Making Sense of Life Insurance: A 2025 Guide

Choosing the right life insurance policy is crucial for financial security. This guide clarifies six common types, including term life vs whole life insurance, helping you make the best decision for your needs and budget. We'll cover term life, whole life, universal life, indexed universal life, variable life, and guaranteed universal life insurance. Understand the pros, cons, costs, and key features of each to find the perfect fit, whether you seek temporary protection or a lifelong plan.

1. Term Life Insurance

In the ongoing debate of term life vs whole life insurance, term life often emerges as a strong contender for those seeking affordable and straightforward coverage. Term life insurance provides coverage for a specified period (the 'term'), typically ranging from 10 to 30 years. If the insured person dies during this term, the policy pays a death benefit to the designated beneficiaries. After the term expires, coverage ends, and the policy has no residual value. This makes it distinct from whole life insurance, which offers lifelong coverage and a cash value component. Term life excels in providing a large death benefit for a significantly lower premium compared to permanent policies, making it an attractive option for many.

The infographic illustrates a simplified decision-making process for choosing between term and whole life insurance. It starts by asking if you need lifelong coverage. If yes, it directs you towards whole life. If no, it asks how long you need coverage, leading you to consider different term lengths. This visual aid helps clarify the fundamental difference between the two types of insurance.

Term life insurance features include a fixed coverage period (commonly 10, 15, 20, or 30 years), level premiums that remain constant throughout the term, and a pure death benefit with no cash value component. Renewable or convertible options may be available, allowing policyholders flexibility in extending or changing their coverage. For example, a 35-year-old parent might purchase a 20-year term policy to cover the period until their children are financially independent. Products like Mutual of Omaha's Term Life Express offer simplified underwriting, making the application process easier. Similarly, Banner Life's OPTerm offers highly competitive rates for healthy individuals. Learn more about Term Life Insurance

Pros of Term Life Insurance:

- Lower Premiums: Significantly more affordable than whole life insurance.

- Simplicity: Easy to understand and purchase.

