Demystifying Insurance Endorsements: What They Are and Why They Matter

Think of your insurance policy as a suit. It offers general protection, but might not fit perfectly. That's where insurance endorsements come in. Sometimes called a rider, an endorsement is a modification to your existing policy, altering its coverage.

This allows you to customize your protection without needing a brand new policy, tailoring it to your specific needs. Imagine owning valuable jewelry. Your standard homeowner's insurance might not cover its full value.

By adding an endorsement specifically for that item, you ensure it's fully protected. This bridges the gap between a standard policy and your individual requirements. Endorsements are crucial components, allowing adjustments without issuing new policies.

They often broaden coverage, add coverage for specific items, or modify policy conditions. In the global insurance market, valued at $9.8 trillion in 2021, endorsements help insurers meet changing customer needs and comply with regulations. Find more detailed statistics here: https://www.bccresearch.com/market-research/finance/insurance-industry-market.html

Why Endorsements Matter: Tailoring Protection

Endorsements aren't just about adding coverage; they can modify or even limit it. This flexibility lets you fine-tune your policy to your risk profile and budget. You might increase your deductible to lower your premium, for example.

Or you could add coverage for specific risks like water backup damage. Endorsements also clarify policy terms, preventing confusion during a claim. They spell out what is and isn't covered, giving you peace of mind.

Understanding your endorsements is key to maximizing your insurance effectiveness.

Endorsements and Your Base Policy: Working Together

Your base policy provides the foundation of your coverage. Endorsements act as building blocks, enhancing and refining that foundation. This interplay creates a robust, personalized safety net.

It ensures your policy reflects your unique circumstances. Understanding this relationship between your base policy and its endorsements is crucial for comprehensive protection.

The Insurance Endorsement Landscape: Types That Transform Coverage

Think of insurance endorsements as specialized tools that enhance a basic toolkit. Your standard insurance policy provides fundamental coverage, but endorsements allow you to customize it to fit your unique circumstances. This section explores the various types of endorsements and how they can enhance or modify your existing protection.

Expanding Coverage: Enhanced Protection For Specific Needs

Many endorsements broaden your existing coverage. For valuable items like jewelry or art, a scheduled personal property endorsement offers additional protection beyond the standard policy limits. These items often have limited coverage under a typical homeowner's policy. Likewise, if you're worried about water damage from a sump pump failure or sewer backup, a water backup endorsement can provide coverage for these often-excluded events.

For your home itself, endorsements can strengthen your dwelling coverage. A guaranteed replacement cost endorsement ensures your home can be rebuilt even if the cost exceeds your policy limit. This provides peace of mind, especially with fluctuating construction costs. This type of endorsement is particularly relevant following a widespread natural disaster, where material and labor costs can quickly escalate.

Limiting or Clarifying Coverage: Fine-Tuning Your Policy

Not all endorsements add coverage. Some endorsements can limit coverage for specific risks or clarify existing policy terms. For instance, if your home has an older roof, an insurer might add an endorsement to exclude roof damage. This can potentially lower your premium and allow you to obtain coverage even if certain aspects of your property don’t meet standard underwriting guidelines.

Endorsements can also clarify ambiguous language within a policy. This added clarity is essential during a claim, preventing disputes and streamlining the claims process. Precise wording ensures both you and the insurance company are on the same page about what is and isn’t covered. You might be interested in Navigating the Legal Consequences: Understanding the Impact of Cons.

