more expensive, pushing premiums higher. These rising costs represent a significant challenge for homeowners.

In 2024, the average rate surge for new home insurance policies reached 17.4%, affecting both new policies and renewals. Over a three-year period, the average homeowner saw a nearly 69% increase in their premiums. This surge was fueled by factors such as inflation, severe weather events, and rising reinsurance costs. Explore this topic further.

How Insurers Calculate Your Risk

Understanding how insurance companies assess risk is key to potentially lowering your home insurance costs. Insurers use complex algorithms and data to create a risk profile for each homeowner. Factors like your home's age, location, construction materials, and proximity to fire hydrants all contribute to this profile.

For instance, a home built with fire-resistant materials in a community with a strong fire department will likely have a lower premium than a comparable home in a high-risk wildfire area. This is because the risk of a major claim is lower. Your personal claims history is also a significant factor. Prior claims, even for relatively minor incidents, can increase your premium.

Why Premiums Vary, Even on the Same Street

You may wonder why your neighbor's premium differs from yours, even if your homes appear similar. Several localized factors can account for these discrepancies. One home might be located in a floodplain, increasing its flood risk, while another sits on higher ground.

One homeowner may have invested in security upgrades that reduce their premium, while another hasn't. These seemingly small differences can result in substantial premium variations. This underscores the importance of understanding your specific risk profile. By identifying and mitigating these factors, you can potentially lower your home insurance costs.