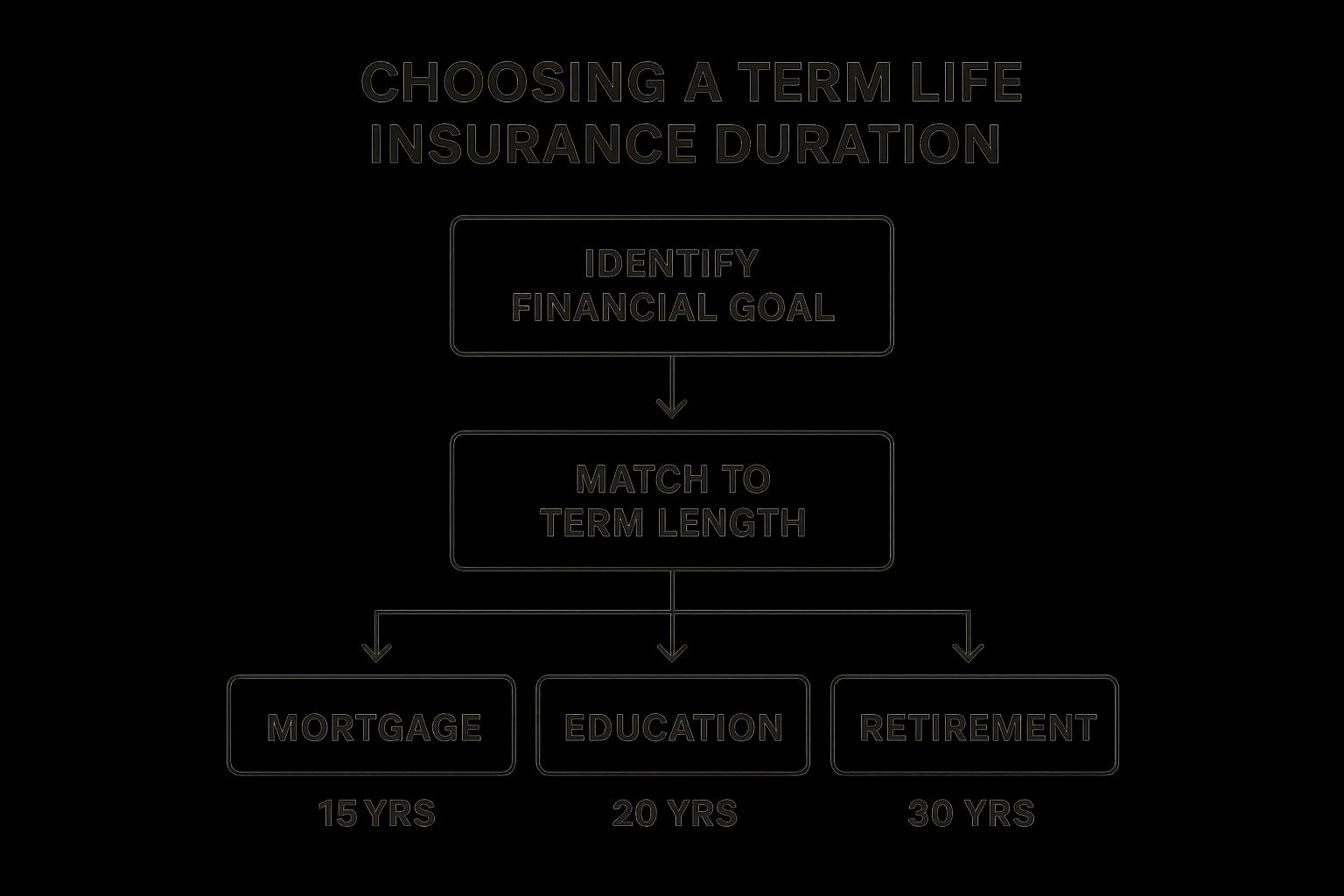

- Targeted Coverage: Ideal for specific, temporary financial obligations like mortgages or children's education.

- Easy Comparison: Simple to compare prices across different providers.

- Higher Death Benefit: Provides a larger death benefit for the same premium dollar compared to permanent policies.

Cons of Term Life Insurance:

- Limited Coverage: No coverage after the term expires.

- No Cash Value: No cash value accumulation or investment component.

- Renewal Costs: Premiums increase substantially if you renew after the term expires.

- Insurability: May become uninsurable when attempting to purchase a new policy later in life.

- Limited Living Benefits: No living benefits unless additional riders are purchased.

Tips for Choosing Term Life Insurance:

- Match Term to Need: Select a term length that aligns with your specific needs, such as the duration of your mortgage.

- Explore Conversion Options: Look for policies with conversion options, allowing you to transition to permanent coverage without new medical underwriting.

- Layered Coverage: Consider layering multiple term policies of different lengths to match decreasing insurance needs over time.

- Short-Term Needs: Consider annual renewable term if you need coverage for a very short period.

- Enhanced Coverage: Add riders like accelerated death benefits for more comprehensive coverage.

Term life insurance is popularized by financial experts like Dave Ramsey and Suze Orman, who advocate for its affordability and effectiveness in meeting specific financial needs. Companies like Haven Life, specializing in simplified online term insurance, and Policygenius, making term life comparison shopping accessible online, have also contributed to its increased popularity.

Term life insurance deserves its place in the "term life vs whole life" discussion because it provides a cost-effective solution for individuals and families seeking temporary but substantial death benefit protection. It's particularly well-suited for those prioritizing affordability and simplicity. It's crucial to weigh the pros and cons in light of your individual circumstances and financial goals when deciding which type of life insurance best fits your needs.

2. Whole Life Insurance

When comparing term life vs whole life, whole life insurance stands as the permanent counterpart to term life's temporary coverage. It's designed to provide lifelong protection, offering a guaranteed death benefit that will be paid out to your beneficiaries no matter when you pass away, as long as premiums are maintained. Unlike term life, which focuses solely on providing a death benefit, whole life insurance also incorporates a cash value component that grows at a guaranteed rate, essentially acting as a built-in savings vehicle. This dual nature makes whole life insurance a complex financial product that can serve multiple purposes throughout the policyholder’s life, from protecting loved ones to supplementing retirement income. It combines insurance protection with a conservative savings element.