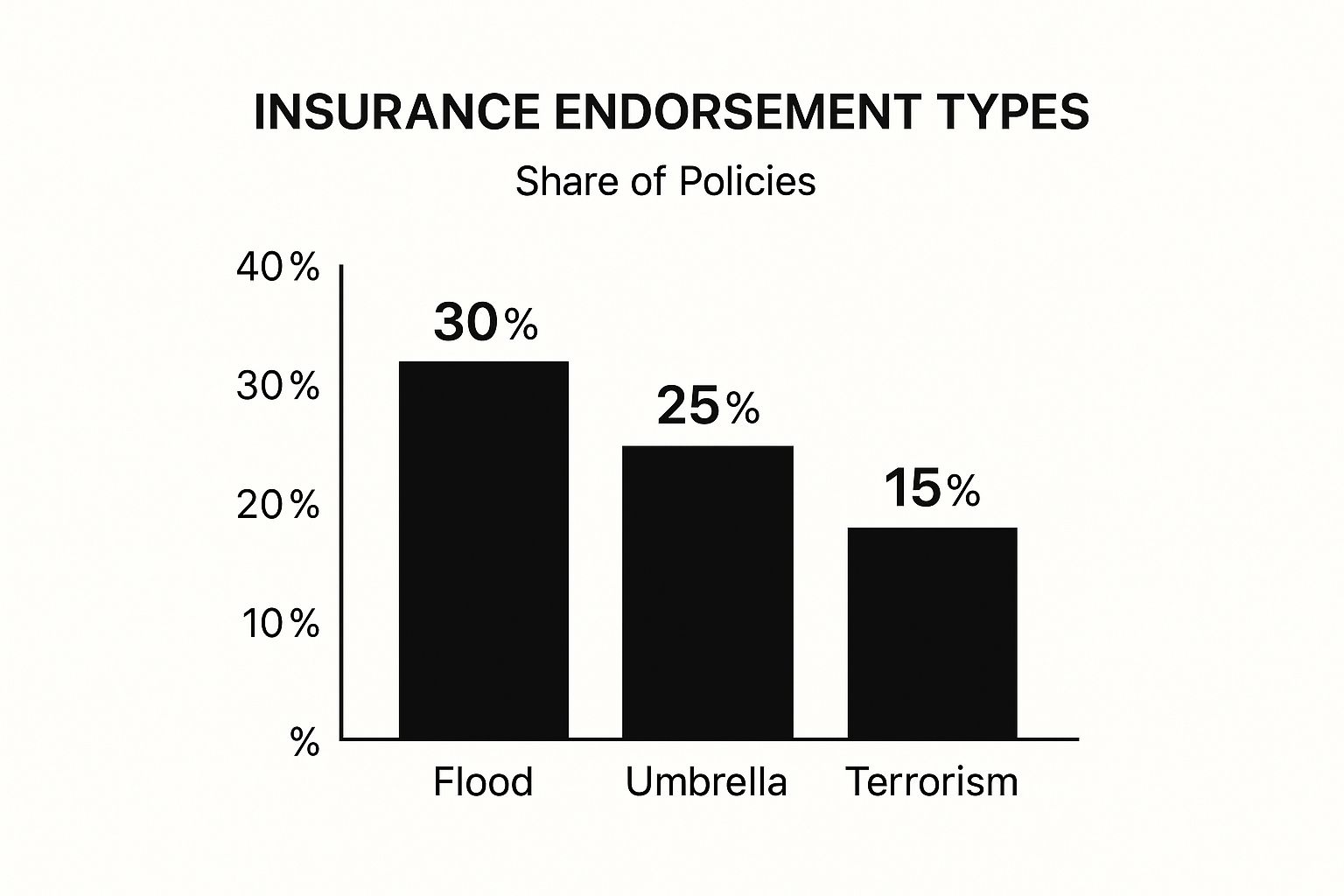

Endorsement Categories Across Insurance Types: A Visual Breakdown

The following data chart depicts the prevalence of different endorsement categories across various insurance types. It highlights how policyholders often tailor their coverage to better suit their needs.

As the chart reveals, certain endorsements are more commonly used within specific insurance types.

To further illustrate common endorsements across insurance types, the following table provides additional detail:

Common Insurance Endorsements by Policy Type

| Insurance Type | Common Endorsements | Purpose | Coverage Impact |

|---|---|---|---|

| Homeowners | Scheduled Personal Property | Covers high-value items beyond standard limits | Increases coverage for specific items |

| Homeowners | Water Backup | Protects against water damage from sewer or drain backups | Adds coverage for a common exclusion |

| Homeowners | Guaranteed Replacement Cost | Ensures home is rebuilt even if cost exceeds policy limit | Increases dwelling coverage |

| Auto | Rental Reimbursement | Covers cost of a rental car while your vehicle is being repaired | Adds coverage for transportation expenses |

| Auto | Roadside Assistance | Provides assistance with towing, flat tires, etc. | Adds coverage for roadside emergencies |

| Auto | Custom Equipment | Covers aftermarket parts or modifications to your vehicle | Increases coverage for vehicle enhancements |

| Life | Accidental Death Benefit | Pays an additional benefit if death is due to an accident | Increases death benefit in specific circumstances |

| Life | Waiver of Premium | Waives premium payments if you become disabled | Modifies payment terms under specific conditions |

| Life | Long-Term Care | Provides benefits for long-term care expenses | Adds coverage for long-term care needs |

This table summarizes common endorsements and their impact on coverage, providing a quick reference for enhancing your insurance protection. By understanding the purpose and impact of these endorsements, you can make informed decisions about customizing your insurance policies.

Beyond The Fine Print: How Endorsements Transform Your Coverage

Your insurance policy isn't a static document; it's a living agreement. Insurance endorsements are the tools you use to adapt your coverage as your life changes. They offer the flexibility to enhance protection, adjust costs, and address specific risks. Essentially, an endorsement customizes your standard policy into a personalized shield.