Security Upgrades That Actually Lower Your Premium

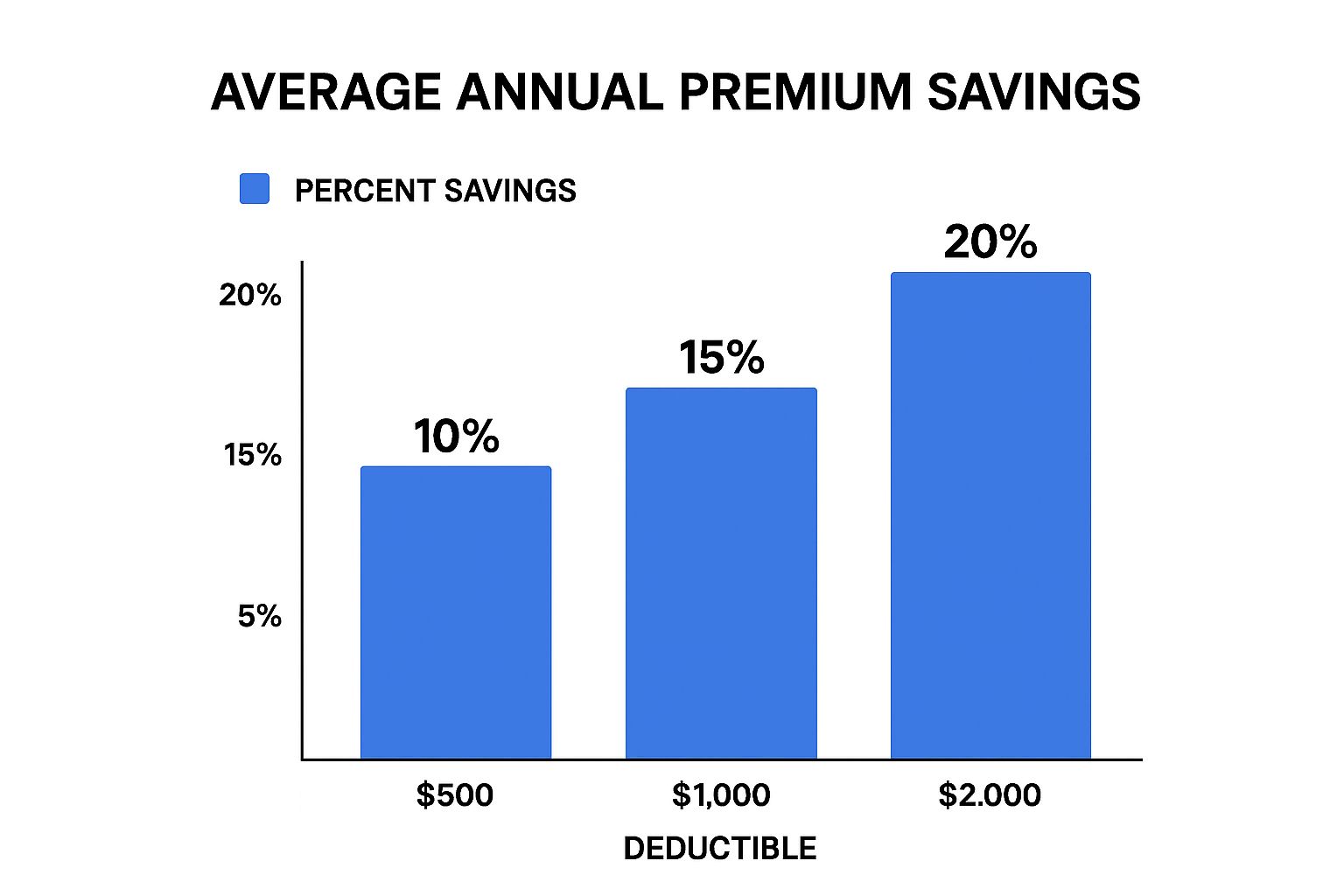

The infographic above illustrates the connection between your deductible and potential premium savings. A higher deductible often leads to lower premiums, with savings increasing as your deductible goes up.

For example, raising your deductible from $500 to $1000 could save you 15% on your annual premium. A $2000 deductible could yield 20% savings. This emphasizes the need to select a deductible that balances potential savings with your ability to pay out-of-pocket expenses if you need to file a claim. Home security systems can frequently lower insurance premiums; it's worthwhile to research reputable local CCTV installation companies.

Smart Home Technology: Hype vs. Reality

Beyond standard safety features like smoke detectors, specific security upgrades can significantly reduce your home insurance premiums. Centrally monitored alarm systems, which notify authorities in the event of a break-in, fire, or other emergencies, are a prime example.

These systems often qualify you for discounts because they lessen the risk of substantial losses for the insurance company. Smart home technology, such as smart locks and water leak detectors, also offers valuable protection.

Water leak detectors, for instance, can quickly identify and alert you to small leaks, preventing them from becoming expensive water damage claims. This proactive approach can result in lower premiums. Learn more about related savings in this article on how to master saving on car insurance.

Maximizing Your ROI: Prioritizing Security Investments

Not every security upgrade carries the same weight regarding premium reductions. While some provide significant discounts, others offer minimal or no savings at all. Prioritizing upgrades that give the best return on investment in terms of premium reduction is crucial.

Consider a graded approach to implementing security enhancements. Begin with the essentials: smoke detectors, burglar alarms, and deadbolt locks. These fundamental components often qualify you for basic discounts.

From there, explore further upgrades tailored to your specific needs and risk assessment. Focus on features offering the highest potential for premium savings. This strategic approach helps you maximize your overall return.

To help illustrate potential savings and payback periods, let's look at the following table:

Security Upgrades and Potential Premium Discounts: This table compares different home security improvements, their approximate installation costs, and the average insurance premium discount they may provide.

| Security Feature | Installation Cost | Average Premium Discount | Payback Period |

|---|---|---|---|

| Centrally Monitored Burglar Alarm | $300 – $500 | 5% – 15% | 2-5 years |

| Smoke Detectors | $50 – $150 per detector | 2% – 5% | 1-3 years |

| Deadbolt Locks | $25 – $100 per lock | 1% – 3% | Less than 1 year |

| Smart Locks | $150 – $300 per lock | 3% – 7% | 2-4 years |

| Water Leak Detectors | $50 – $150 per detector | 2% – 5% | 1-3 years |

As you can see, simpler upgrades like deadbolt locks offer a quick return on investment, while more complex systems like centrally monitored alarms offer greater discounts but take longer to recoup the installation cost. Carefully consider your budget and security needs when making these decisions.

Location Matters: Regional Strategies for Lower Premiums

Your home insurance premium is significantly impacted by location. This means that strategies for reducing these premiums need to account for regional variations. A one-size-fits-all approach simply won't work. This section explores location-specific strategies to help you save.