Whole life insurance policies typically feature fixed, level premiums that will never increase, offering predictable costs for the duration of the policy. The cash value component grows tax-deferred, meaning you won't pay taxes on the growth until you withdraw it. Many whole life policies, particularly those offered by mutual insurance companies, also offer the potential for dividend payments, which can further enhance the cash value accumulation. Policyholders can also borrow against their accumulated cash value, providing access to funds without incurring tax consequences. Learn more about Whole Life Insurance for a deeper dive into these concepts.

Pros:

- Lifetime Coverage: Provides peace of mind knowing your beneficiaries will receive a death benefit regardless of when you pass away.

- Guaranteed Cash Value Growth: Offers a safe and predictable way to accumulate savings on a tax-deferred basis.

- Potential Dividend Payments: Participating policies may offer dividends, which can be used to increase cash value or reduce premiums.

- Forced Savings Vehicle: Helps instill financial discipline by requiring regular premium payments.

- Loan Provisions: Access accumulated cash value without tax penalties.

- Estate Planning Benefits: Can be used to cover estate taxes and provide liquidity to your heirs.

Cons:

- High Premiums: Significantly more expensive than term life insurance.

- Lower Investment Returns: Compared to other investment options, the returns on cash value growth can be relatively modest.

- High Surrender Charges: Withdrawing cash value in the early years can incur hefty fees.

- Complexity: The various features and options can make it challenging to compare policies.

- Inflexible Premium Structure: Fixed premiums may strain budgets, especially in the early years.

Examples of Whole Life Insurance in Action:

- Northwestern Mutual offers whole life policies known for their consistent dividend payments.

- MassMutual also provides participating whole life insurance with a history of strong performance.

- New York Life offers Custom Whole Life, allowing for shorter payment periods than a lifetime commitment.

Tips for Utilizing Whole Life Insurance:

- Explore Accelerated Payment Options: Consider 10-Pay or 20-Pay options to complete premium payments in a shorter timeframe.

- Research Dividend History: Review the insurer's track record of dividend payments (while keeping in mind that future dividends are not guaranteed).

- Strategic Loan Usage: Utilize policy loans for major expenses or investment opportunities.

- Consider Paid-Up Additions Rider: This rider can accelerate cash value growth.

- Consult with a Qualified Agent: Work with an agent who can clearly explain the difference between guaranteed and projected performance.

Whole life insurance earns its place in the term life vs whole life discussion by catering to specific needs. It's particularly relevant for individuals seeking lifelong coverage, those who prioritize guaranteed cash value growth, and those interested in using life insurance as part of a broader financial and estate planning strategy. While the higher cost may be prohibitive for some, the combination of lifelong protection, cash value accumulation, and potential tax advantages makes whole life insurance a compelling option for certain individuals and families seeking long-term financial security. It's especially relevant for families, couples planning for the future, and business owners looking for asset diversification and estate planning tools.

3. Universal Life Insurance

When comparing term life vs whole life insurance, universal life insurance often emerges as a compelling middle ground. It offers the permanent death benefit of whole life insurance combined with greater flexibility, making it an attractive option for those seeking a balance between guaranteed coverage and the potential for cash value growth. Learn more about Universal Life Insurance

Universal life insurance works by combining a death benefit with a cash value component. Your premiums, after covering the cost of insurance and administrative fees, are credited to your cash value account. This account earns interest based on current market rates, potentially offering higher returns compared to the fixed rates of whole life policies. However, unlike whole life, the interest rate isn't fully guaranteed and is subject to market fluctuations, although a minimum guaranteed rate is typically provided.

One of the key features of universal life is its flexibility. Premium payments can be adjusted within certain limits, allowing you to increase, decrease, or even skip payments (if sufficient cash value exists) as your financial situation changes. The death benefit can also be adjusted – increased (subject to underwriting) or decreased – to align with your evolving needs. This flexibility makes universal life a suitable choice for individuals experiencing fluctuating income or those anticipating changing life circumstances.