For example, if you start a home-based business, your standard homeowner's insurance might not cover business-related liabilities. An endorsement can add this essential protection, safeguarding your personal assets. Adding a teenage driver to your auto policy may also require an endorsement to adjust liability coverage, reflecting the increased risk. For more information on homeowner's insurance coverage, you can check out this article: What Does Homeowners Insurance Really Cover? Find Out Here.

Impact On Premiums And Protection: A Balancing Act

Endorsements affect both your premium and the scope of your protection. Adding coverage typically increases your premium, while reducing coverage might lower it. This calls for careful balancing of cost and protection. Think of it like adding options to a car – each added feature increases the value, but also the price.

Endorsements can also significantly impact how claims are handled. A clear endorsement specifying coverage for specific items, such as jewelry, can simplify the claims process, leading to a smoother experience. Conversely, misunderstood endorsements can result in denied claims and unexpected expenses.

Strengthening Or Weakening Your Policy: Understanding The Nuances

While endorsements often bolster protection, they can also weaken it if not fully understood. An endorsement excluding specific types of damage, while potentially lowering your premium, could leave you exposed if that type of damage occurs. Therefore, understanding each endorsement's details is crucial.

The global insurance market is expected to approach $10 trillion by 2029, fueled by factors like technological advancements and increased demand for insurance. You can explore more detailed statistics here: https://www.statista.com/statistics/1192960/forecast-global-insurance-market/. In this evolving market, endorsements enable policies to adapt to new trends and individual needs. This adaptability highlights the importance of carefully reviewing each endorsement to ensure it fits your specific circumstances and strengthens, not weakens, your overall protection.

Navigating the Endorsement Process: From Request to Protection

Securing the right insurance endorsements is crucial for comprehensive coverage. This section offers a practical guide to navigating the endorsement process, ensuring your policy aligns with your specific needs. From identifying coverage gaps to implementing endorsements, this guide provides valuable insights into maximizing your insurance protection.

Identifying Your Needs: Assessing Coverage Gaps

The first step is understanding your existing coverage and pinpointing any potential gaps. Carefully review your policy, noting what is and isn't covered. Consider life changes, such as starting a home-based business or acquiring valuable items, that might require an insurance endorsement.

For instance, if you begin working from home, a standard homeowner’s policy may not adequately cover business equipment or liability. Also, think about potential risks specific to your location, like flooding or earthquakes. This assessment clarifies what additional protection you require. It's similar to evaluating your wardrobe—you identify what's missing before shopping.

Contacting Your Insurer: Initiating the Process

After identifying potential needs, contact your insurance agent. Clearly explain your situation and the specific coverage you're seeking. Be ready to provide details, such as the value of items you want to insure or the nature of your home-based business.

This initial conversation initiates the endorsement process. It’s like ordering a customized product—you provide your specifications to the manufacturer. Your agent can guide you through available insurance endorsement options and explain how they could affect your premiums.

Understanding Endorsement Options and Costs: Informed Decision-Making

Your insurance provider will present you with available endorsement options. Carefully review the terms and conditions of each endorsement, noting coverage details, limitations, and exclusions. Compare how each endorsement impacts your overall protection.

Endorsements usually come with an added cost, affecting your premium. Understand the connection between increased coverage and premium increases. This informed comparison helps you balance enhanced protection with your budget. It's similar to selecting options on a new car—weighing benefits against cost.

Review and Confirmation: Ensuring Accuracy

Before finalizing any insurance endorsement, thoroughly review the revised policy. Ensure the endorsement accurately reflects the changes you requested and that there aren't any unexpected limitations or exclusions. Don’t hesitate to ask your agent to clarify anything that’s unclear.

This final review confirms your understanding of the changes and avoids future issues. Think of it as proofreading an important document before signing. Once satisfied, confirm the endorsement and ensure it's correctly documented in your policy. This careful process guarantees your insurance coverage provides the specific protection you need.

The Digital Revolution in Insurance Endorsements

The insurance industry is changing, and so is how we handle endorsements. Adding, modifying, or removing coverage is moving away from paper and toward digital platforms. This shift makes the whole process faster, more efficient, and easier for policyholders.

This move to digital aligns with the growing demand for personalized insurance. The global insurance market sees a rising need for digital products shaped by technology and changing customer preferences. Insurance endorsements are crucial, letting insurers quickly adapt policies. Learn more about these trends: Global Insurance Market Trends 2024. Online platforms allow for more efficient processing, sometimes even in real-time.