Coastal Concerns: Protecting Your Home From Hurricanes

Coastal homeowners face the added challenge of hurricane risk. Reinforcing your roof with hurricane straps or installing storm shutters can increase your property's resilience to wind and water damage, often resulting in lower premiums. Upgrading your sliding glass doors can also enhance security and protection. For more information on protecting your sliding glass doors, see this helpful guide: sliding glass door protection. Another impactful measure is elevating your home's foundation, if possible. This can significantly reduce the risk of flood damage and, consequently, lower your flood insurance costs.

Wildfire Zones: Mitigating Fire Risk

In wildfire-prone areas, mitigating fire risk is crucial for lower insurance premiums. Creating defensible space is essential. This involves clearing brush and maintaining appropriate landscaping around your home to prevent fires from spreading to your property. Using fire-resistant materials for roofing and siding further reduces vulnerability to fire damage. Insurers often reward these precautions with lower premiums.

Regional Insurers: Finding Local Savings

While national insurance companies are widely recognized, exploring regional insurers can often lead to significant savings. Regional insurers possess a deeper understanding of local risks and can offer more competitive rates for specific areas. They may also provide specialized coverage tailored to regional needs, such as earthquake insurance in California or hurricane coverage in Florida. This targeted approach can result in substantial savings compared to the generic policies offered by national carriers. Homeowners insurance costs vary considerably across the US. The average annual premium for an HO-3 policy is around $1,411, but this can be significantly higher in disaster-prone states. For example, Florida has the highest average premiums at $2,437, while Oregon has the lowest at $793. You can find more detailed statistics here.

State-Specific Programs and Discounts

Many states offer programs and discounts that can reduce home insurance premiums. These initiatives might include subsidies for wind mitigation upgrades in coastal regions or tax credits for installing fire-resistant materials in wildfire zones. Researching these state-specific options can uncover valuable savings opportunities. Also, be sure to contact your insurance agent to inquire about any applicable regional discounts. These localized discounts can further reduce your premium.

Fine-Tuning Your Policy: Deductibles and Coverage Limits

Raising your deductible is a common way to lower home insurance premiums. However, strategically adjusting your coverage limits and endorsements can also significantly impact your costs. This section explores how to find the balance between premium savings and sufficient protection.

Understanding Deductibles

Your deductible is the amount you pay out-of-pocket before your insurance coverage begins. A higher deductible typically results in lower premiums. This is because you're assuming more of the financial responsibility if you have to file a claim. For example, increasing your deductible from $500 to $1,000 could save you between 10% and 25% on your annual premium. However, make sure you have enough money readily available to cover the higher deductible if a claim arises.

Calculating Your Optimal Deductible

The ideal deductible for your situation depends on your personal finances and how much risk you're comfortable with. If you have considerable savings and are comfortable with potentially larger out-of-pocket expenses, a higher deductible can be a smart choice. On the other hand, if your savings are limited, a lower deductible might provide greater peace of mind. A helpful exercise is to calculate the break-even point for different deductible levels based on your home's value.

To illustrate this, let's look at the following scenarios:

The table below illustrates how different deductible increases affect annual premiums across various home values.

Deductible Increase Scenarios and Premium Savings

| Home Value | Current Deductible | New Deductible | Annual Premium Savings | Break-even Point (Years) |

|---|---|---|---|---|

| $250,000 | $500 | $1,000 | $200 | 2.5 |

| $250,000 | $500 | $2,000 | $400 | 1.25 |

| $500,000 | $1,000 | $2,500 | $300 | 0.83 |

| $500,000 | $1,000 | $5,000 | $600 | 0.83 |

This table shows how increasing your deductible can lead to significant savings over time. The break-even point represents the time it takes to recoup the difference in the deductible amount through lower premium payments.

Rightsizing Your Dwelling Coverage

Dwelling coverage protects the physical structure of your home. It's crucial to have enough coverage to rebuild your home if it's ever completely destroyed. However, over-insuring your home can result in paying for coverage you don't need. Ensure your dwelling coverage accurately reflects your home's replacement cost, not its market value. This means considering the actual cost to rebuild, including materials and labor, not just what your home might sell for in the current real estate market.