Features of Universal Life Insurance:

- Flexible premium payments (within limits)

- Adjustable death benefit options

- Cash value growth tied to current interest rates (minimum guaranteed rate)

- Transparency in cost of insurance and administrative fees

- Ability to skip payments if sufficient cash value exists

- Option to increase or decrease coverage as needs change

Pros:

- Premium flexibility: Adapt payments to your financial situation.

- Adjustable death benefit: Customize coverage as your needs evolve.

- Cash value accessibility: Withdraw or borrow against your cash value.

- Potential for higher returns: Benefit from favorable interest rate environments.

- Transparency: Understand how your premiums are allocated.

Cons:

- Cash value growth dependency: Returns fluctuate with interest rates.

- No guaranteed level premiums: Unlike whole life, premiums can change.

- Risk of policy lapse: Insufficient cash value can lead to policy termination.

- Complexity: More complex to understand and manage than term or whole life.

- Higher fees: Typically higher fees than term insurance.

Examples of Universal Life Policies:

- Transamerica's financial foundation UL policy with living benefits

- Lincoln Financial's LifeGuarantee UL offering guaranteed death benefit with minimal cash accumulation

- John Hancock's Protection UL with lower premiums among permanent policies

Tips for Managing a Universal Life Policy:

- Pay more than the minimum premium early on: Build a cash value buffer.

- Regularly review policy performance: Especially during low interest rate periods.

- Consider a no-lapse guarantee rider: Secure your death benefit against market volatility.

- Understand interest rates: Compare current and guaranteed rates in policy illustrations.

- Work with a financial advisor: Determine appropriate premium levels to meet your goals.

Universal life insurance deserves its place in the term life vs whole life discussion because it bridges the gap between the two. While term life provides affordable temporary coverage and whole life guarantees lifelong protection with fixed premiums, universal life offers a flexible permanent option with the potential for greater cash value growth. This makes it particularly appealing to individuals who desire lifelong coverage but need the flexibility to adjust premiums and death benefits over time, and are comfortable with some level of market risk. It’s particularly well-suited for families, couples, business owners, and even singles seeking long-term financial security with a degree of control over their policy. However, it’s crucial to understand the complexities of universal life, including the impact of fluctuating interest rates on cash value growth, before making a decision. Consulting with a financial advisor is highly recommended to determine if universal life insurance aligns with your individual financial goals and risk tolerance.

4. Indexed Universal Life Insurance

Indexed Universal Life (IUL) insurance often enters the conversation when comparing term life vs whole life insurance, offering a unique blend of permanent coverage and market-linked growth potential. IUL policies provide a death benefit similar to whole life, but the cash value growth is tied to the performance of a stock market index, like the S&P 500. This offers the opportunity for higher returns compared to traditional universal life insurance, while also providing a safety net against market downturns, typically with a 0% floor preventing negative returns. However, potential gains are usually limited by a cap rate.

IUL policies achieve this balance through a few key mechanisms. A participation rate determines the percentage of index gains credited to your cash value. For instance, a 90% participation rate means you'd receive 90% of the index's growth. A cap rate limits the maximum return you can earn in a given period. For example, a 10% cap limits your gains to 10%, even if the index performs better. Finally, the 0% floor ensures your cash value doesn't decrease due to market losses. While you won't experience the full upswing of the market, your cash value is shielded from declines. IUL also offers flexible premiums and adjustable death benefits, allowing you to adapt the policy to your changing financial needs.

Examples of IUL policies include:

- Pacific Life's PDX IUL: Offers uncapped indexing strategy options, potentially providing greater upside potential.

- Nationwide's IUL Accumulator II: Features a multiplier feature for potentially enhanced returns.

- Allianz Life's Life Pro+ Advantage: Provides multiple indexing options for diversification.

When and Why to Use IUL:

IUL insurance can be a suitable option when comparing term life vs. whole life if you seek the lifelong protection of permanent life insurance with the potential for greater cash value growth than traditional whole life. It's particularly relevant for individuals with a longer-term horizon who are comfortable with some market exposure but prioritize downside protection. Families and couples seeking long-term financial security, business owners looking for tax-advantaged accumulation, and even singles looking to build cash value over time might find IUL appealing.