Real-Time Policy Modifications: Speed and Efficiency

Digital platforms enable almost instant policy changes. Instead of waiting weeks for paperwork, updates can happen in minutes. This speed benefits both policyholders and insurers.

Think of it like email versus traditional mail. Communication and processing are much faster, offering more convenience and responsiveness. This allows for quick reactions to changing needs, providing adaptable coverage.

Simplified Language and Transparency: Clarity for Consumers

Digital endorsements also increase clarity. Policy language is often simpler, making it easier for policyholders to understand their coverage. Online portals provide easy access to policy documents and details.

Imagine a user-friendly dashboard to view and manage your insurance policy, including endorsements. This gives you greater control and understanding of your coverage. This transparency builds trust and helps with informed decisions.

Comparing Traditional and Digital Endorsement Processing

To better understand the advantages of digital endorsements, let's look at a comparison of traditional and digital methods. The following table highlights the key differences.

| Process Aspect | Traditional Method | Digital Method | Advantage |

|---|---|---|---|

| Speed | Weeks | Minutes | Digital drastically reduces processing time |

| Documentation | Paper-based | Electronic | Digital simplifies access and storage |

| Transparency | Often complex | Simple and accessible | Digital improves clarity and understanding |

| Customer Experience | Cumbersome | Streamlined and efficient | Digital provides a better experience |

| Accuracy | Prone to manual errors | Automated | Digital minimizes errors |

This table summarizes the benefits of digital endorsements. The shift towards digital is changing how policyholders manage coverage, creating a more efficient, customer-focused experience.

Reading Between the Lines: Mastering Endorsement Evaluation

Not all insurance endorsements are the same. Understanding the details of these policy modifications is crucial for ensuring you have the right coverage. This section provides a framework for carefully evaluating endorsements before you agree to them, allowing you to make informed decisions about your insurance.

Recognizing Red Flags: Protecting Your Interests

Evaluating an endorsement requires careful review. A key aspect is identifying red-flag language. Look closely at phrases that substantially limit coverage, introduce many exclusions, or shift responsibility to the policyholder. For example, an endorsement excluding damage from "acts of God" can be too broad and leave you unprotected from a range of unforeseen events.

Another important area is finding contradictions between the endorsement and your original policy. If an endorsement seems to clash with the initial terms of your policy, ask your agent for clarification. These inconsistencies could result in denied claims or lower payouts. Treat any contradictions as serious warnings.

Finally, be cautious of standardized endorsements that might not fully address your specific needs. While pre-written endorsements are convenient, they may not adequately cover unusual risks or circumstances. If a standardized endorsement isn't a perfect fit, discuss customizing it with your agent. This ensures your policy reflects your particular situation.

Analyzing Real-World Scenarios: Learning From Others' Mistakes

Reviewing real claim scenarios offers valuable insights into common endorsement problems. Cases where claims were denied due to poorly written or misinterpreted endorsements highlight the need for thorough review. These real-world instances offer practical lessons on what to look out for.

Expert analysis of these cases can further explain the potential consequences of inadequate endorsement review. By learning from others' mistakes, you can avoid similar problems and safeguard your own interests. You might be interested in this Comparative Review: The 7 Best Life Insurance Companies To Trust This Year. Changes in how insurance endorsements are handled, including the importance of compliant content marketing, have been influenced by technology.

Negotiating Favorable Terms: Advocating for Your Needs

Don't hesitate to negotiate with your insurance company for better endorsement terms. If you believe an endorsement's restrictions are excessive or the cost is too high, discuss your concerns with your agent. Insurance companies are often willing to work with policyholders to find solutions that work for everyone.

An insurance policy is a contract between you and the insurer. You have the right to advocate for your needs and ensure the coverage meets your expectations and budget. This proactive approach allows you to secure the best possible protection.

Best Practices: A Checklist for Endorsement Evaluation

Here’s a helpful checklist to use when you evaluate insurance endorsements:

- Scrutinize wording: Watch out for vague or excessively broad language that might limit coverage.

- Check for contradictions: Make sure the endorsement aligns with your base policy and doesn’t create conflicts.

- Assess customization: Consider if standardized endorsements need changes to fit your particular requirements.

- Analyze claim scenarios: Learn from real-world examples of endorsement problems.

- Negotiate terms: Don’t be afraid to advocate for better coverage or pricing.

- Document everything: Keep records of all endorsements, conversations with your agent, and policy changes.

By following these best practices, you can effectively evaluate endorsements and feel confident in your insurance coverage. This careful approach ensures your policy offers the exact coverage you need, protecting you from unforeseen financial difficulties. Understanding your insurance policy, including its endorsements, is vital for maximizing your peace of mind.

Comments are closed.