Evaluating Endorsements

Endorsements are additions to your policy that offer specialized coverage. While some endorsements provide essential protection, others may be redundant based on your needs and location. Carefully review your endorsements and determine if they are truly necessary for your situation. For instance, if you live in an area with minimal flood risk, flood insurance might be an unnecessary expense. Removing unnecessary endorsements can noticeably lower your premium. Additionally, consider having a thorough policy review with an independent insurance advisor. They can provide personalized guidance and help you find potential savings your regular agent might miss, ensuring you have the right coverage at the best price.

Uncovering Hidden Discounts and Bundling Opportunities

Many homeowners are unaware of the potential savings available through various home insurance discounts. This often leaves a significant amount of money on the table. This section explores these often-hidden discounts, ranging from occupation-based reductions to automatic loyalty rewards. We'll also discuss how combining multiple discounts can lead to substantial premium reductions and offer effective negotiation strategies with insurance providers. For further insights, you might find this resource helpful: How to master scoring home insurance discounts.

The Untapped Potential of Home Insurance Discounts

Insurance companies don't always broadly advertise the full spectrum of discounts they offer. This means homeowners need to be proactive in seeking them out. These discounts can range from 5% to 25% or more, significantly impacting your final premium. The actual percentage depends on the specific discount and the individual insurer.

Some commonly available discounts include:

- Safety features: Installing smoke detectors, burglar alarms, and fire extinguishers can often qualify you for a discount.

- Security systems: Centrally monitored alarm systems and smart home devices often lead to even larger discounts.

- Claim-free history: Maintaining a history free of filed claims demonstrates lower risk and often earns a discount.

- Loyalty programs: Many insurers reward customer loyalty with discounts for staying with them for a specified period.

- Bundling policies: Combining home and auto insurance with the same provider often results in a discounted rate for both.

- Occupations: Certain professions, such as teachers or firefighters, might be eligible for specific discounts.

Stacking Discounts for Maximum Savings

Combining or "stacking" multiple discounts can significantly amplify your savings. This strategic approach can result in substantial premium reductions. For example, a homeowner with a monitored security system, a claim-free history, and bundled home and auto policies might see their premium decreased by 30% or more. This highlights the considerable financial benefit of actively pursuing all applicable discounts.

Negotiating With Your Insurer

Don't be afraid to negotiate with your insurance company. Inquire about all potential discounts and be prepared to discuss your options. Many insurers are open to negotiation, particularly with long-term customers.

Here are a few negotiation tips:

- Be prepared: Familiarize yourself with your policy details and the specific discounts you want to discuss.

- Be polite but firm: Clearly express your desire for a lower premium.

- Compare quotes: Researching rates from other insurers can provide leverage during negotiations.

- Document everything: Maintain records of all conversations and correspondence with your insurer.

Bundling: Real Savings or Cost Shifting?

While bundling home and auto insurance is often advertised as a money-saving strategy, it's important to approach bundled offers with a critical eye. Some bundles offer genuine discounts, while others simply redistribute the total cost across multiple policies. Carefully analyze the bundled offer to confirm actual savings and compare it to separate policies from different insurers. A bundled policy isn't always the most cost-effective option. By thoroughly exploring each available discount and employing effective negotiation techniques, you can potentially reduce your home insurance premium without compromising necessary coverage.

Climate-Proofing Your Home for Premium Reduction

As weather-related insurance claims rise, strengthening your home against climate change can significantly impact your insurance premiums. This translates into potential savings for homeowners willing to invest in protective measures. This section explores the most valuable climate-resistant improvements from an insurer's perspective, using their data as a guide.

Targeted Improvements for Maximum Impact

Insurers understand that specific home improvements directly correlate with a reduced risk of weather-related damage. A robust roof, for instance, offers better protection against high winds and heavy snow, minimizing the need for costly repairs. Likewise, effective water management systems, such as proper drainage and sump pumps, mitigate the risk of water damage from flooding or leaks.

These targeted improvements can lead to lower premiums. The influence of climate change on home insurance costs is becoming increasingly noticeable. Between 2018 and 2022, average homeowners insurance premiums climbed 8.7% faster than inflation. This surge is directly attributed to the increasing frequency and intensity of climate-related damage. Find more detailed statistics here.