Pros:

- Potential for higher returns than whole life or traditional universal life.

- Protection against market losses with a guaranteed floor.

- Tax-advantaged cash value growth and access through loans.

- Premium flexibility.

- Potential for living benefits through riders.

- Death benefit for estate planning.

Cons:

- Complex crediting methods and policy mechanics.

- Returns limited by caps, participation rates, and spreads.

- Higher fees and expenses than term insurance.

- Illustrations may use optimistic assumptions.

- Risk of policy lapse if underfunded.

- No direct investment in market indices (no dividends).

Tips for Choosing and Managing an IUL Policy:

- Focus on guaranteed features: Don't solely rely on projected returns.

- Understand the mechanics: Learn how caps, participation rates, and floors affect potential returns.

- Overfund early if accumulating cash: This can boost growth potential.

- Compare carriers: Look at different crediting methods and historical performance.

- Annual review: Adjust the policy based on actual performance.

- Check financial strength ratings: Ensure the insurer is reputable.

By understanding the intricacies of IUL insurance and carefully weighing its pros and cons, you can make an informed decision when choosing between term life vs. whole life insurance and determine if an IUL policy aligns with your long-term financial goals.

5. Variable Life Insurance

When comparing term life vs whole life insurance, variable life insurance often enters the conversation as a more complex, albeit potentially rewarding, form of permanent coverage. Unlike term life, which provides coverage for a specific period, variable life insurance offers lifelong protection combined with an investment component. This makes it appealing to those seeking long-term financial security with the potential for higher returns, but it’s crucial to understand the inherent risks involved.

Variable life insurance works by allowing policyholders to allocate their cash value into various sub-accounts, similar to mutual funds. These sub-accounts typically invest in a range of asset classes, including stocks, bonds, and money market instruments. The policy's cash value grows tax-deferred, and the death benefit can potentially increase based on the performance of these investments. However, unlike whole life insurance, there are no minimum cash value guarantees, meaning the cash value can fluctuate and even decrease based on market performance.

Features:

- Cash value invested in sub-accounts: Similar to managing a portfolio of mutual funds, offering greater control and potential for growth.

- Multiple investment options: Spanning various asset classes to allow for diversification and alignment with individual risk tolerance.

- Policyholder assumes investment risk: The potential for higher returns comes with the responsibility of managing investment choices and bearing potential losses.

- No minimum cash value guarantees: Unlike whole life insurance, the cash value is tied to market performance and can fluctuate.

- Fixed or flexible premium options: Depending on the specific policy variant, offering flexibility in premium payments.

- Death benefit may increase: Strong investment performance can lead to a higher death benefit, enhancing the policy's value over time.

Pros:

- Highest growth potential among permanent life insurance types: Offers the opportunity to outpace inflation and accumulate wealth.

- Professional money management options: Some policies provide access to professional money managers who can assist with investment decisions.

- Diversification across multiple investment options: Helps mitigate risk by spreading investments across different asset classes.

- Tax-deferred growth of cash value: Allows for compounding growth without immediate tax implications.

- Ability to switch between sub-accounts without tax consequences: Provides flexibility to adjust investment strategy as needed.

- Death benefit can increase with strong investment returns: Adds an additional layer of potential financial benefit for beneficiaries.

Cons:

- Investment risk borne by policyholder: The potential for loss requires careful consideration of risk tolerance.

- Higher fees than comparable direct investments: Mortality costs, administrative fees, and fund expenses can impact overall returns.

- Complexity requiring ongoing management: Requires active monitoring and adjustments to the investment strategy.

- Typically higher minimum premiums: May not be as accessible as term life insurance for those on a tighter budget.

- Subject to securities regulations: Requires a prospectus and understanding of associated regulations.

- Not suitable for conservative investors: The inherent market risk makes it less suitable for those with a low risk tolerance.

Examples:

- Prudential's VUL Protector

- Lincoln Financial's VULONE

- Nationwide's Variable Universal Life Accumulator II

Tips:

- Consider your risk tolerance: Variable life insurance is best suited for individuals comfortable with market fluctuations.

- Diversify sub-account investments: Spread investments across different asset classes to manage risk.

- Monitor and rebalance investments periodically: Ensure your portfolio remains aligned with your goals and risk tolerance.

- Understand all layers of fees: Be aware of mortality charges, administrative fees, and fund expenses.

- Consider using a financial advisor with securities licenses: Seek professional guidance to navigate the complexities of variable life insurance.

- Review prospectus carefully before investing: Understand the details of the policy and its associated investment options.

When and why to use this approach:

Variable life insurance is a suitable option for individuals seeking lifelong insurance coverage combined with the potential for higher investment returns. It’s particularly relevant when comparing term life vs whole life for those who are comfortable with market risk, have a longer time horizon, and are looking for a way to build cash value with potential for growth beyond what traditional whole life offers. This approach is particularly popular among high-net-worth individuals and those seeking wealth transfer strategies. However, it's crucial to carefully weigh the risks and benefits before making a decision.

6. Guaranteed Universal Life Insurance

When comparing term life vs whole life insurance, Guaranteed Universal Life (GUL) insurance often emerges as a compelling middle ground. This hybrid policy blends the affordability of term life with the permanence of whole life, offering a unique approach to lifelong protection. Essentially, GUL insurance provides a guaranteed death benefit to a specific age (commonly 90, 95, 100, or even 121) as long as you maintain the required premium payments. This makes it function much like a "term policy for life," but at a considerably lower cost than traditional whole life insurance.

How it Works:

GUL policies focus primarily on the death benefit, minimizing the cash value accumulation component typically found in whole life insurance. You pay a level premium for the chosen guaranteed period, and the insurer guarantees the death benefit payout to your beneficiaries if you pass away within that timeframe. While some GUL policies may accrue a small amount of cash value, it's significantly less than whole life and isn't designed for substantial wealth building. This streamlined focus on death benefit protection helps keep premiums lower.

Examples:

- Protective's Advantage Choice UL offers strong guarantees and competitive pricing in the GUL market.

- Lincoln Financial offers GUL coverage extending all the way to age 121, providing maximum longevity protection.

- American General's Secure Lifetime GUL 3 provides options that can even include a return of premium feature.

Why GUL Deserves Its Place in the Term Life vs Whole Life Discussion:

GUL bridges the gap for individuals who want the security of lifelong coverage without the high premiums and complex investment component of whole life insurance. It provides a simplified approach to permanent life insurance, focusing solely on guaranteeing a death benefit for a specified period. This makes it an attractive alternative to both term and whole life insurance in specific scenarios.

Features and Benefits:

- Guaranteed Death Benefit: The death benefit is locked in for the chosen period, providing peace of mind and financial security for your beneficiaries.

- Level Premiums: Premiums remain consistent throughout the guaranteed period, making budgeting predictable.

- No Market Risk Exposure: Unlike variable life insurance, GUL policies aren't tied to market performance, protecting your death benefit from fluctuations.

- Simplified Structure: GUL is easier to understand and manage compared to more complex permanent life insurance products.

- Estate Planning and Legacy Goals: GUL is an effective tool for estate planning, providing liquidity to cover estate taxes, debts, and final expenses.

- Protection Against Longevity Risk: Coverage to age 121 eliminates the risk of outliving your coverage, a concern with term life policies.

Pros:

- Lower premiums than whole life insurance.

- Guaranteed death benefit without market risk.

- Simplified structure compared to other permanent products.

- Ideal for estate planning and legacy goals.

- No need to monitor investment performance.

- Protection against longevity risk.

Cons:

- Little to no cash value accumulation.

- Less premium flexibility than traditional universal life.

- Missing payments can void guarantees.

- Limited living benefits without added riders.

- Higher cost than term insurance.

- Less efficient for wealth accumulation goals.