Real-World Savings: Homeowner Case Studies

Examining the experiences of homeowners who've invested in climate-proofing upgrades offers valuable insights. By exploring real-world examples, we can see the tangible impact of these improvements. We'll delve into actual premium savings achieved and uncover any unexpected benefits.

For example, some homeowners discovered that improved insulation, initially installed for wind resistance, also resulted in lower energy bills. These added advantages further amplify the overall value proposition of climate-proofing projects.

Financial Assistance: Tax Incentives and Rebates

Investing in climate-proofing measures often involves upfront costs. However, many homeowners may not be aware of the various financial resources available to help offset these expenses. Federal and state governments offer programs designed to incentivize energy efficiency and climate resilience.

Some insurance companies also provide discounts to policyholders who make specific upgrades. By capitalizing on these opportunities, homeowners can make climate-proofing their homes more financially manageable.

Implementing Climate-Proofing Measures: A Step-by-Step Guide

This section provides practical guidance tailored to your home's vulnerabilities and regional climate risks.

-

Assess your risks: Determine the specific climate threats prevalent in your area. This could include hurricanes, wildfires, floods, or severe winter storms.

-

Prioritize improvements: Focus on upgrades that address your most significant vulnerabilities and offer the greatest potential for premium reductions.

-

Seek professional advice: Consult with qualified contractors and insurance professionals to identify the most effective and cost-efficient solutions.

-

Explore financing: Research available tax incentives, rebates, and financing options to help cover upgrade costs.

-

Document your upgrades: Maintain detailed records of all improvements, including receipts and permits. This documentation will be essential when seeking premium discounts from your insurer.

By strategically implementing these climate-proofing measures, you can enhance your home's resilience to extreme weather, safeguard your investment, and potentially lower your home insurance premiums.

The Strategic Shopping Method Most Homeowners Miss

Shopping for home insurance isn't just about grabbing a few quick online quotes. It's a strategic process that can unlock significant savings when done right. This section reveals how to effectively time your market search, structure your comparison requests for accurate results, and use competitive quotes to your advantage.

Timing Your Insurance Search: Beyond Renewal

Many homeowners only consider their insurance at renewal time. However, shopping a few months before your renewal date offers several benefits. This provides ample time to compare offers, negotiate with insurers, and switch providers without pressure. You might be interested in: How to master navigating the home insurance market. Plus, some insurers offer early-switching discounts, rewarding a proactive approach.

Structuring Comparison Requests: Apples to Apples

When requesting quotes, ensure you are comparing similar coverage levels. Requesting quotes for identical coverage limits, deductibles, and endorsements ensures an accurate comparison. It's like buying a car—you wouldn't compare a basic sedan's price with a fully loaded SUV. Likewise, comparing differing insurance coverage can be misleading. Clearly specify your requirements to each insurer.

Leveraging Competitive Quotes: Negotiating With Your Current Insurer

Gathered competitive quotes? Use them to negotiate with your current insurer. Present the quotes and ask if they can match or beat the competitor's offer. This can lower your premium without switching providers. For instance, if a competitor offers a much lower premium for similar coverage, your insurer might reduce your rate to keep your business. Be prepared to switch if they won't negotiate.

Independent Agents: Accessing Specialized Markets

Consider an independent insurance agent. Unlike captive agents representing a single company, independent agents work with multiple insurers. This provides access to a wider range of policies and potentially better rates. They can also offer personalized advice and help navigate the complexities of insurance. This personalized guidance is especially useful for unique coverage needs.

Digital Comparison Tools: Accuracy and Limitations

While digital comparison tools are convenient for initial quotes, they don't always provide accurate results. Some prioritize certain insurers or show limited options, leading to an incomplete market view. Use these tools as a starting point, but confirm details and secure the best rate directly with insurers or an independent agent.

Evaluating Insurers: Beyond Price

Price is crucial, but consider other factors when choosing an insurer. Research their financial strength and customer satisfaction ratings. A financially stable company with a strong customer service reputation is more likely to provide a positive claims experience. This adds security beyond simply finding the cheapest premium. Through planning and strategic shopping, homeowners can reduce premiums, often by 25-40%, without sacrificing coverage. This empowers homeowners to control their costs and protect their finances.

Comments are closed.