Actionable Tips:

- Carefully review the guaranteed period and ensure it aligns with your longevity expectations. Consider coverage to age 121 for maximum protection.

- Set up automatic premium payments to avoid missed payments and potential lapse of coverage.

- Explore adding riders for long-term care or chronic illness if you desire living benefits.

- Compare quotes from multiple insurance carriers to find the most competitive pricing.

When and Why to Use GUL:

GUL is an excellent choice for individuals seeking permanent life insurance primarily for estate planning, legacy protection, or covering final expenses. It's particularly suitable for those who want guaranteed lifelong coverage but don't prioritize cash value accumulation. If your main objective in the term life vs whole life debate is affordable, guaranteed lifelong death benefit protection, then GUL is worth considering. If, however, you are looking for a cash value component or significant wealth building opportunities, other permanent life insurance options may be more appropriate.

6 Major Life Insurance Types Comparison

| Policy Type | 🔄 Implementation Complexity | 🛠️ Resource Requirements | 📊 Expected Outcomes | 💡 Ideal Use Cases | ⭐ Key Advantages |

|---|---|---|---|---|---|

| Term Life Insurance | Simple underwriting, easy to purchase | Low (basic underwriting, no investments) | Pure death benefit during specified term | Temporary financial obligations (mortgage, education) | Low premiums, straightforward, large death benefit |

| Whole Life Insurance | Moderate complexity, permanent coverage | High (premium payments + cash value management) | Lifetime coverage, guaranteed cash value growth | Long-term financial planning, forced savings | Lifetime coverage, cash value growth, dividends |

| Universal Life Insurance | Moderate to high complexity, flexible premiums | Moderate (active management of premiums) | Flexible death benefit and premiums, cash value growth linked to interest rates | Policyholders needing premium/death benefit flexibility | Premium flexibility, adjustable coverage, transparency |

| Indexed Universal Life | High complexity, market-linked cash value growth | High (requires market performance monitoring) | Potential for higher cash value growth with downside protection | Retirement income planning, tax-advantaged growth | Market-linked returns with downside protection |

| Variable Life Insurance | High complexity, manages investment sub-accounts | Very high (investment selection & monitoring) | Highest growth potential, variable cash value & death benefit | Investors tolerant to risk seeking growth | Investment choice, high growth potential |

| Guaranteed Universal Life | Moderate complexity, permanent coverage with guarantees | Moderate (focus on guaranteed death benefit) | Guaranteed death benefit to advanced age, minimal cash value | Estate planning, affordable permanent coverage | Guaranteed death benefit, lower cost than whole life |

Choosing Your Path to Financial Security

Navigating the world of life insurance can feel complex, but understanding the core differences between term life vs whole life insurance, and other policy types like universal, indexed, and variable life, empowers you to take control of your financial future. As we've explored, term life insurance offers affordable coverage for a specific period, while whole life insurance provides lifelong protection combined with a cash value component. Other options like universal, indexed universal, variable, and guaranteed universal life insurance offer varying degrees of flexibility and investment potential. The key takeaway is that there's no one-size-fits-all solution.

Your ideal policy depends on your individual circumstances, whether you're a single student seeking basic coverage, a couple planning for a family, a business owner protecting your assets, a frequent traveler needing comprehensive coverage, or someone seeking long-term financial peace of mind. The most important factors to consider are the length of coverage you need, the premium you can comfortably afford, the potential for cash value growth, and your risk tolerance if you're considering investment-linked policies.

Next Steps:

- Evaluate your needs: Determine your coverage needs based on your financial obligations, dependents, and long-term goals.

- Compare quotes: Use our online tools to compare quotes from different insurers and find the best rates for your chosen policy type.

- Consult a professional: If you're unsure which policy is right for you, consider speaking with a financial advisor who can provide personalized guidance.

Mastering the nuances of term life vs whole life insurance, along with the broader spectrum of life insurance options, is a significant step towards building a secure financial foundation. By carefully considering your needs and utilizing the resources available, you can make an informed decision that protects your loved ones and provides lasting peace of mind. Take control of your financial future today – your future self will thank you.

Comments are closed.